Research Article

Intellectual Capital and Startup Survival in Global Accelerator Programs

Carlos Canfield carlos.canfield@gmail.com

Enrique Wiencke enrique.wiencke@anahuac.mx

Carlos Canfield carlos.canfield@gmail.com

Enrique Wiencke enrique.wiencke@anahuac.mx

Intellectual Capital and Startup Survival in Global Accelerator Programs

BAR - Brazilian Administration Review, vol. 22, no. 1, e230071, 2025

ANPAD - Associação Nacional de Pós-Graduação e Pesquisa em Administração

Received: 11 July 2023

Accepted: 30 October 2024

Published: 31 March 2025

ABSTRACT

Objective: this research investigates the impact of intellectual capital (IC) on the longevity of startups in global accelerator programs, focusing on human, social, and structural capital.

Methods: Utilizing data from Emory University’s GALI Entrepreneurship Database Survey Program, a logistic regression model predicts the survival likelihood of pre-seed stage startups based on their initial IC levels.

Results: the findings reveal that social and structural capital positively influence startup survival, while human capital does not. Specifically, founders’ entrepreneurial experience, a proxy for specific human capital, does not enhance survival odds.

Conclusions: this suggests that other factors, such as socio-demographic characteristics, financial constraints, diversity, temporal aspects, gender, and accelerator-related variables, play a significant role in startup success. By controlling for these predictors, the study isolates the effect of IC, thereby strengthening its contribution to the literature on IC and entrepreneurship. It provides cross-sectional and global evidence of IC’s influence on new ventures, offering practical implications for designing more effective accelerator programs and policies to foster new venture creation in various contexts.

Keywords: Accelerator programs+ for-profit new venture performance+ GALI Entrepreneurship Database Program+ intellectual capital dimensions+ pre-seed stage.

INTRODUCTION

The object of study

The importance of new businesses for regional and economic growth was recognized in Schumpeter’s seminal work, The Theory of Economic Development, in 1934 (Del Sarto et al., 2020). Scholars, practitioners, and policymakers acknowledge that startups significantly contribute to economic expansion, job creation, and societal prosperity (Audretsch et al., 2006; Pradhan et al., 2020).

Nascent ventures face numerous challenges, including operational, competitive, resource, and planning issues, threatening their long-term survival. Startups are particularly vulnerable in their early years, with a 30% failure rate within the first two years (Picken, 2017; Santisteban & Mauricio, 2017). However, this risk decreases over time (Yang & Aldrich, 2017).

The survival of new firms can be analyzed through three main factors: personal attributes, firm-specific characteristics, and the external environment (Brüderl et al., 1992). Challenges to survival often include limited financial resources (Smilor, 1997) and an inexperienced founding team (Gruber et al., 2008).

While the existing literature on startup survival is extensive, it often remains confined to a single theoretical perspective, region, or industry (Andreeva & Garanina, 2016; Baum & Silverman, 2004; Cressy, 1996; Gimmon & Levie, 2010). Most studies have been conducted in advanced economies such as Europe, North America, and Asia, with less emphasis on emerging economies (Azeem & Khanna, 2023). Empirical research employs regression-based models, particularly logistic regression models (LR), to examine the relationship between various antecedents and outcomes, often focusing on internal resources and non-financial performance measures.

Given the limited scope of previous research, future studies should prioritize cross-country analyses. The rise of startups in emerging economies and the expanding research on startup survival offer numerous opportunities for new investigations. These studies can explore the interplay between internal and external factors affecting startup survival in these emerging markets. Therefore, it is essential to include emerging countries in such research endeavors.

This study examines startups in global accelerator programs, including those in emerging economies, using the resource-based view (RBV) and human capital theory. Building on Cooper et al. (1994), it posits that initial financial and human capital allocations predict new venture survival (Van Praag, 2003).

The impact of initial conditions on companies’ performance

Predicting new venture performance based on initial observable factors is a key interest for entrepreneurship researchers, as it can optimize resource allocation, benefiting both entrepreneurs and society (Dahlqvist et al., 2000).

The survival of startups has been extensively studied from various theoretical perspectives. Azeem and Khanna (2023) highlight the resource-based view (RBV) as the most frequently cited perspective, forming the foundation of our study. RBV posits that a company’s unique, valuable, difficult-to-replicate, and irreplaceable resources and capabilities confer a competitive edge and enhance performance (Barney, 1991; Wernerfelt, 1984). Among these resources, intellectual capital (IC) is an intangible asset intricately linked to a company’s strategy, which is crucial for longevity (Rossi et al., 2016).

Our research is informed by the Resource-Based View (Barney et al., 2001) and in human capital theory (Becker, 1964; Mincer, 1974), underscores the pivotal role of individual expertise and abilities in driving economic productivity. Consistent with Cooper et al. (1994), we argue that a company’s initial financial resources and human capital are fundamental to its survival, especially for nascent enterprises (Van Praag, 2003). This perspective highlights the essential contribution of both tangible and intangible resources possessed by founding teams to the success of a startup (Strotmann, 2007).

Research purpose

Our study examines startups, the engines of innovation and economic growth, focusing on the role of initial intangible knowledge, or intellectual capital (IC), during the critical pre-seed phase. By controlling financial availability, environmental conditions, and founding team characteristics, we aim to underscore the significance of IC in startup longevity.

Nascent enterprises frequently join accelerator programs for financial support and expert guidance (Radojevich-Kelley & Hoffman, 2012). This study investigates the correlation between the intellectual capital (IC) of founding teams - including their skills, knowledge, experience, relationships, and abilities - and the survival rates of these ventures. These startups often emerge in unstable environments to seize new market opportunities (Beckman & Burton, 2008; Davidsson & Honig, 2003). Our objective is to determine how a founder’s initial IC influences the survival chances of these ventures.

Our study focuses on startups in global accelerator programs, utilizing data from the Entrepreneurship Database Program (EDP) at Emory University, part of the Global Accelerator Learning Initiative (GALI, 2020). Launched in 2013, the EDP examines the causal effects of accelerating impact-oriented ventures. It employs a standardized set of questions used by all participating accelerators in their application processes, enhancing responsiveness and allowing observation of the entire pool of serious applicants. Program managers also track which applicants join their programs (Lall et al., 2020). These programs prioritize the IC of founders according to their selection criteria (GALI, 2021).

Most studies on startup survival exhibit a geographical bias, primarily focusing on developed countries (Azeem & Khanna, 2023). Our research aims to address this gap by incorporating geographic and socio-economic diversity. Recognizing the lack of comprehensive studies on startups in emerging economies (Andreeva & Garanina, 2016), we seek to rectify this. Our study expands the scope by examining the impact of intellectual capital (IC) - including both initial financial resources and intangible knowledge - on the global growth of startups, with a focus on the pre-seed stage of accelerator programs.

This study employs a logistic regression model to evaluate the influence of numerous factors on the survival probabilities of startups within our sample. The model also predicts the likelihood of a startup’s success during its initial stages. Our primary objective is to enhance the understanding of how intellectual capital (IC) impacts the success of pre-seed startups, particularly those participating in accelerator programs.

This study offers valuable insights for a range of stakeholders. Policymakers can leverage this knowledge to craft policies that foster startup growth by emphasizing the importance of intellectual capital (IC) in team formation, thereby cultivating a dynamic and prosperous startup ecosystem. Accelerator programs and venture capitalists can utilize these findings to refine their selection and support processes, enhancing the success rates of the startups they endorse. Similarly, practitioners, including startup founders and employees, can apply this knowledge to focus on developing and enhancing their IC, enabling them to better adapt to growing market opportunities. The structure of the remaining sections of the study is as follows: The second section establishes the relevant literature that supports the conceptual framework and the hypotheses under study; the third section discusses materials and methods, followed by the estimation results and their discussion.

LITERATURE REVIEW AND HYPOTHESES STATEMENT

Our analysis investigates how a firm’s founding conditions affect its performance, particularly its longevity. Various perspectives have examined this topic. Organizational ecology suggests that firms with superior initial resources are more likely to survive through natural selection (Fuertes-Callén et al., 2022; Hannan & Freeman, 1977; Romanelli, 1989). Other research highlights the enduring impact of strategic choices made at the outset. For instance, Eisenhardt and Schoonhoven (1990) demonstrated that founding teams have a lasting influence on firm performance. Similarly, Cooper et al. (1994) found that initial financial and human capital are strong predictors of firm performance and survival. Kimberly (1979) also argued that environmental conditions, the founder’s personality, and initial strategic choices significantly shape organizational behavior.

The entrepreneurial context

Entrepreneurship involves a dynamic process of team formation and adaptation to meet customer needs. Salamzadeh and Kesim (2015) describe business development as a life cycle with stages including idea conception, prototype development, market entry, product sales, and job creation. Wong et al. (2005) argue that preparation for the startup phase is the crucial foundation that shapes emerging ventures. Brüderl and Schussler (1990) suggest that early survival indicates initial success, while long-term endurance highlights the importance of adaptability in later stages.

The impact of initial conditions on companies’ performance

The resource-based view (RBV) posits that a founder’s attributes and circumstances significantly impact venture performance. Dencker et al. (2009) found that knowledge positively influences startup survival in Germany, with the cumulative experience of founders bolstering knowledge integration. Research has shown a varied positive correlation between talent and performance, dependent on a country’s macroeconomic development (Furlan, 2019; Mayer-Haug et al., 2013). Studies have also demonstrated a differentiated positive impact of talent across different entrepreneurial stages and economic contexts (Kerrin et al., 2017). However, these effects can be nonlinear or varied, contingent on factors such as business development stages, survival duration, administrative maturity, technological orientation, funding sources, performance measures, and the specific conditions of the countries and sectors (Delmar & Shane, 2006).

Human capital theory suggests that an individual’s human capital, comprising their education, work experience, and job training, is vital for achieving organizational goals, securing a competitive edge, and enhancing financial performance (Becker, 1994; Unger et al., 2011). Gimmon and Levie (2010) applied this theory to examine how founder qualities affect the ability to attract external investment and ensure the survival of new high-tech firms. Their research underscores that a founder’s managerial experience and academic credentials are more critical in attracting external investment than their technological expertise.

Cooper et al. (1994) distinguished four types of initial capital in their influential study: general human capital, management expertise, industry-specific knowledge, and financial capital. General human capital, from the entrepreneur’s background, includes knowledge that increases productivity and access to network resources. Management expertise is tacit knowledge from the entrepreneur’s previous general management experience, learning by doing or observing. Industry-specific expertise is also tacit and expensive to obtain without prior industry experience, and it is essential for understanding the context of suppliers, competitors, and customers. Financial capital, the most concrete form of capital, serves as a cushion and allows strategic flexibility.

This study leverages the resource-based view (RBV) and human capital theory, building on Cooper et al.’s (1994) findings, to propose that initial allowances of financial and human capital are reliable predictors of the survival of new ventures (Van Praag, 2003).

Intellectual capital

Intellectual capital (IC) is widely acknowledged but lacks a precise definition (Bontis, 1998). It gained prominence with the rise of knowledge-based assets, initially quantified as the difference between market and accounting values (Brennan & Connell, 2000). Gary Becker’s modernization of the human capital (HC) concept in 1993 reignited academic interest in HC (Nyberg & Wright, 2015). The resource-based view (RBV) paradigm shifted focus from physical and financial resources to intangible assets (Abeysekera, 2021; Spender, 1996), positioning IC as a strategic resource for emerging technological ventures (Juma & McGee, 2006).

This study defines IC as an organization’s intangible assets, based on Stewart’s (1997) concept of IC as ‘packaged useful knowledge.’ These assets include employee knowledge, adaptability, customer and supplier relationships, brands, intellectual property, product trade names, internal processes, and R&D capabilities. Although not listed in traditional financial statements, these assets create future value and competitive advantage. IC often shows values three to four times higher than their book values (Edvinsson & Malone, 1997).

The three dimensions of intellectual capital in entrepreneurship

Bontis (1998) suggests a research framework with three dimensions of intellectual capital (IC): human, social, and structural. This framework, which views IC as valuable interconnected elements, explains IC’s dimensions (Marr & Moustaghfir, 2005). It also enables the empirical examination of IC components’ impact on performance (Felício et al., 2014).

Human capital (HC) attributes, such as education and experience, are associated with small business success (Baptista et al., 2014). Financial intermediaries and venture capital firms value entrepreneurial experience highly when assessing startups, using managerial skills and experience as primary selection criteria (Piva & Rossi-Lamastra, 2018). HC is crucial in knowledge-based companies (Bosma et al., 2004), and the value of specific human capital is evident in new business founders’ entrepreneurial experience, especially among habitual entrepreneurs who have previously founded at least one business (Baptista et al., 2014).

Relational capital (RC), also known as social capital (SC), is an intangible asset that values relationships. It involves cultivating, preserving, and enhancing quality relationships with individuals, organizations, or groups that impact business performance (Welbourne & Pardo-del-Val, 2009). RC includes knowledge from relationships with stakeholders such as customers, suppliers, and industry associations, which influence the organization, add value, and strengthen operations. These relational networks are crucial business resources, enabling entrepreneurs to access otherwise unavailable resources (Bandera & Thomas, 2018; Burt, 2017). A significant aspect of SC is the reputation, experience, and contacts that facilitate entrepreneurs’ access to financing (Baum & Silverman, 2004). New ventures can improve their financing conditions through effective communication with investors and customers (Gardner & Avolio, 1998).

Structural capital (STC) is recognized in the literature as the company’s internalized knowledge. It pertains to the organizational structure and systems that bolster employee productivity (Edvinsson & Malone, 1997). It encompasses all non-human intangible assets of an organization, including culture, philosophy, internal processes, information systems, databases, organizational charts, process manuals, software, planning, strategies, routines, technology, and intellectual property rights such as patents, trademarks, and copyrights. The value of these assets to the company surpasses their material worth (Abdulaali, 2018). Intellectual property is often the only source of competitive advantage for knowledge-based companies (McGee & Dowling, 1994). Structural capital focuses on organizational efficiency, and its value derives from internal infrastructure, processes, and culture on the one hand and from the adaptive and development strategies adopted by the company on the other (Brennan & Connell, 2000).

Impact of intellectual capital on the performance of startups: Empirical evidence

The resource-based view (RBV) theory highlights human capital as a crucial determinant of firm performance (Barney et al., 2001). HC, characterized by knowledge, is both valuable and challenging to replicate. Studies have demonstrated a positive correlation between knowledge-based intangibles and performance (Davidsson & Honig, 2003; Kellermanns et al., 2016).

Coff (1997) provided moderate evidence supporting HC as a strategic resource. The presence of contradictory findings could be attributed to factors such as path dependence, the inability of cross-sectional studies to capture delayed effects, and the efficiency of the labor market for specific forms of HC (Coff, 1997).

In the context of human capital, both general and specific forms significantly impact a startup’s performance (Cressy, 1996; Gimmon & Levie, 2010). Bosma et al. (2004) investigated the effects of three types of investments - general, industry-specific, and entrepreneurship-specific - on startup survival, profitability, and employment. Their study found that these targeted investments substantially improve these performance metrics.

Research on the impact of initial intellectual capital accumulation on the performance and survival of emerging ventures, especially during the pre-seed phase and within high-impact acceleration programs, is scarce. Most studies focus on startups in developed countries and specific industries (Azeem & Khanna, 2023). This necessitates further validation across a broader spectrum of startups.

Intellectual capital, including knowledge, skills, and experience, is crucial for a startup’s success, particularly in the pre-seed phase. However, current research inadequately addresses this, especially for high-impact startups and those in acceleration programs. Most studies are limited to developed countries, leaving a knowledge gap about startups in diverse geographical contexts. They also tend to focus on specific sectors, missing the broader startup ecosystem (Andreeva & Garanina, 2016). Therefore, expanding research to include startups from various locations, sectors, and development stages is essential to understanding how intellectual capital affects startup performance and longevity.

The nature of the problem under study

Our research focuses on startups, which are key drivers of innovation and economic growth. We aim to investigate how initial financial resources and intangible assets, collectively known as intellectual capital (IC), impact a startup’s development during the crucial pre-seed phase. This phase involves setting business objectives, identifying potential hurdles, establishing market positions, and devising strategic plans.

We particularly focus on emerging ventures seeking financial aid and expert advice through accelerator programs. Our goal is to examine the correlation between IC - which includes the founding team’s skills, knowledge, experience, relationships, and capabilities - and the survival rate of nascent for-profit ventures.

We define ‘startups’ and ‘nascent for-profit ventures’ as organizations created in volatile environments to seize new market opportunities. Our primary goal is to determine how a founder’s IC influences the survival prospects of these ventures.

Our key research question is: “How does the initial allowance of intellectual capital of startups influence their survival rate?” Answering this question is crucial as it highlights the role of IC in determining a startup’s future.

Hypothesis statement

Our research focuses on startups in accelerator programs within the EDP sample, emphasizing the intellectual capital (IC) provided by founders. We hypothesize that this initial IC positively influences startups’ survival probabilities during the pre-performance phase, providing a competitive advantage in business navigation, investment acquisition, and survival.

To validate our hypothesis, we use a logistic regression model to quantify the impact of numerous factors on the survival probabilities of startups in our sample and predict their success likelihood during the critical pre-performance phase.

We aim to deepen the understanding of IC’s role in startup success, particularly within accelerator programs across diverse geographical and socio-demographic contexts. The findings could significantly influence founders, investors, and policymakers in designing programs that support and nurture emerging ventures.

MATERIALS AND METHODS

This research examines the influence of initial intellectual capital (IC) intangibles on startups during the pre-performance phase. The startups, part of a subset that applied to accelerator programs, were sourced from the Entrepreneurship Database Program (EDP) with data collected via surveys.

The sample

EDP characteristics

This study analyzes data from a global pool of entrepreneurs who applied to impact-focused accelerators between 2013 and 2019. The data, gathered by Emory University’s Entrepreneurship Database Program (EDP), include application information and biannual follow-up survey results. The EDP compiled a dataset of 14,457 emerging for-profit ventures after removing duplicates and incomplete surveys. These ventures applied to around 370 programs run by over 130 organizations, with half based in the United States, Mexico, India, and Kenya. Approximately 68% operate in countries classified as low to upper-middle-income by the World Bank.

The EDP collected data at the application stage and a year later from both successful and unsuccessful applicants. The surveys, split into two sections, contain 91 questions. The initial section includes contact information, entrepreneurship details, impact metrics, operating model, financing, founding partners’ characteristics, and understanding of new venture accelerators’ benefits. The follow-up section gathers information about entrepreneurship goals, impacts, financial and operational details, financing, and involvement in new venture accelerator programs. The application data offers preliminary insights into the ventures, founding teams, and pre-program performance.

Key issues for ventures in the sample

Our analysis of the EDP sample, which includes 14,457 for-profit ventures from 164 countries, reveals a strong social orientation and success biases. Ventures that have been operational for at least three years show a survival rate of 31% at the time of application, with over half generating revenue and 78% expanding their workforce beyond the founding members. Notably, 58% of these companies operate on proprietary technology.

About one-third of these ventures have secured external equity investment, while a quarter have taken on debt for startup expenses. Philanthropic contributions support a larger portion. Ventures led by female founders are less likely to secure equity investments but have a higher likelihood of having positive revenues in the preceding year. Over 10% of the ventures in the sample are directed by women.

Ventures led by experienced entrepreneurs or those with previous company-founding experience tend to attract more equity investments and report revenues and employees in the preceding year. Similarly, ventures with founders who hold patents, copyrights, or trademarks also show a higher tendency to attract equity investments and report revenues and employees in the preceding year.

However, as expected, the sample may exhibit a selection bias, as program selectors often favor ventures with more established records (Hallen et al., 2020). Participants in these programs are significantly more likely to report revenues in the preceding year (GALI, 2020, 2021).

Procedures, variables, and models

Analysis of startups’ initial IC intangibles allocation and surrounding economic conditions

We performed an exploratory factor analysis (EFA) to examine the initial operational conditions of startups in our dataset. This analysis accounted for both country and startup conditions. We aimed to understand the interplay between specific economic conditions, the venture’s operations, and the initial distribution of founders’ intangible intellectual capital. Following the work of Bontis (1998), we sought to identify these factors in our dataset and evaluate their impact on the startups’ survival probabilities.

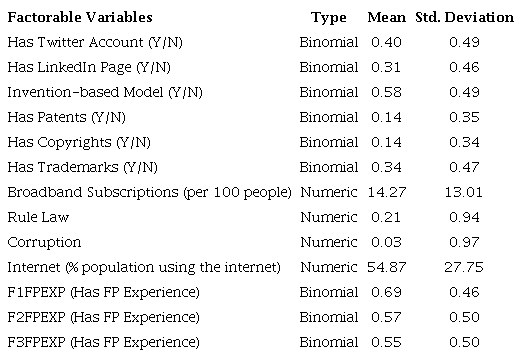

We chose 13 variables from two primary sources: the World Bank Development Indicators (WDI) and the Entrepreneurship Database Program at Emory University (EDP). The WDI supplied four variables that mirror the economic conditions of each country, including broadband subscriptions, control of corruption, rule of law, and internet usage as a percentage of the population (World Bank, 2023). The EDP provided nine variables associated with the initial allocation of founders’ intellectual capital intangibles. These variables included factors like the founders’ previous for-profit experience, the venture’s social media presence, and ownership of patents, inventions, copyrights, and trademarks. Table 1 presents the descriptive statistics for these variables.

Note. N: 14,457. Source: Own calculations.

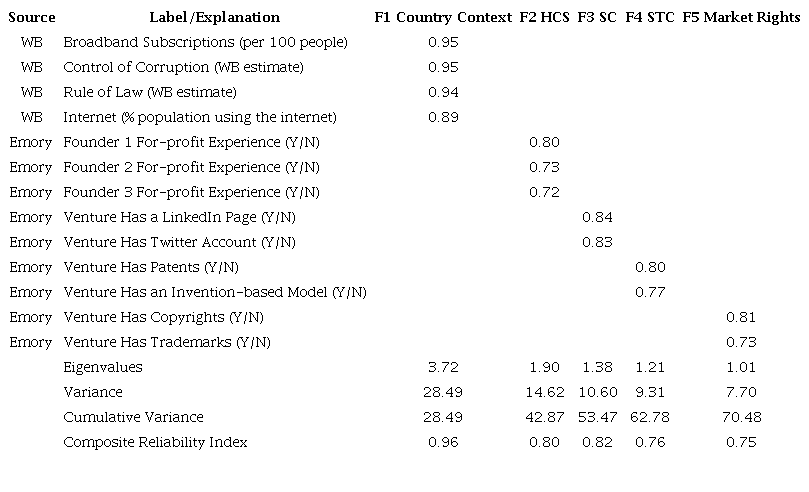

The analysis identified five primary factors (Table 2): F1 - country context (economic, infrastructure, and legal conditions), F2 - specific human capital (founders’ entrepreneurial experience), F3 - social capital (social networks), F4 - structural capital (patents or invention-based models), and F5 - market rights (trademarks or copyrights). While product innovation often results in patents and copyrights, the analysis initially differentiated between structural capital and market rights. However, these two components can be associated with organizational capital, which includes copyrights, patents, procedures, rules, and decision-making aids (Abdulaali, 2018).

Note. For interpretative purposes, variables with factor loadings below 0.5 were not included in the report. Extraction method: Principal component analysis. Rotation Method: Varimax with Kaiser normalization. Source: WB = World Bank Development Indicators; Emory = Emory Entrepreneurship Database applications surveys.

The test results confirm the suitability of the factor analysis. The composite reliability indices exceed the recommended threshold of 0.7. The Kaiser-Meyer-Olkin measure, which evaluates the sample’s adequacy, achieved a value of 0.70, surpassing the suggested minimum of 0.6. This suggests that the sample is appropriate for factor analysis. Bartlett’s test for sphericity was statistically significant, with a p-value less than 0.001. The five components extracted, detailed in Table 2, account for 70% of the total variance. Notably, factors 2 through 5 align with the IC classification criteria according to existing literature.

Variables in the logistic regression model

The two most frequently used non-financial startup performance measures are ‘survival’ (Adams et al., 2019; Brüderl & Preisendörfer, 1998; Mas-Verdú et al., 2015; Wamba et al., 2017) and ‘growth’ (Haeussler et al., 2019; Vanderstraeten et al., 2016). To provide empirical validation for our research question and working hypotheses, we selected ‘survival’ as our dependent variable (DV), a binomial variable that takes the value of 1 if the startup remains in operation three years after its inception and 0 otherwise (Hyytinen et al., 2015).

Regarding our predictive variables, we focus on the influence of the founding teams’ IC intangibles on the startups’ likelihood of survival, as categorized by three types: human capital, organizational or structural capital, and social capital (Bontis, 1998; Wang & Chang, 2005; Yang & Lin, 2009).

Our logistic regression model integrates the initial intellectual capital endowments, utilizing principal components extracted from an exploratory factor analysis (Aguilera et al., 2006). The resulting variables are ‘F2 SHC experience’, which reflects the founding team’s for-profit venture experience; ‘F3 SC media presence’ (Bandera & Thomas, 2018), indicating the entrepreneur’s network via LinkedIn and Twitter (Song & Vinig, 2012), and two components, ‘F4 STC innovation’ and ‘F5 market rights’ (Alvarez-Salazar & Seclen-Luna, 2023), related to the venture’s structural or organizational capital, covering aspects like intellectual assets, databases, organizational culture, structure, patents, and trademarks (Abdulaali, 2018).

New business survival hinges on three-factor categories: personal, business-specific, and environmental (Brüderl et al., 1992). We consider a range of these factors, including external economic conditions, team dynamics, and venture specifics, to study the effect of a venture’s initial intellectual capital (IC) endowment. Acknowledging their influence on survival probability, we use these factors as control variables in our analysis.

The ‘F1 country context’ factor includes country-specific variables (economic context) derived from World Bank Indicators (WBI). These variables reflect the national economic environment faced by startups. Additionally, ‘startup density,’ as defined by the World Bank (2021), signifies the number of newly registered corporations per 1,000 individuals aged 15-64, offering insight into the entrepreneurial ecosystem.

In terms of firm or venture founding team characteristics in our sample, we include the variable ‘female presence,’ which denotes the degree of female representation or influence in a venture’s founding team. Women’s entrepreneurship plays a significant role in a country’s economic growth, particularly in developing economies (Cardella et al., 2020). In this study, if women constitute two-thirds or more of the founding team, it is considered to exhibit strong female dominance (Barnir, 2014).

Regarding the influence of finances on survival probabilities in the face of financial constraints (Fuertes-Callén et al., 2022; Lee & Zhang, 2011; Wamba et al., 2017), we include two categorical variables ‘has equity’ and ‘has debt’. These variables are coded as follows: 1 signifies that the venture has obtained equity/debt financing either at its inception or in the year following the application; 2 means that the venture has secured financing on both occasions; 0 is used when the venture has not received any such financing. To gain a deeper understanding of the effect of specific financial goals on performance, we incorporate the concept of exhibiting a distinct profit margin, serving as a financial planning proxy (Miner & Raju, 2004) based on the foundational startup survival studies by Cressy (1996). The ‘has target margin’ variable is binary, with a value of 1 assigned if the venture operates with a predetermined target margin and 0 if not.

Business accelerators significantly contribute to the facilitation of new venture creation. Startups seek top-tier accelerators to expedite their developmental journey (Salamzadeh & Markovic, 2018). These accelerators provide early-stage funding and essential mentorship, driven by their confidence in the startup’s potential, personal interest in the concept, or admiration for the entrepreneurial team (Radojevich-Kelley & Hoffman, 2012). The characteristics of accelerator programs are known to influence venture performance. Although we cannot explicitly measure specific accelerator characteristics, we will account for program-specific unobserved heterogeneity in our subsequent analyses, thereby indirectly accommodating program differences.

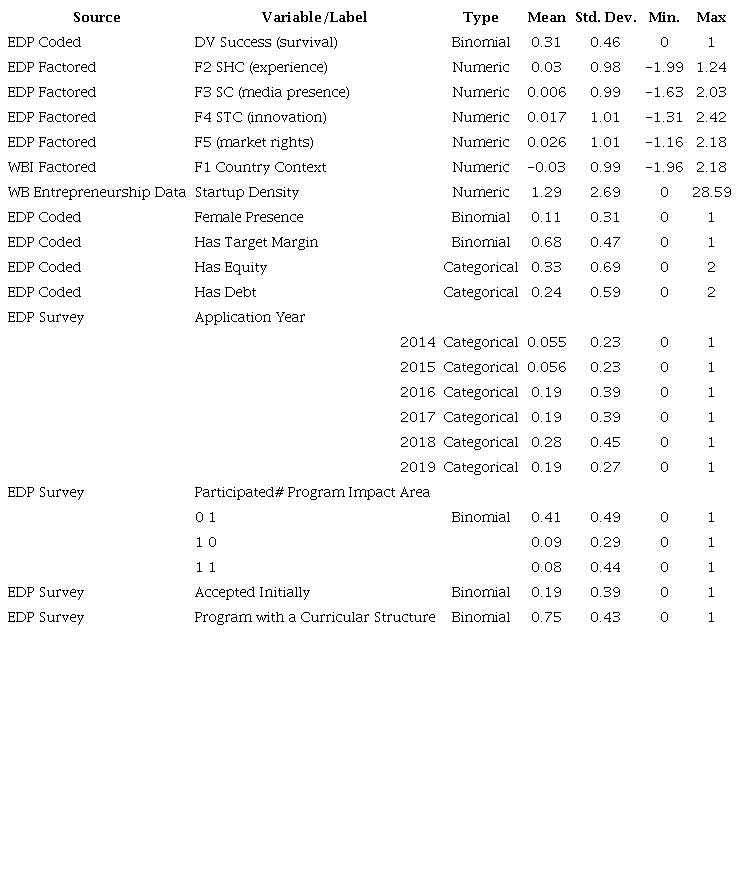

The EDP examines several variables for accelerator program characteristics. These include ‘application year’ (the submission year of the venture’s application); this variable accounts for temporal variations and the impact of learning over time, and partly alleviates the effect of unobserved heterogeneity; participated - ventures that completed the program (GALI, 2021); ‘accepted initially’ - ventures initially selected into the program; ‘program impact area’ - whether the program has a specific impact area (Lall et al., 2020); and ‘program with curriculum structure’ - whether the program provides a structured curriculum to participants (Kramer et al., 2023). Table 3 exhibits the descriptive statistics for the variables in the LR model.

Note. Binomial Variables are assigned a value of 1 when present and 0 when absent. The Application Year represents the survey year. For Equity/Debt Presence, categorical variables are assigned as follows: a value of 1 is given if an investment is present either at inception or at the end of the last calendar year, a value of 2 is given if an investment is present at both inception and the end of the last calendar year, and a value of 0 is given in all other cases.

Estimation techniques

For the validation of our hypothesis, we use a logarithmic regression model (LR), which is considered suitable when the response variable is dichotomous, and the effect of predictors is linear. Our LR model relies on the reduced-form model: y_i = π_i + ε_i ,i =1,…,n, where π_i is the expected value of Y given (X_1 = x_i1, X_2 = x_i2, … ,X_p = x_ip) (Aguilera et al., 2006). In this case, Y is the probability of survival as a function of a set of available information about the ventures. The analysis of the effects of the dimensions of IC over success as they are operationalized requires a technique that adequately manages the probabilities of attaining a successful performance. Logistic regression (LR) is the appropriate technique when dealing with the relationship between a dichotomous outcome and a set of explanatory variables.

When an LR model estimates a binary response outcome, we assume that its logit transformation has a linear relationship with the predictor variables. Thereby the relationship between the response variable and its covariates is interpreted through the odds ratio from the parameters of the models. Measured in odds ratio (OR), if the parameter in the regression is positive, the OR > 1, and if it is negative OR < 1, indicating the effect of the IV on the chances of survival. The logistic regression model can be written as in Equation 1:

The binary response variable Y is either 0 or 1, and E(Y_1 |Χ_1i, Χ_21, …, Χ_k1). Then π(Χ_1, Χ_2, …, Χ_k) is interpreted as P(Y=1) for a given combination of values of the predictor variables Χ_1, Χ_2, …, Χ_k. We express the model as: 〖Y=π (Χ〗_1, Χ_2, …, Χ_k)+ϵ where ϵ, could only assume two values depending on whether Y is equal to zero or one. The left-hand side of Equation 1 is the log odds ratio, that is, the logarithm of the odds that Y will equal 1, for a given combination of the predictor variables. Our estimation uses the maximum likelihood (ML) method.

The proposed model

To validate our hypothesis, the following logistic regression model (LR) is proposed.

RESULTS FROM THE LR MODEL

Academic literature identifies several factors influencing the survival of new companies in their pre-performance phase (Santisteban & Mauricio, 2017; Strotmann, 2007). Our research focused on understanding the impact of recognized intangible intellectual capital (IC) dimensions on this survival. We integrated these variables into our logistic regression (LR) model to mitigate potential confounding effects. This method aimed to distinctly assess the influence of IC dimensions on survival, thus facilitating the effective validation of our working hypothesis.

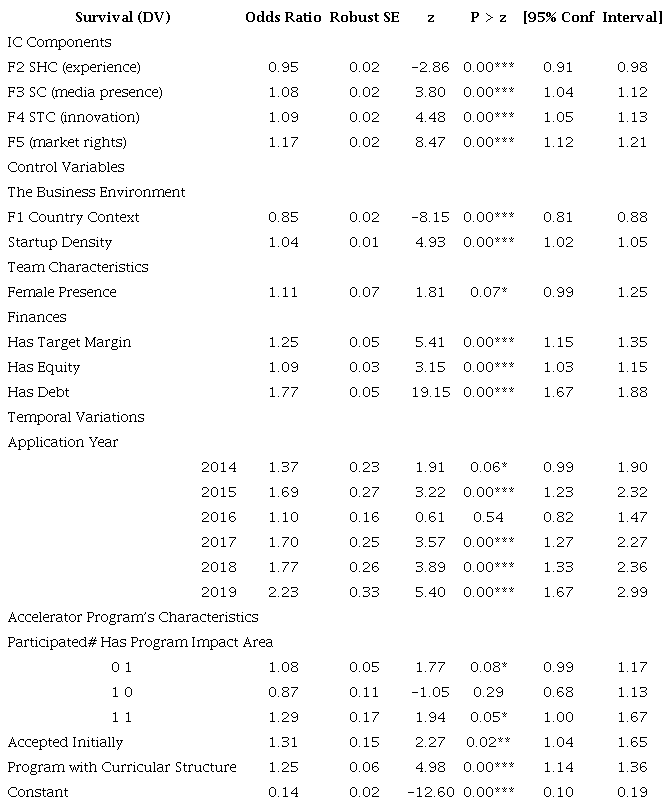

Table 4 shows the results of the logistic regression (LR) model, which we used to test our hypothesis. This hypothesis proposes a positive link between the initial intellectual capital of the founding team and the longevity of the startups in our sample.

Note. *** p < .01, ** p < .05, * p < .10; Robust SE = Robust standard errors. Source: Own elaboration.

The resulting LR model

The model’s results, expressed in terms of odds ratios (expb), are as follows:

The estimated odds ratios exhibit significance at the 1% level, except for the accelerator program-related variable ‘accepted initially’, which demonstrated significance at the 5% level. Furthermore, the variables ‘year 2014’, ‘female dominance in the founding team’, and the interaction between the variables ‘participated#’ program with ‘impact area’ [1 1] and [0 1] were significant at the 10% level.

To identify specification errors in the logistic regression (LR) model, we executed a link test, which was not deemed significant at the 5% level. The Hosmer-Lemeshow goodness-of-fit test validated the appropriateness of the LR model for explaining ‘survival,’ with a chi-square statistic of 13.10 (df = 8) and a probability exceeding the chi-square value of 0.11. The McFadden R-squared value for the LR model was determined to be 0.054. The potential issue of multicollinearity in the LR model was investigated and subsequently dismissed; the individual variance inflation factors (VIF) were significantly below the accepted threshold of 10, and the mean VIF was observed to be 2.17.

By employing a logistic regression (LR) model, we were able to measure the influence of various independent variables, including control factors, on the survival probabilities of startups in the EDP sample. This also resulted in a predictive model that can be used to determine the likelihood of success for a startup during its pre-performance phase. The model correctly classified 70.1% of the companies that survived. It had a sensitivity of 16.07%, indicating its ability to correctly identify successful startups, and a specificity of 94.68%, reflecting its ability to correctly identify unsuccessful startups. The probability cutoff point was approximately 0.28, and the area under the receiver operating characteristic (ROC) curve, which incorporates all thresholds, was 66%.

Discussion

Our analysis, consistent with other studies, highlights the crucial role of project financing in determining the survival probabilities of startups. Specifically, in our sample, easing financial constraints and the presence of a financing project jointly enhance a startup’s chances of survival during the pre-performance phase. These findings align with those of Åstebro and Bernhardt (2003), who identified bank loans as a positive predictor of startup survival.

In their seminal work, Cooper et al. (1994) demonstrated that the total amount of capital invested by the time of the first sale positively impacts the growth and survival of new ventures. The literature widely acknowledges the significance of startup capital for fledgling firms in their early formation stages (Cabral & Mata, 2003; Figueroa-Armijos, 2019). In a broader geographical context, our empirical evidence suggests that the most impactful control factors are intrinsically linked to the easing of these financial constraints. During the pre-performance phase, ventures that have procured financing either through external equity (has equity) or debt agreements (has debt), at inception, in the preceding year, or both instances, demonstrate a survival likelihood higher by 9% and 77%, respectively, compared to those constrained by external financing. These results align with other studies that acknowledge the positive effect of debt financing obtained in the name of the firm, which is associated with longer survival times and higher revenues (Cole, 2018). Additionally, financial planning, identified in the sample as having a pre-determined profit margin, increases the likelihood of a venture’s survival by 25%, as substantiated by the literature (Cressy, 1996; Miner & Raju, 2004).

Our research underlines the significant role of accelerator programs, particularly those with a well-structured curriculum, in enhancing the survival probabilities of startups. We observed increases of 31% and 25%, respectively, for both factors. These results align with the findings of Kramer et al. (2023). By including these variables in our model, we were able to mitigate the known selection bias associated with accelerator programs (GALI, 2020). Furthermore, we found a nonlinear interaction effect between variables indicating program completion and focus on a specific impact area. Notably, when both indicators are present, the survival probabilities of the venture increase by 29%. This is consistent with the findings of Venâncio and Jorge (2022), who found that accelerated startups have higher external equity ratios than non-accelerated startups; this was observed after accounting for firm-specific differences and unobserved startup factors, thereby enhancing their survival and growth probabilities, and those related to the positive effect of entrepreneurial focus of EDP’s participating accelerator programs on high-impact projects (GALI, 2021; Lall et al., 2020).

By introducing a temporal variable in our model, we were able to account for variations in both the characteristics of ventures participating in acceleration programs and the independent variables, thus mitigating the effects of unobserved heterogeneity (Pourhoseingholi et al., 2012). Our findings indicate that the temporal effect significantly enhances survival probabilities, with an average annual increase of 10.2%. In the study, the time variable identifies a learning curve process, suggesting an increase in the efficacy of accelerator programs over time. Our results align with the findings of Hallen et al. (2020), who identified a sorting dynamics mechanism within accelerators, resulting from extensive, intensive, and paced consultation. This implies that the knowledge gained from early programs about ventures can be applied in a beneficial and potentially replicable manner. Such practices may hold relevance not only for independent entrepreneurs but also for educational programs and corporate innovation.

The study reveals that the wider economic environment, measured by WDI variables, reduces survival probabilities by 15%. Although emerging countries are well-represented in the sample, the EDP primarily characterizes the entrepreneurial ecosystem in developed nations, particularly the United States. Contrary to the results of Strotmann (2007) in Germany and Box (2008)in Sweden, this finding suggests a diminished role of the overall economic context in our study, opening avenues for future research to explore the operational dynamics of startups and accelerators in various country groups.

Geroski et al. (2010) highlight that business population density, or the number of firms in the market, significantly impacts market conditions for newcomers. The specific effect of the entrepreneurial ecosystem becomes prominent during the pre-performance phase of ventures in the EDP sample. In nations with a robust ecosystem, survival probabilities rise by 4%, as indicated by the World Bank’s Startup Density indicator.

After assessing the influence of external and internal variables from the EDP sample, we now examine how initial IC inventories affect startup survival probabilities. These inventories include human capital, social capital, and structural or organizational capital. Our primary focus is to validate the hypothesis that founding teams’ initial intangible IC assets enhance survival probabilities during the pre-performance phase.

According to our estimates, the SC assets identified by the F3 SC (media presence) factor increase survival probabilities by 8%. This result is generally consistent with the studies of Bandera and Thomas (2018), and specifically aligns with the findings of Song and Vinig (2012), who associate positive performance in the initial stages of ventures with expanded social media networks, particularly on LinkedIn and Twitter.

The structural or organizational capital (STC), identified as F4 STC (innovation) in the EDP sample, increases survival probabilities by 9%, as indicated by variables such as patent ownership and the adoption of invention-based models. This finding aligns with studies by Power and Reid (2021) and Patel and Pearce (2018) in the retail sector, and with the fact that 58% of ventures in the sample adopt an innovation-based business model (GALI, 2020). It also corresponds with the natural selection bias of acceleration programs in our sample (Radojevich-Kelley & Hoffman, 2012) and supports the idea that most accelerators seek concepts with large upside potential that can be scaled to meet national or global demand (Hallen et al., 2020).

In line with the F5 factor (market rights), owning copyrights and trademarks enhances a venture’s survival chances by 17%. This aligns with Abdulaali’s (2018)findings, which highlight the positive impact of structural capital components on survival. It also reflects the sample composition, where 33% of the studied ventures possess trademarks and 13% have copyrights.

Although the founding team’s experience in creating previous for-profit ventures was significant in the model, it did not positively influence the survival probabilities of ventures in the sample, reducing them by 5%. This contrasts with the notion that founders’ capabilities, such as education and industry experience, positively affect startup performance (Bosma et al., 2004; Brüderl et al., 1992; Geroski et al., 2010). One explanation is de Jong and Marsili’s (2015) finding that founders only experience positive impacts if they take over an existing business or spend significant time at the startup. However, we lean toward Keogh and Johnson’s (2021) findings, which suggest nonlinearities and possible moderating and mediating effects in the HC effect on startup survival, due to interactions between financing and specific human and social capital attributes of the founders. Moreover, close-tie inspiration negatively impacts founders with prior entrepreneurial experience, highlighting the need for new firm survival studies to model contingency variables better. Our findings open possibilities for future studies on more specific conditions with entrepreneurs.

After accounting for control variables, we were able to concentrate on our primary research objective. The empirical evidence, encompassing a wider geographic and demographic context, validated our general hypothesis. This demonstrated the positive impact of the three dimensions of intellectual capital (IC) as recognized in the existing literature and identified in the EDP sample. These dimensions, represented by the intellectual capital assets of the founding teams, significantly influence survival probabilities during the pre-performance phase, effectively bridging the geographical gap of single-country or industry-specific context studies.

CONCLUSION

This research builds on previous studies to examine the influence of initial intellectual capital (IC) on the survival probabilities of new ventures in accelerator programs, as surveyed by the EDP. It confirms the beneficial impact of IC assets on their survival, a crucial success indicator for new ventures in the pre-performance phase, as highlighted by Unger et al. (2011) and Sardo and Serrasqueiro (2019).

Most existing studies on startup survival have been confined to advanced economies or industry-specific contexts and have employed a single theoretical approach (Azeem & Khanna, 2023). This research, however, bridges geographic and business orientation gaps by highlighting the significance of initial IC for startups in various globally oriented impact accelerator programs. Additionally, the study integrates the perspectives of the resource-based view (RBV) and human capital theory. Both perspectives emphasize the positive effect of initial human capital on startup survival, where the key explanatory variables relate to the value of useful and encapsulated knowledge as an intangible asset, which serves as a source of longevity and potentially better performance.

The analysis shows that these IC accumulations, encapsulating useful and applicable knowledge identified in surveys, enhance the survival prospects of startups in the EDP sample. This enhancement remains even after accounting for potential unobserved heterogeneity and considering both external and internal influences on startup operations. By examining the role of initial IC in a diverse range of early-stage ventures in global acceleration programs, the research expands our understanding of startup survival determinants and broadens its scope to encompass emerging economies and diverse accelerator programs.

Our findings are not just a result but a starting point for further research. Future studies using the EDP information will analyze the impact of knowledge intangibles on survival probability under specific conditions, including socio-demographic coverage, heterogeneity of acceleration programs, founding team composition, diversity, operational sectors, size, funding source diversity, and differentiated effects. They will also consider the contribution to the development of the countries where they operate and the innovation processes generated from their operation.

Additionally, there is a significant opportunity for complementing this research. Due to the scarcity of studies analyzing the mediating and moderating effects of IC components on performance, future research will consider these complementary effects (Delmar & Shane, 2006), particularly the relationships between human capital and financial constraints as suggested by the research of authors such as Unger et al. (2011), Keogh and Johnson (2021), and Salamzadeh et al. (2023). The lack of interaction studies in this area highlights a gap in the literature, presenting a valuable avenue for future exploration to better understand these dynamics.

Implications of the study

By implementing these practical strategies, startup founders can better navigate the challenges of the initial stages and improve their chances of long-term success. Our study underscores the importance of early recognition and investment in key factors such as intellectual capital (IC), financial planning, and participation in accelerator programs for startup founders. By prioritizing the development of IC assets, including the knowledge and skills of the founding team, startups can build a solid foundation for navigating the early stages. Securing diverse funding sources and establishing clear financial goals from the outset can further mitigate financial constraints and improve survival probabilities.

Engaging in well-structured accelerator programs offers valuable resources, mentorship, and networking opportunities, enhancing the startup’s resilience and performance. Our research contributes to this understanding by demonstrating that these elements significantly influence startup survival, particularly in diverse and globally oriented contexts. By recognizing and leveraging these critical factors early on, founders can better position their ventures for long-term success and growth, adapting to challenges and capitalizing on opportunities as they arise.

For policymakers and accelerator program developers, our findings provide valuable insights for refining selection processes and program development. Leveraging data from the EDP and the predictive strength of our logistic regression (LR) model, we offer preliminary guidance for creating more effective mentoring and support initiatives. The clear distinction between the values of specificity and sensitivity in our LR model indicates that survival and failure probabilities are independent entities, challenging traditional assumptions and uncovering new research opportunities. Further investigation into these factors can enhance the efficacy of support initiatives, benefiting the startup ecosystem by fostering more resilient and successful ventures.

REFERENCES

Abdulaali, A. (2018). The impact of intellectual capital on business organizations. Academy of Accounting and Financial Studies Journal, 22(6), 1-16. https://www.abacademies.org/articles/the-impact-of-intellectual-capital-on-business-organisation-7630.html

Abeysekera, I. (2021). Intellectual capital and knowledge management research towards value creation. From the past to the future. Journal of Risk and Financial Management, 14(6), 238. https://doi.org/10.3390/jrfm14060238

Adams, P., Fontana, R., & Malerba, F. (2019). Linking vertically related industries: Entry by employee spinouts across industry boundaries. Industrial and Corporate Change, 28(3), 529-550. https://doi.org/10.1093/icc/dtz014

Aguilera, A., Escabias, M., & Valderrama, M. (2006). Using principal components for estimating logistic regression with high-dimensional multicollinear data. Computational Statistics & Data Analysis, 50(8), 1905-1924. https://doi.org/10.1016/j.csda.2005.03.011

Alvarez-Salazar, J., & Seclen-Luna, J. (2023). To survive or not to survive: Findings from PLS-SEM on the relationship between organizational resources and startups’ survival. In Partial Least Squares Path Modeling: Basic Concepts, Methodological Issue and Applications (pp. 329-374).

Andreeva, T., & Garanina, T. (2016). Do all elements of intellectual capital matter for organizational performance? Evidence from Russian context. Journal of Intellectual Capital, 7(2), 397-412. https://doi.org/10.1108/JIC-07-2015-0062

Åstebro, T., & Bernhardt, I. (2003). Start-up financing, owner characteristics, and survival. Journal of Economics and Business, 55(4), 303-319. https://doi.org/10.1016/S0148-6195(03)00029-8

Audretsch, D., Keilbach, M., & Lehmann, E. (2006). Entrepreneurship and economic growth. Oxford University Press.

Azeem, M., & Khanna, A. (2023). A systematic literature review of startup survival and future research agenda. Journal of Research in Marketing and Entrepreneurship, 26(1), 111-139. https://doi.org/10.1108/JRME-03-2022-0040

Bandera, C., & Thomas, E. (2018). The role of innovation ecosystems and social capital in startup survival. IEEE Transactions on Engineering Management, 66(4), 542-551. https://doi.org/10.1109/TEM.2018.2859162

Baptista, R., Karaöz, M., & Mendonça, J. (2014). The impact of human capital on the early success of necessity versus opportunity-based entrepreneurs. Small Business Economics, 42, 831-847. https://doi.org/10.1007/s11187-013-9502-z

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 33-120. https://doi.org/10.1177/014920639101700108

Barney, J., Wright, M., & Ketchen Jr., D. (2001). The resource-based view of the firm: Ten years after 1991. Journal of Management, 27(6), 625-641. https://doi.org/10.1016/S0149-2063(01)00114-3

Barnir, A. (2014). Gender differentials in antecedents of habitual entrepreneurship: Impetus factors and human capital. Journal of Developmental Entrepreneurship, 19(1), 1-22. https://doi.org/10.1142/S1084946714500010

Baum, J., & Silverman, B. (2004). Picking winners or building them? Alliance, intellectual, and human capital as selection criteria in venture financing and performance of biotechnology startups. Journal of Business Venturing, 19(3), 411-436. https://doi.org/10.1016/S0883-9026(03)00038-7

Becker, G. (1964). Human capital: A theoretical and empirical analysis with special reference to education. National Bureau of Economic Research.

Becker, G. (1994). Human capital revisited. In Human capital: A theoretical and empirical analysis with special reference to education. The University of Chicago Press.

Beckman, C., & Burton, M. (2008). Founding the future: Path dependence in the evolution of top management teams from founding to IPO. Organization Science, 19(1), 3-24. https://doi.org/10.1287/orsc.1070.0311

Bontis, N. (1998). Intellectual capital: An exploratory study that develops measures and models. Management decision, 36(2), 63-76. https://doi.org/10.1108/00251749810204142

Bosma, N., Van Praag, M., Thurik, R., & De Wit, G. (2004). The value of human and social capital investments for the business performance of startups. Small Business Economics, 23, 227-236. https://doi.org/10.1023/B:SBEJ.0000032032.21192.72

Box, M. (2008). The death of firms: Exploring the effects of environment and birth cohort on firm survival in Sweden. Small Business Economics, 31(4), 379-393. https://doi.org/10.1007/s11187-007-9061-2

Brennan, N., & Connell, B. (2000). Intellectual capital: Current issues and policy implications. Journal of Intellectual Capital, 1(3), 206-240. https://doi.org/10.1108/14691930010350792

Brüderl, J., & Preisendörfer, P. (1998). Network support and the success of newly founded businesses. Small business economics, 10, 213-225. https://doi.org/10.1023/A:1007997102930

Brüderl, J., & Schussler, R. (1990). Organizational mortality: The liabilities of newness and adolescence. Administrative Science Quarterly, 53(3), 530-547. https://doi.org/10.2307/2393316

Brüderl, J., Preisendörfer, P., & Ziegler, R. (1992). Survival chances of newly founded business organizations. American Sociological Review, 57(2), 227-242. https://doi.org/10.2307/2096207

Burt, R. (2017). Structural holes versus network closure as social capital. In R. Dubos (Ed.), Social capital (pp. 31-56). Routledge.

Cabral, L., & Mata, J. (2003). On the evolution of the firm size distribution: Facts and theory. American Economic Review, 93(4), 1075-1090. https://doi.org/10.1257/000282803769206205

Cardella, G., Hernández-Sánchez, B., & Sánchez-García, J. (2020). Women entrepreneurship: A systematic review to outline the boundaries of scientific literature. Frontiers in Psychology, 11, 1557. https://doi.org/10.3389/fpsyg.2020.01557

Coff, R. (1997). Human assets and management dilemmas: Coping with hazards on the road to resource-based theory. Academy of Management Review, 22(2), 374-402. https://doi.org/10.2307/259327

Cole, R. S. (2018). Debt financing, survival, and growth of start-up firms. Journal of Corporate Finance, 50, 609-625. https://doi.org/10.1016/j.jcorpfin.2017.10.013

Cooper, A., Gimeno-Gascon, F., & Woo, C. (1994). Initial human and financial capital as predictors of new venture performance. Journal of Business Venturing, 9(5), 371-395. https://doi.org/10.1016/0883-9026(94)90013-2

Cressy, R. (1996). Pre-entrepreneurial income, cash-flow growth and survival of startup businesses: Model and tests on UK data. Small Business Economics, 8, 49-58. https://doi.org/10.1007/BF00391975

Dahlqvist, J., Davidsson, P., & Wiklund, J. (2000). Initial conditions as predictors of new venture performance: A replication and extension of the Cooper et al. study. Enterprise and innovation management studies, 1(1), 1-17.

Davidsson, P., & Honig, B. (2003). The role of social and human capital among nascent entrepreneurs. Journal of Business Venturing, 18(3), 301-331. https://doi.org/10.1016/S0883-9026(02)00097-6

Del Sarto, N., Isabelle, D., & Di Minin, A. (2020). The role of accelerators in firm survival: An fsQCA analysis of Italian startups. Technovation, 90-91, 102102. https://doi.org/10.1016/j.technovation.2019.102102

Delmar, F., & Shane, S. (2006). Does experience matter? The effect of founding team experience on the survival and sales of newly founded ventures. Strategic Organization, 4(3), 215-247. https://doi.org/10.1177/1476127006066596

Dencker, J., Gruber, M., & Shah, S. (2009). Pre-entry knowledge, learning, and the survival of new firms. Organization Science, 20(3), 516-537. https://doi.org/10.1287/orsc.1080.0387

Edvinsson, L., & Malone, M. (1997). Intellectual capital: Realizing your company’s true value by finding its hidden roots. HarperCollins Publishers Inc.

Eisenhardt, K., & Schoonhoven, C. (1990). Organizational growth: Linking founding team, strategy, environment, and growth among US semiconductor ventures, 1978-1988. Administrative Science Quarterly, 35(3), 504-529. https://doi.org/10.2307/2393315

Felício, J., Couto, E., & Caiado, J. (2014). Human capital, social capital and organizational performance. Management Decision, 52(12), 350-364. https://doi.org/10.1108/MD-04-2013-0260

Figueroa-Armijos, M. (2019). Does public entrepreneurial financing contribute to territorial servitization in manufacturing and KIBS in the United States? Regional Studies, 53(3), 341-355. https://doi.org/10.1080/00343404.2018.1554900

Fuertes-Callén, Y., Cuellar-Fernández, B., & Serrano-Cinca, C. (2022). Predicting startup survival using first-year financial statements. Journal of Small Business Management, 60(6), 1314-1350. https://doi.org/10.1080/00472778.2020.1750302

Furlan, A. (2019). Startup size and pre-entry experience: New evidence from Italian new manufacturing ventures. Journal of Small Business Management, 57(2), 679-692. https://doi.org/10.1111/jsbm.12427

Gardner, W. L., & Avolio, B. J. (1998). The charismatic relationship: A dramaturgical perspective. Academy of Management Review, 23(1), 32-58. https://doi.org/10.2307/259098

Geroski, P., Mata, J., & Portugal, P. (2010). Founding conditions and the survival of new firms. Strategic Management Journal, 31(5), 510-529. https://doi.org/10.1002/smj.823

Gimmon, E., & Levie, J. (2010). Founder’s human capital, external investment, and the survival of new high-technology ventures. Research Policy, 39(9), 1214-1226. https://doi.org/10.1016/j.respol.2010.05.017

Global Accelerator Learning Initiative. (2020). The entrepreneurship database program at Emory University. https://www.galidata.org/assets/report/pdf/2019%20Year-End%20Summary.pdf

Global Accelerator Learning Initiative. (2021, May). Does accelerators work? https://www.galidata.org/assets/report/pdf/Does%20Acceleration%20Work_EN.pdf

Gruber, M., MacMillan, I., & Thompson, J. (2008). Look before you leap: Market opportunity identification in emerging technology firms. Management Science, 54(9), 1652-1665. https://doi.org/10.1016/j.respol.2010.05.017

Haeussler, C., Hennicke, M., & Mueller, E. (2019). Founder-inventors and their investors: Spurring firm survival and growth. Strategic Entrepreneurship Journal, 13(3), 288-325. https://doi.org/10.1016/j.respol.2010.05.017

Hallen, B., Cohen, S., & Bingham, C. (2020). Do accelerators work? If so, how? Organization Science, 31(2), 378-414. https://doi.org/10.1287/orsc.2019.1304

Hannan, M., & Freeman, J. (1977). The population ecology of organizations. American Journal of Sociology, 82(5), 929-964. https://doi.org/10.1086/226424

Hyytinen, A., Pajarinen, M., & Rouvinen, P. (2015). Does innovativeness reduce startup survival rates? Journal of Business Venturing, 30(4), 564-581. https://doi.org/10.1016/j.jbusvent.2014.10.001

Jong, J., & Marsili, O. (2015). Founding a business inspired by close entrepreneurial ties: Does it matter for survival? Entrepreneurship Theory and Practice, 39(5), 1005-1025. https://doi.org/10.1111/etap.12086

Juma, N., & McGee, J. (2006). The relationship between intellectual capital and new venture performance: An empirical investigation of the moderating role of the environment. International Journal of Innovation and Technology Management, 3(4), 379-405. https://doi.org/10.1142/S0219877006000892

Kellermanns, F., Walter, J., Crook, T., Kemmerer, B., & Narayanan, V. (2016). The resource-based view in entrepreneurship: A content-analytical comparison of researchers’ and entrepreneurs’ views. Journal of Small Business Management, 54(1), 26-48. https://doi.org/10.1111/jsbm.12126

Keogh, D., & Johnson, D. K. (2021). Survival of the funded: Econometric analysis of startup longevity and success. Journal of Entrepreneurship, Management, and Innovation, 17(4), 29-49. https://doi.org/10.7341/20211742

Kerrin, M., Mamabolo, M., & Kele, T. (2017). Entrepreneurship management skills requirements in an emerging economy: A South African outlook. The Southern African Journal of Entrepreneurship and Small Business Management, 9(1), 1-10. https://hdl.handle.net/10520/EJC-9bea7314e

Kimberly, J. (1979). Issues in the creation of organizations: Initiation, innovation, and institutionalization. Academy of Management Journal, 22(3), 437-457. https://doi.org/10.2307/255737

Kramer, A., Veit, P., Kanbach, D., Stubner, S., & Maran, T. (2023). A framework of accelerator design: Harmonizing fragmented knowledge. European Journal of Innovation Management, 27(8), 2780-2817. https://doi.org/10.1108/EJIM-11-2022-0668

Lall, S., Chen, L., & Roberts, P. (2020). Are we accelerating equity investment into impact-oriented ventures? World Development, 131, 104952. https://doi.org/10.1016/j.worlddev.2020.104952

Lee, J., & Zhang, W. (2011, Aug 12-16). Financial capital and startup survival. Academy of Management Proceedings, pp. 1-6. San Antonio, TX. https://ink.library.smu.edu.sg/lkcsb_research/7627

Marr, B., & Moustaghfir, K. (2005). Defining intellectual capital: A three-dimensional approach. Management Decision, 43(9), 114-1128. https://doi.org/10.1108/00251740510626227

Mas-Verdú, F., Ribeiro-Soriano, D., & Roig-Tierno, N. (2015). Firm survival: The role of incubators and business characteristics. Journal of Business Research, 68(4), 793-796. https://doi.org/10.1016/j.jbusres.2014.11.030

Mayer-Haug, K., Read, S., Brinckmann, J., Dew, N., & Grichnik, D. (2013). Entrepreneurial talent and venture performance: A meta-analytic investigation of SMEs. Research Policy, 42(6-7), 1251-1273. https://doi.org/10.1016/j.respol.2013.03.001

McGee, J., & Dowling, M. (1994). Using R&D cooperative arrangements to leverage managerial experience: A study of technology-intensive new ventures. Journal of Business Venturing, 9(1), 33-48. https://doi.org/10.1016/0883-9026(94)90025-6

Mincer, J. (1974). The human capital earnings function. In J. A. Mincer (Ed.), Schooling, Experience, and Earnings (pp. 83-96). NBER.

Miner, J., & Raju, N. (2004). Risk propensity differences between managers and entrepreneurs and between low-and high-growth entrepreneurs: A reply in a more conservative vein. Journal of Applied Psychology, 89(1), 3-13. https://doi.org/10.1037/0021-9010.89.1.3

Nyberg, A., & Wright, P. (2015). 50 years of human capital research: Assessing what we know, exploring where we go. Academy of Management Perspectives, 29(3), 287-295. https://www.jstor.org/stable/43822116

Patel, P. C., & Pearce II, J. A. (2018). The survival consequences of intellectual property for retail ventures. Journal of Retailing and Consumer Services, 43, 77-84. https://doi.org/10.1016/j.jretconser.2018.03.005

Picken, J. (2017). From startup to scalable enterprise: Laying the foundation. Business Horizons, 60(5), 587-595. https://doi.org/10.1016/j.bushor.2017.05.002

Piva, E., & Rossi-Lamastra, C. (2018). Human capital signals and entrepreneurs’ success in equity crowdfunding. Small Business Economics, 51, 667-686. https://doi.org/10.1007/s11187-017-9950-y

Pourhoseingholi, M., Baghestani, A., & Vahedi, M. (2012). How to control confounding effects by statistical analysis. Gastroenterol Hepatololy from Bed to Bench, 5(2), 79-83. https://pmc.ncbi.nlm.nih.gov/articles/PMC4017459/

Power, B., & Reid, G. C. (2021). The impact of intellectual property types on the performance of business start-ups in the United States. International Small Business Journal, 39(4), 372-400. https://doi.org/10.1177/0266242620967009

Pradhan, R., Arvin, M., Nair, M., & Bennett, S. (2020). The dynamics among entrepreneurship, innovation, and economic growth in the Eurozone countries. Journal of Policy Modeling, 42(5), 1106-1122. https://doi.org/10.1016/j.jpolmod.2020.01.004

Radojevich-Kelley, N., & Hoffman, D. L. (2012). Analysis of accelerator companies: An exploratory case study of their programs, processes, and early results. Small Business Institute Journal, 8(2), 54-70. https://sbij.scholasticahq.com/article/26258

Romanelli, E. (1989). Environments and strategies of organization start-up: Effects on early survival. Administrative Science Quarterly, 34(3), 369-387. https://doi.org/10.2307/2393149

Rossi, C., Cricelli, Grimaldi, M., & Greco, M. (2016). The strategic assessment of intellectual capital assets: An application within Terradue Srl. Journal of Business Research, 69(5), 1598-1603. https://doi.org/10.1016/j.jbusres.2015.10.024

Salamzadeh, A., & Kesim, H. K. (2015). Startup companies: Life cycle and challenges. 4th International conference on employment, education, and entrepreneurship. Belgrade, Serbia: EEE.

Salamzadeh, A., & Markovic, M. (2018). Shortening the learning curve of media start-ups in accelerators: Case of a developing country. In A. Gyamfi, & I. Williams, Evaluating media richness in organizational learning (pp. 36-48). IGI Global.

Salamzadeh, A., Tajpour, M., Hosseini, E., & Brahmi, M. (2023). Human capital and the performance of Iranian Digital Startups: The moderating role of knowledge sharing behavior. International Journal of Public Sector Performance Management, 12(1-2), 171-186. https://doi.org/10.1504/IJPSPM.2023.132248

Santisteban, J., & Mauricio, D. (2017). Systematic literature review of critical success factors of information technology startups. Academy of Entrepreneurship Journal, 23(2), 1-23. https://www.abacademies.org/articles/systematic-literature-review-of-critical-success-factors-of-information-technology-startups-6638.html

Sardo, F., & Serrasqueiro, Z. (2019). On the relationship between intellectual capital and service SME survival and growth: A dynamic panel data analysis. International Journal of Learning and Intellectual Capital, 16(3), 213-238. https://doi.org/10.1504/IJLIC.2019.100537

Smilor, R. (1997). Entrepreneurship: Reflections on a subversive activity. Journal of Business Venturing, 12(5), 341-346. https://doi.org/10.1016/S0883-9026(97)00008-6

Song, Y., & Vinig, T. (2012). Entrepreneur online social networks-structure, diversity, and impact on start-up survival. International Journal of Organisational Design and Engineering, 2(2), 189-203. https://doi.org/10.1504/IJODE.2012.047574

Spender, J. (1996). Making knowledge the basis of a dynamic theory of the firm. Strategic Management Journal, 17(S2), 45-62. https://doi.org/10.1002/smj.4250171106

Stewart, T. (1997). Intellectual Capital. Bantam Doubleday Dell Publishing Group.

Strotmann, H. (2007). Entrepreneurial survival. Small Business Economics, 28, 87-104. https://doi.org/10.1007/s11187-005-8859-z

Unger, J., Rauch, A., Frese, M., & Rosenbusch, N. (2011). Human capital and entrepreneurial success: A meta-analytical review. Journal of Business Venturing, 26(3), 341-358. https://doi.org/10.1016/j.jbusvent.2009.09.004

Van Praag, C. (2003). Business survival and success of young small business owners. Small business Economics, 21, 1-17. https://doi.org/10.1023/A:1024453200297

Vanderstraeten, J., van Witteloostuijn, A., Matthyssens, P., & Andreassi, T. (2016). (2016). Being flexible through customization − The impact of incubator focus and customization strategies on incubated survival and growth. Journal of Engineering and Technology Management, 41, 45-64. https://doi.org/10.1016/j.jengtecman.2016.06.003

Venâncio, A., & Jorge, J. (2022). The role of accelerator programs on the capital structure of start-ups. Small Business Economics, 59, 1143-1167. https://doi.org/10.1007/s11187-021-00572-8

Wamba, L., Hikkerova, L., Sahut, J., & Braune, E. (2017). Indebtedness for young companies: Effects on survival. Entrepreneurship & Regional Development, 29(1-2), 174-196. https://doi.org/10.1080/08985626.2016.1255435

Wang, W., & Chang, C. (2005). Intellectual capital and performance in causal models: Evidence from the information technology industry in Taiwan. Journal of Intellectual Capital, 6(2), 222-236. https://doi.org/10.1108/14691930510592816

Welbourne, T., & Pardo-del-Val, M. (2009). Relational capital: Strategic advantage for small and medium-size enterprises (SMEs) through negotiation and collaboration. Group Decision and Negotiation, 18, 483-497. https://doi.org/10.1007/s10726-008-9138-6

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5(2), 171-180. https://doi.org/10.1002/smj.4250050207

Wong, W., Cheung, H., & Venuvinod, P. (2005). Assessing the growth potential of high-technology start-ups: An exploratory study from Hong Kong. Journal of Small Business & Entrepreneurship, 18(4), 453-470. https://doi.org/10.1080/08276331.2005.10593353

World Bank. (2021). World Bank Entrepreneurship Database. https://www.worldbank.org/en/programs/entrepreneurshipang

World Bank. (2023). World Development Indicators. https://info.worldbank.org

Yang, C., & Lin, C. (2009). Does intellectual capital mediate the relationship between HRM and organizational performance? The perspective of the healthcare industry in Taiwan. The International Journal of Human Resource Management, 20(9), 1965-1984. https://doi.org/10.1080/09585190903142415

Yang, T., & Aldrich, H. (2017). “The liability of newness” revisited: Theoretical restatement and empirical testing in emergent organizations. Social Science Research, 63, 36-53. https://doi.org/10.1016/j.ssresearch.2016.09.006

Notes

BAR - Brazilian Administration Review encourages data sharing but, in compliance with ethical principles, it does not demand the disclosure of any means of identifying research subjects.

Author notes

(Universidade do Vale do Rio dos Sinos, Brazil)

Ricardo Limongi https://orcid.org/0000-0003-3231-7515

(Universidade Federal de Goiás, Brazil)

(Universidade de São Paulo, FEA, Brazil)

(Universidade de São Paulo, FEA, Brazil)

and two anonimous reviewers.

(ANPAD, Maringá, Brazil)

Corresponding author: Carlos Canfield Universidad Anahuac Mexico Av. Universidad Anáhuac, n. 46, Col. Lomas Anáhuac, Huixquilucan, Estado de México, Mexico

Conflict of interest declaration