Research Article

Decoding the Financial Zeitgeist: A Scientific Exploration of the Calculus of Capital for Cost-Efficient and Sustainable Growth in Investments and Operations

Enkeleda Lulaj enkeleda.lulaj@unhz.eu

Enkeleda Lulaj enkeleda.lulaj@unhz.eu

Decoding the Financial Zeitgeist: A Scientific Exploration of the Calculus of Capital for Cost-Efficient and Sustainable Growth in Investments and Operations

BAR - Brazilian Administration Review, vol. 22, no. 2, e230171, 2025

ANPAD - Associação Nacional de Pós-Graduação e Pesquisa em Administração

Received: 07 December 2023

Accepted: 13 November 2024

Published: 24 April 2025

ABSTRACT

Objective: to examine financial dynamics within the financial zeitgeist, focusing on capital calculation and cost-effectiveness for sustainable investment and operational growth.

Methods: data from 200 stakeholders in Kosovar companies (2022-2023) Were analyzed using SPSS and AMOS, with exploratory and confirmatory factor analysis, reliability analysis, and structural equation modeling (SEM) to assess direct and indirect effects among cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD).

Results: CaOE had a positive effect on both IDaII and OCaD, with IDaII also positively impacting OCaD. CaOE’s indirect effect on OCaD via IDaII was significant. Key factors included maintenance costs for CaOE, competitive advantage for IDaII, and technological advancement for OCaD.

Conclusions: the model showed excellent fit, confirming the proposed relationships. Firms should integrate investment strategies, operational efficiencies, and development capabilities for sustainable growth.

Keywords: Financial zeitgeist+ investments+ sustainable growth+ finance+ capital.

INTRODUCTION

The concept of the financial zeitgeist encompasses the prevailing trends, collective consciousness, and underlying dynamics in the financial sector that shape decision-making and behavior within a given timeframe. A rigorous understanding and decoding of this zeitgeist can optimize capital efficiency, cost management, and drive sustainable growth in investments and operations. Existing studies suggest that the financial zeitgeist is influential in framing economic behavior, especially in areas where motivations and contradictions align with broader social and economic trends. Therefore, Bouaiss et al. (2015) argue that the zeitgeist encapsulates the salience of contemporary financial trends that directly impact economic decision-making, particularly in emerging areas such as crowdfunding where motivations reflect broader socioeconomic currents. Murthy and Murthy (2014) expand on this, describing financial zeitgeist as the integration of cognition, awareness, and collective spirit across firms. Additionally, Méric (2016)and Paulo (2011) suggest that alignment with the zeitgeist is essential to achieving cost-effectiveness and operational efficiency within financial management. These studies collectively highlight the relevance of the financial zeitgeist in guiding financial strategies and decision-making processes across industries, policymaking bodies, and institutions.

Despite these insights, the current literature on financial zeitgeist has notable limitations. Existing studies tend to address cost efficiency, investment dynamics, or operational capacity as isolated factors, lacking an integrated framework that captures their interdependent roles within a holistic financial zeitgeist. Apter and Desselles (2018) underscore the role of motivational intelligence in achieving sustainable growth as a primary goal of capital investment; their analysis lacks a connection to other essential constructs, such as operational capacity and investment dynamics. Similarly, Topić et al. (2021) explore how consumer pressures are reshaping corporate social responsibility, but they do not connect these shifts to broader trends in financial consciousness or the evolving zeitgeist influencing corporate strategy. Without a cohesive approach, the field lacks an integrated perspective on the financial zeitgeist, which could enable a more comprehensive understanding of interconnected financial dynamics. Filling this gap in the literature is critical because a fragmented understanding of the financial zeitgeist limits the accuracy of financial forecasting and reduces the effectiveness of strategic responses to emerging financial trends. Without a holistic model, organizations, policymakers, and institutions are challenged to develop responsive strategies that address the interrelated dynamics of cost efficiency, investment behavior, and operational capacity. This limitation hinders the development of robust policies and strategies that can align with the evolving collective financial mindset.

As a result, an integrated framework for understanding the financial zeitgeist is essential to improve strategic planning and performance at multiple levels. This study proposes a systematic examination of the financial zeitgeist through three core constructs: cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). Together, these constructs serve as foundational elements that deepen understanding of the financial zeitgeist and support improved financial strategies and decision-making. This research approach goes beyond traditional analyses that focus on individual financial factors by developing a cohesive framework that reflects the collective financial mindset. By integrating these constructs, the study addresses the limitations in the literature and establishes a new approach for decoding the financial zeitgeist.

Moreover, this research provides several significant contributions to the field of financial management. First, it introduces a precise definition of the financial zeitgeist within a contemporary theoretical framework, offering a foundation for further exploration and application of this concept in financial analysis and strategic planning. Second, it develops a novel analytical framework that integrates CaOE, IDaII, and OCaD, which collectively capture the financial zeitgeist as a dynamic and influential factor in business decision-making. This framework is consistent with the empirical findings of Veenendaal and Kearney (2014), which highlight the impact of board dynamics and human capital on firm performance, reinforcing the need for strategic responsiveness to collective financial trends. Finally, the model provides policymakers and practitioners with valuable insights into the importance of the financial zeitgeist and supports adaptive responses to shifts in financial consciousness, as suggested by recent studies on capital structure by Putri and Willim (2023) and innovation strategies in growth firms by Spitsin et al. (2022).

In summary, through its theoretical foundation, literature review, and methodological approach, this study’s analysis establishes a new perspective on capital efficiency, industry impact, and operational development within a cohesive zeitgeist model. The sections that follow further analyze the empirical findings and theoretical implications, positioning the decoding of the financial zeitgeist as a path toward improved financial strategy and performance.

THEORETICAL FOUNDATION

This section provides the theoretical foundation for understanding how cost and operational efficiency (CaOE), investment dynamics and operational impact (IDaII), and operational capacity and development (OCaD) interact within the comprehensive framework of decoding the financial zeitgeist. This concept summarizes the emerging financial and economic trends that firms must interpret and adapt to in order to remain competitive, innovative, and sustainable. Drawing on key financial theories, this framework provides insight into how companies can align their resources, investment strategies, and operational capabilities to succeed in the current financial environment. According to Hailiang (2018), a new zeitgeist perspective is emphasized, which focuses on strategic support, fundamental approaches, and necessary investment and operational routes. Therefore, by decoding the financial zeitgeist, companies interpret and respond to the changing economic and financial dynamics driven by technological innovation, regulatory changes, sustainability imperatives, and global competition. As the economic environment becomes more complex, companies must optimize internal resources, align investments with strategic priorities, and increase operational capacity to achieve short-term financial performance and long-term sustainability. Several theoretical frameworks provide valuable insights into how firms can address these challenges. Resource-based theory, developed by Barney (1991) and Wernerfelt (1984) and extended by Utami and Alamanos (2023), emphasizes the importance of leveraging internal resources for competitive advantage. Barney (2001) further elaborated resource-based theories of competitive advantage, while his strategic management theory (Barney, 2020) provides a framework for evaluating firm performance. In addition, Denrell and Powell’s (2016) theory of dynamic capabilities emphasizes the need for firms to adapt and renew competencies in changing environments. Finally, Meredith’s (1998) work on construction operations management theory provides insights into strengthening operational processes to support the firm’s overall strategy.

Cost and operational efficiency (CaOE) is essential to drive financial sustainability while supporting innovation goals. Resource-based theory emphasizes how firms can gain competitive advantage by optimizing internal resources, particularly through the adoption of advanced technologies such as Industry 4.0 and circular economy practices. Alkaraan et al. (2023) show that this synergy between technology and environmental sustainability leads to improved financial performance. Transaction cost theory (Knoedler, 1995) and transaction cost economics (Williamson, 2010) further emphasize the importance of minimizing inefficiencies in resource allocation, including waste management, as noted by Depczyński (2022). By focusing on operational efficiency, companies can streamline processes, reduce costs, and contribute to long-term sustainability. Furthermore, agency theory (Eisenhardt, 1989) emphasizes the need for financial accountability mechanisms to prevent overproduction and improve cost management, as discussed by Galdi and Johnson (2021). Together, these theories show how CaOE plays a central role in shaping financial performance by aligning operational strategies with sustainability and efficiency goals.

Investment dynamics and operational impact (IDaII) is grounded in the principles of dynamic capabilities theory, which explains how firms renew and adapt their capabilities by investing in innovation and technology to respond to changing financial conditions. Choi and Kim (2008) argue that continuous investment in research and development increases a firm’s ability to respond to market changes, driving operational efficiency and industrial impact. The pecking order theory of corporate capital structure, as explained by Frank et al. (2020), states that firms prioritize their financing sources based on adverse selection concerns. Managers, who possess private information, may have incentives to issue risky overpriced securities, but they understand that rational investors, disadvantaged by incomplete information, will discount the prices of these securities. As a result, firms usually follow a quick order: they first use internal resources, then seek external debt if necessary, and only turn to external capital as a last resort. Fiscal policy theory, discussed by Canale (2019), traces its evolution from Keynesian principles, where public spending was used to support aggregate demand and full employment, to a modern framework where fiscal policy is seen as an external shock, especially in the Eurozone. After the global financial crisis, fiscal policy has been recognized for its short- and long-term effects on both income and potential output, although it has yet to regain a central role in economic strategy, especially in Europe. These theories emphasize the importance of strategic financial planning in shaping investment outcomes. Hanafi et al. (2019) demonstrate that the alignment of investment decisions with fiscal policies and market conditions significantly affects operational performance. Additionally, system dynamics modeling, as explored by Oesterreich and Teuteberg (2020), illustrates how financial constraints and risk assessments affect long-term operational outcomes, enabling firms to better navigate uncertainty. In conclusion, these theories show that IDaII is central to understanding how firms manage investment strategies to optimize operational performance and ensure long-term sustainability.

Operational capacity and development (OCaD) is a critical element in maintaining organizational efficiency and sustainability, especially in times of economic and financial uncertainty. Gupta and Boyd (2008) point out that the theory of constraints (TOC) serves as a strong framework for operations management, providing decision-making strategies that prevent local optimization by promoting a cross-functional approach within organizations. Peng and Bai (2022) argue that firms with more focused operational strategies tend to outperform their competitors, highlighting the direct link between operational capability and financial performance. The technology adoption model (TAM) developed by Davis (1989) is also crucial for OCaD. Xi et al. (2024) show that the adoption of intelligent manufacturing technologies significantly improves a firm’s operational sustainability, especially during crises such as the COVID-19 pandemic. TAM, based on the theory of reasoned action, asserts that perceived ease of use, perceived usefulness, and attitudes toward the technology are critical factors influencing its acceptance and adoption. Contingency theory (Otley, 1980) further states that firms must adapt operational strategies in response to external conditions, suggesting an improved model that focuses on organizational control and effectiveness. Thus, these theoretical perspectives emphasize the importance of aligning operational capabilities with changing market demands and competitive pressures (Cagno et al., 2022). These frameworks show that OCaD is essential to enable firms to respond effectively to external changes, thereby promoting sustainable growth and long-term success.

In synthesizing these perspectives, CaOE, IDaII, and OCaD are not isolated factors, but interconnected components of a broader framework for decoding the financial zeitgeist. CaOE ensures efficient use of resources and supports innovation, while IDaII facilitates adaptive investment strategies that enable firms to manage financial constraints and uncertainties. OCaD strengthens a firm’s capacity to meet evolving operational requirements and adapt to external challenges. Therefore, these factors form a cohesive theoretical foundation that guides firms in navigating the complexities of today’s financial environment, ensuring their long-term sustainability and operational success.

In summary, this theoretical framework, informed by resource-based theory, dynamic capabilities, operations management, and other major financial theories, provides a strong foundation for understanding how firms decode the financial zeitgeist to maintain competitiveness and pursue sustainable development.

LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

The role of cost and operational efficiency (CaOE) in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

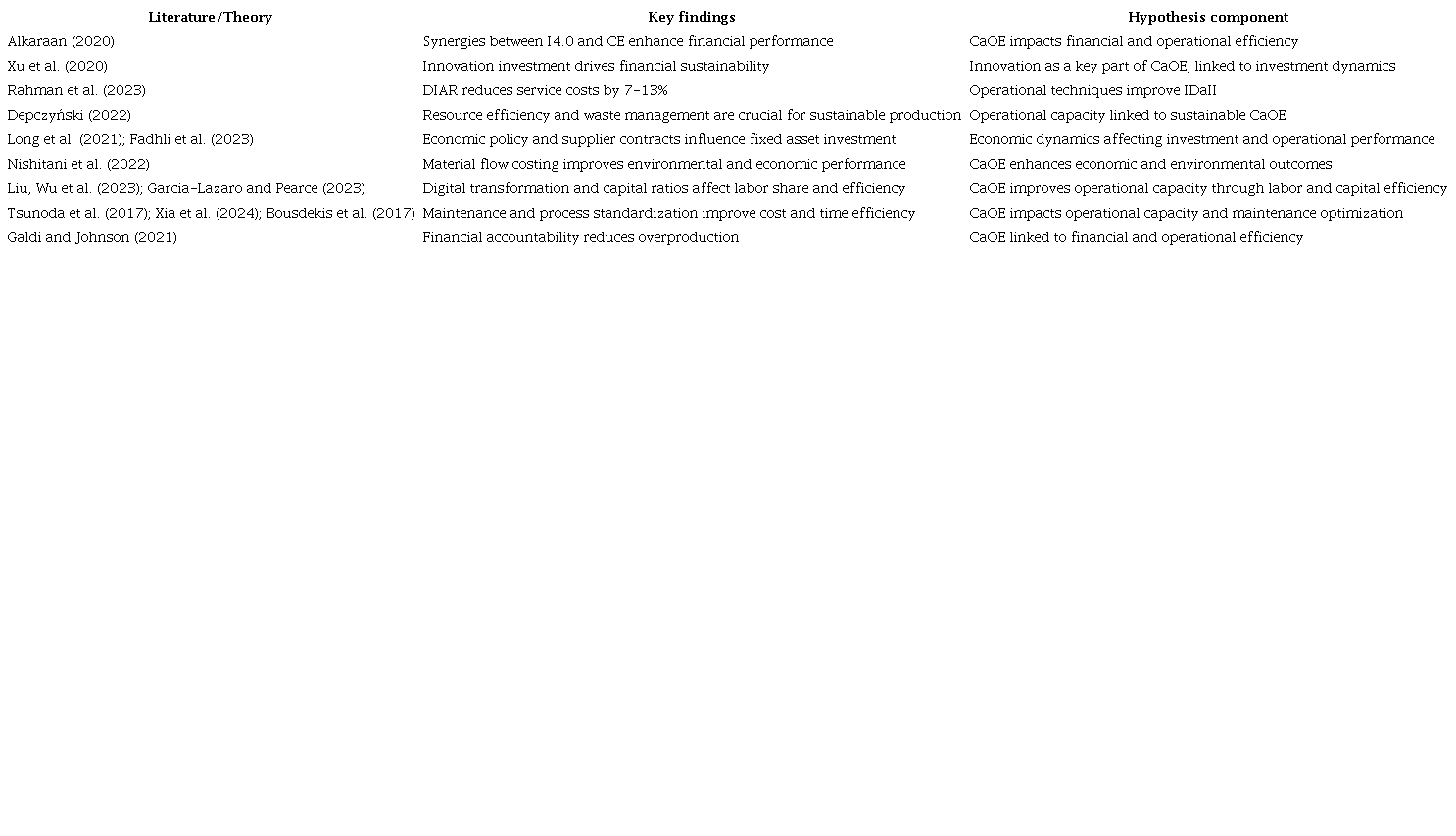

The central theory driving this research is the decoding of the financial zeitgeist. This theory posits that understanding the broader economic context - referred to as the zeitgeist - can help align financial and operational strategies in a way that optimizes both sustainability and growth. The central construct of this study is cost and operational efficiency (CaOE), which refers to how well a company manages its costs and operations to improve its overall financial performance and sustainability. Research highlights the significant role of CaOE in improving financial performance and operational sustainability. For instance, investment in innovation - particularly innovation spending - has been shown to be essential to achieving long-term financial goals, as demonstrated by Xu et al. (2020). Similarly, the use of dial-a-ride (DIAR) systems, which can reduce service costs by 7% to 13%, illustrates how operational strategies directly affect financial sustainability, as noted by Rahman et al. (2023). In addition to these operational improvements, resource efficiency and waste management have emerged as pivotal factors for sustainable development across industries. Research by Long et al. (2021) reveals how economic policy uncertainty, capital costs, and raw material prices create asymmetric effects on investment in fixed assets, highlighting the complexities of achieving cost efficiency. Supplier contracts, particularly those specifying raw material procurement agreements, are also crucial for resource forecasting and cost management, as emphasized by Fadhli et al. (2023). Material flow costing has proven to be a valuable tool for improving both environmental and economic performance, with Nishitani et al. (2022)underscoring its effectiveness in boosting organizational efficiency. Similarly, Li et al. (2023) demonstrate that regulatory factors, such as China’s 2008 Labor Contract Law, significantly influence foreign direct investment (FDI) decisions, which, in turn, affect labor costs and operational capacity. Furthermore, Liu, Wu et al. (2023) highlight digital transformation as another critical factor in enhancing labor efficiency, reinforcing the role of CaOE in improving operational outcomes. In line with this, Tsunoda et al. (2017) emphasize that process standardization, such as reducing the working hours of information system operators, can significantly improve operational efficiency. Xia et al. (2024) present innovative strategies, such as M-OMICJO, that optimize maintenance outsourcing and inventory management, further demonstrating how operational techniques contribute to improved efficiency.

(a) Summary of the theoretical links to Hypothesis 1: The literature reviewed illustrates the multifaceted role of CaOE, encompassing innovation investments, operational strategies, regulatory factors, and digital transformation. Collectively, these findings underscore the importance of CaOE in improving both financial and operational performance. By synthesizing insights from these diverse areas, the research supports the proposition that CaOE is a key driver of both investment momentum and operational impact.

(b) Hypothesis derivation: Rationale for Hypothesis 1: Based on the theoretical foundation established in the literature, it is evident that CaOE is a critical determinant of both investment dynamics and operational impact. Improvements in cost management, resource efficiency, innovation, and labor investment directly contribute to better financial and operational outcomes. Thus, Hypothesis 1 logically posits that CaOE positively affects investment dynamics and operational capacity.

H1: CaOE (cost and operational efficiency) has a direct and positive effect on:

H1a: IDaII (investment dynamics and operational impact) by decoding the financial zeitgeist.

H1b: OCaD (operational capacity and development) by decoding the financial zeitgeist.

(c) How Hypothesis 1 extends or challenges existing knowledge: Hypothesis 1 extends existing knowledge by integrating findings from diverse fields - such as innovation, cost management, and digital transformation - into a unified framework that positions CaOE as a central driver of both financial and operational success. While previous research often examines these elements separately (e.g., DIAR’s effect on cost reduction or material flow costing’s impact on environmental performance), this hypothesis challenges traditional views by framing CaOE as a holistic factor influencing broader investment and operational outcomes. It advances the discussion by positioning CaOE not as a secondary consideration, but as a core factor essential for navigating today’s financial challenges and achieving sustainable development.

The role of investment dynamics and operational impact (IDaII) in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

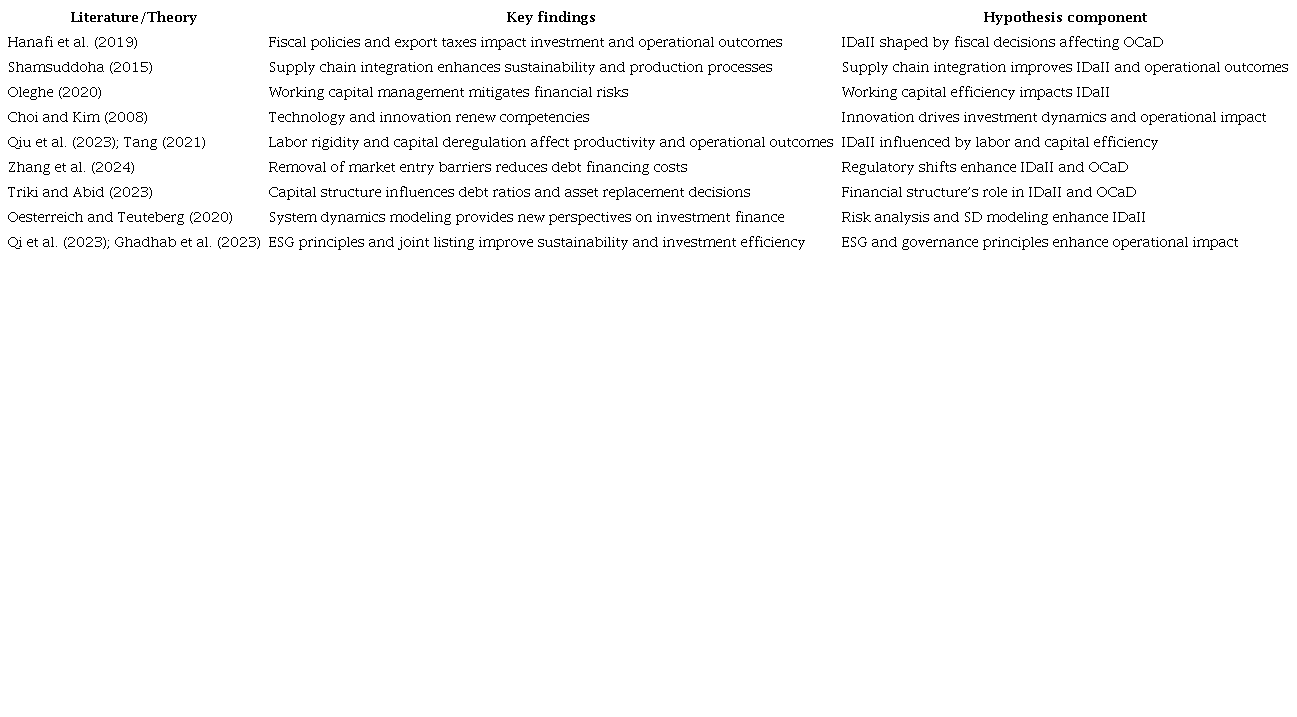

Investment dynamics and operational impact (IDaII) is crucial for understanding the sustainable development of both investments and operations. Shamsuddoha (2015) emphasizes that supply chain integration is essential for economic, social, and environmental sustainability as it helps optimize investment dynamics, especially in vertically integrated companies. Oleghe (2020) highlights the importance of working capital management in mitigating financial risks and improving operational effectiveness. Research by Qiu et al. (2023)identifies labor input rigidity as a significant factor in operational impact, particularly in firms with high labor intensity. In addition, Tang (2021) shows how capital misallocation can hinder the productivity of manufacturing firms and suggests that eliminating misallocation could improve operational outcomes. Zhang et al. (2024) show that the removal of entry barriers has a direct effect on reducing the cost of debt financing, which further influences investment and operational outcomes. The literature also discusses the critical role of financial structuring in shaping investment dynamics. Triki and Abid (2023) find that a firm’s capital structure, particularly its leverage ratio, has a significant impact on operational decisions, reinforcing the importance of strategic financial planning. In addition, Karanina et al. (2023)find that direct investment through parent-subsidiary integration contributes to international business development and operational efficiency. Finally, Qi et al. (2023)argue that ESG principles significantly shape investment dynamics by promoting sustainable infrastructure, while Ghadhab et al. (2023) show that common listing can mitigate investment inefficiencies, thereby enhancing operational impact.

(a) Summary of the theoretical links to Hypothesis 2: The reviewed literature reveals a clear link between fiscal policies, technological integration, supply chain management, and investment dynamics, all of which have a direct impact on operational capacity and development (OCaD). The integration of ESG principles and strategic financial decisions further supports the hypothesis that IDaII positively affects OCaD by decoding the financial zeitgeist.

(b) Hypothesis derivation: Rationale for Hypothesis 2: The literature demonstrates that investment dynamics - shaped by fiscal policies, technological innovation, and financial structuring - directly impact operational outcomes. The integration of supply chains, management of working capital, and strategic financial planning enhance operational impact. Therefore, it logically follows that IDaII has a direct and positive effect on OCaD, mediated by the financial decoding of the zeitgeist.

H2: IDaII has a direct and positive effect on OCaD by decoding the financial zeitgeist.

(c) How Hypothesis 2 extends or challenges existing knowledge: Hypothesis 2 challenges traditional views by proposing a comprehensive framework in which multiple dimensions of investment dynamics - such as technological innovation, supply chain integration, and financial structuring - collectively drive operational development. It also broadens the discourse by suggesting that decoding the financial zeitgeist is central to understanding how these dynamics translate into sustainable operational outcomes.

The role of operational capacity and development (OCaD) in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

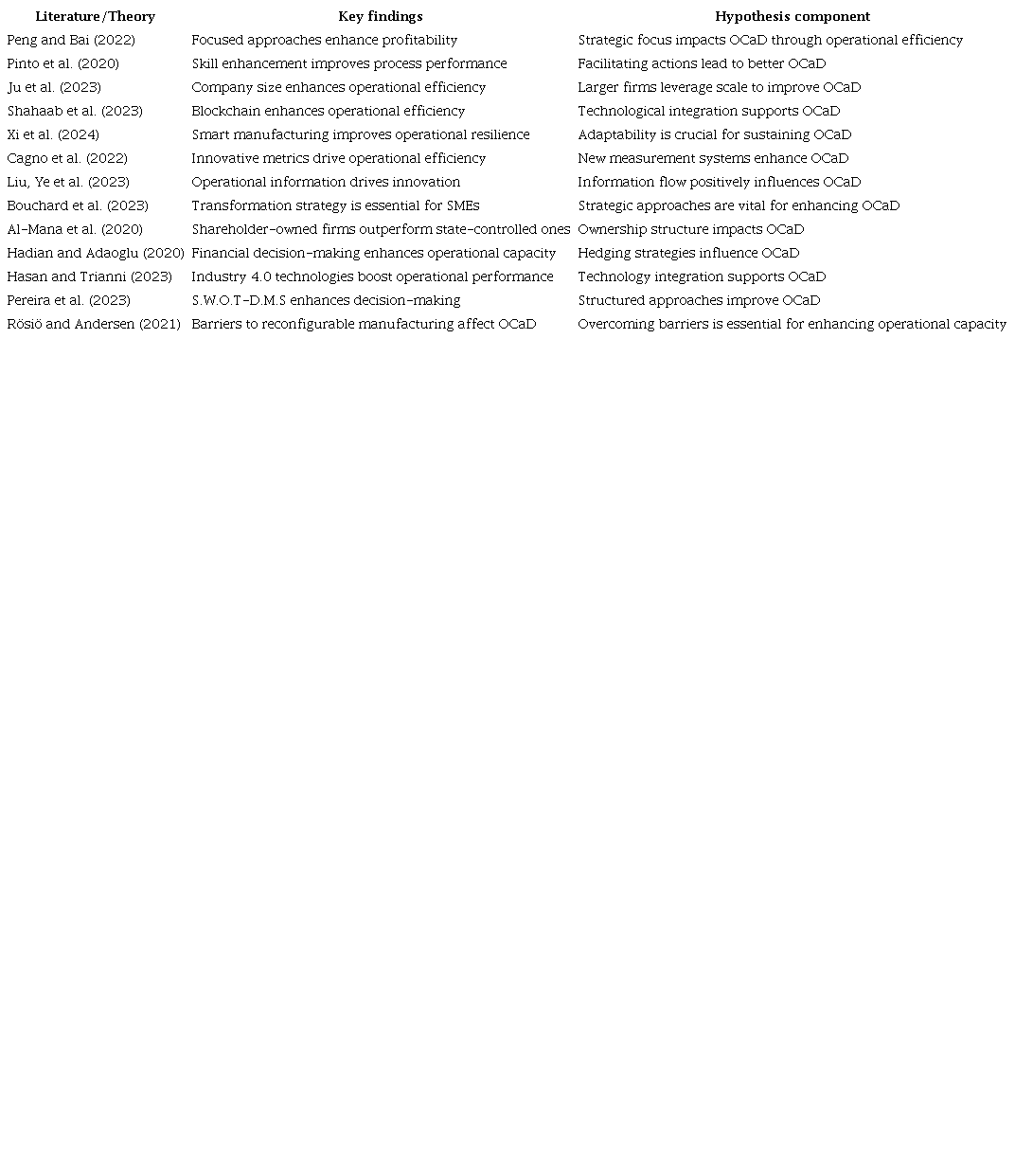

Operational capacity and development (OCaD) is a critical component of sustainable business practices. Pinto et al. (2020) highlight that job characterization and standardized procedures improve worker skills, which, in turn, improve process performance and equipment efficiency. Ju et al. (2023) argue that competitive pressures positively influence operational efficiency, with larger firms leveraging their scale to improve OCaD. Blockchain technology is another key driver of OCaD, as shown by Shahaab et al. (2023), who demonstrate its transformative potential in improving operational efficiency in public service organizations. Liu, Ye et al. (2023) emphasize the importance of operational information in driving innovation, especially in non-public firms facing financial constraints. In addition, Bouchard et al. (2023) argue that strategic transformation for SMEs - through modular product and process designs, technology exploitation, and collaborative networks - is essential for improving OCaD. In addition, Al-Mana et al. (2020) show that shareholder-owned firms tend to outperform their state-controlled counterparts, reinforcing the relationship between ownership structure and OCaD. Technological advances, particularly Industry 4.0, also have a significant impact on operational capabilities, as discussed by Hasan and Trianni (2023).

(a) Summary of theoretical links to Hypothesis 3: The literature illustrates the interdependence of strategic decision-making, technological integration, and market dynamics in influencing OCaD. The integration of innovative measurement systems, operational information, and strategic transformation collectively promotes OCaD. These insights support the hypothesis that the relationship between CaOE and OCaD is mediated by IDaII.

(b) Hypothesis derivation: Rationale for Hypothesis 3: The complex nature of OCaD is influenced by a variety of factors, including strategic decisions, technological advancements, and organizational dynamics. The connection between operational skills, efficiency, and technological integration underscores the multifaceted nature of OCaD. Hence, it follows that investment dynamics and industrial impact (IDaII) mediate the indirect relationship between CaOE and OCaD.

H3: IDaII mediates the relationship between CaOE and OCaD by decoding the financial zeitgeist.

(c) How Hypothesis 3 extends or challenges existing knowledge: Hypothesis 3 extends existing knowledge by proposing that IDaII serves as a mediator between CaOE and OCaD, providing a more nuanced view of how cost efficiencies and operational improvements translate into capacity development. This mediating role challenges the assumption that OCaD is driven solely by direct organizational or technological change, and instead recognizes the importance of investment dynamics in shaping operational outcomes.

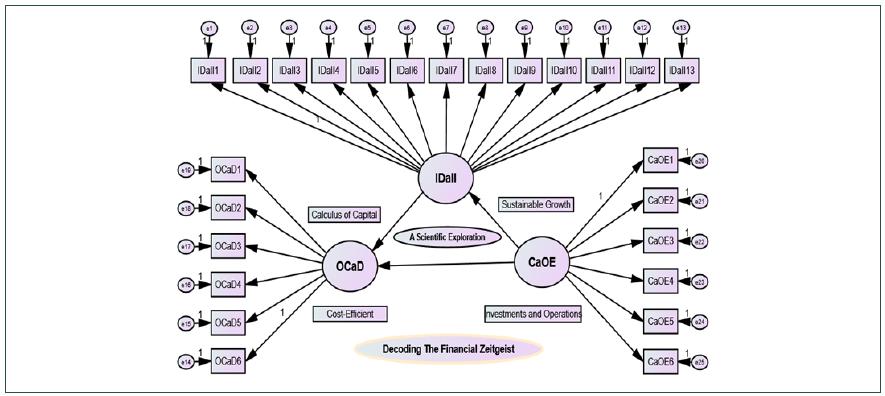

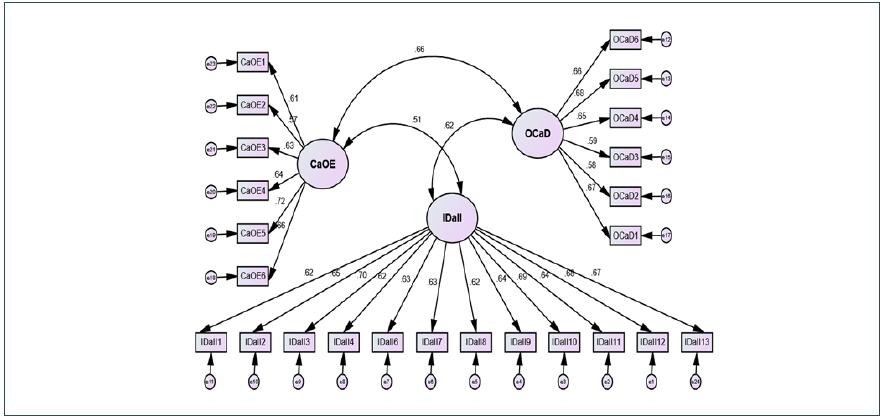

The conceptual model depicted in Figure 1 illustrates the framework for decoding the financial zeitgeist, focusing on three key constructs: cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). Each construct includes relevant variables (CaOE1-6, IDaII1-4, 6-13, and OCaD1-6) that capture specific dimensions of the constructs. The central concept, financial decoding of the zeitgeist, represents the analytical lens through which the relationships among these constructs are interpreted. The model depicts the following hypothesized relationships:

Figure 1

Conceptual model of decoding the financial zeitgeist (CaOE, IDaII, and OCaD).

Source: Author’s analysis (2023-2024).

H1: CaOE has a direct and positive effect on both IDaII and OCaD by the financial decoding of the zeitgeist. This is represented by arrows from CaOE to IDaII and CaOE to OCaD, indicating that CaOE contributes to improved investment dynamics and operational capacity.

H2: IDaII has a direct and positive effect on OCaD by decoding the financial zeitgeist. This relationship is represented by an arrow from IDaII to OCaD, illustrating that investment dynamics directly enhance operational capacity and development.

H3: IDaII acts as a mediator in the relationship between CaOE and OCaD, providing an indirect pathway through which CaOE influences OCaD via IDaII. This mediation effect is represented by a pathway from CaOE to OCaD through IDaII, underscoring the importance of investment dynamics as a bridge between cost efficiency and operational development.

Together, these hypotheses illustrate the interconnected roles of cost efficiency, investment dynamics, and operational development in interpreting the financial zeitgeist. This model advances theoretical understanding and offers practical insights into fostering sustainable growth and efficiency in investments and operations.

METHODOLOGY

The purpose of the paper

This study examines capital calculus from a scientific perspective, aiming to decode the financial zeitgeist to promote cost-efficient and sustainable growth in investments and operations. It explores the relationships - both direct and indirect - among three key constructs: cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). By analyzing these relationships within the current financial context, the research provides new insights into capital efficiency for industries, institutions, policymakers, and nations.

Sample size reporting and appropriateness

To ensure methodological rigor, the sample sizes used for each analysis are clearly reported. For exploratory factor analysis (EFA), confirmatory factor analysis (CFA), and structural equation modeling (SEM), the total sample size was (N = 200). This sample size was determined according to Kline’s (2015) guidelines, which recommend a minimum of 200 cases for SEM.

Power analysis (G*Power) was performed to confirm that this sample size was sufficient to detect the expected effect sizes, especially for SEM. Sensitivity analysis was also used to ensure robustness in terms of model stability and interoperability. It is important to note that there are no missing data from the 200 company respondents, ensuring that the sample size is not limited. To validate the representativeness and reliability of the sample, analyses were conducted on sample characteristics, representativeness, critical F statistics, descriptive statistics (including skewness and kurtosis), and Cohen’s effect size.

Data collection and measurement tools

Data were collected through an online survey using a five-point Likert scale (1 = strongly disagree to 5 = strongly agree) and in-person interviews conducted in Kosovo between 2022 and 2023. A five-point scale was chosen because of its proven ability to capture attitudes while balancing respondent convenience (Dawes, 2008). Although other scales, such as seven- or ten-point options, were considered, the five-point scale was preferred to reduce respondent fatigue and streamline data interpretation. After being highlighted in the pilot survey, one of the recommendations was answered with five degrees. Potential response biases, including central tendency and acquiescence bias, were minimized by providing respondents with clear instructions on how to complete the survey.

For in-person interviews, interviewers were trained to follow standardized protocols. Each interview followed a structured guide, and responses were recorded and systematically analyzed to reduce interviewer effects and increase the reliability of findings.

Data analysis

Data analysis was performed in several steps to ensure a thorough exploration of the relationships between CaOE, IDaII, and OCaD. Analyses were performed using SPSS (64-bit) and AMOS (26.0) software:

(a) Exploratory factor analysis (EFA): Following Spearman’s (1927) methodology, EFA was conducted to identify underlying factor structures and provide initial insight into the constructs. The statistical thresholds used in this study - including factor loadings (λ > 0.50), significance (p < 0.001), and reliability (Cronbach’s alpha, α ≥ 0.70) - were chosen based on widely accepted standards in finance and management research to ensure the robustness of the analysis. A factor loading threshold of 0.50 was applied to confirm that each item contributed substantially to its respective construct, as recommended for construct validity (Hair et al., 2014). The conservative significance level of p < 0.001 was chosen to reduce the likelihood of Type I errors, consistent with financial research practices that prioritize minimizing false positives in complex, multifactorial datasets (Benjamini & Hochberg, 1995). Reliability was assessed using Cronbach’s alpha, with α ≥ 0.70 serving as the benchmark for internal consistency (Cronbach, 1951; Nunnally & Bernstein, 1994); the observed values (e.g., α = 0.803 for cost and operational efficiency, α = 0.903 for investment dynamics and industrial impact) indicate strong consistency across constructs. These thresholds, which are consistent with current best practices in financial research, strengthen the basis for interpreting the study results. The results section presents factor loadings, Kaiser-Meyer-Olkin (KMO) values, Bartlett’s test results, and Cronbach’s alpha values for each construct to demonstrate the reliability and appropriateness of the analysis.

(b) Confirmatory factor analysis (CFA): Based on Jöreskog’s (1969) approach, CFA validated the hypothesized factor structures. Standardized regression coefficients (β) and correlation coefficients (r) assessed the relationships among the latent variables.

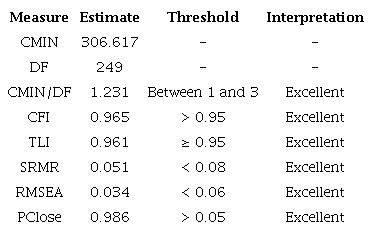

(c) Structural equation modeling (SEM): SEM was conducted following Hooper et al. (2008) and Bentler (1990) using fit indices such as RMSEA, SRMR, CFI, and TLI. Model fit criteria were set with a CFI value ≥ 0.95 (West et al., 2012) and RMSEA ≤ 0.05 (MacCallum et al., 1996) as optimal indicators of model stability. Chi-square (χ²) divided by degrees of freedom between 1 and 3 was considered an excellent fit according to Kline (1998). Table 14 provides a summary of the model fit indices and statistical methods, thus increasing transparency and replicability.

Model specification and modification in SEM

The initial specification of the SEM model was based on theoretical frameworks and prior research, which provided an informed design. The data from the SEM model had high values, so no modification was required. In the SEM analysis subsection, the results of this analysis are elaborated in detail (e.g., paths and correlated error terms), thus increasing the validity of the model. So, a CFI value of ≥ 0.95 is considered an excellent fit for the model by West et al. (2012) and McDonald and Marsh (1990).

Then, (N - 1) FML where FML is the value of the statistical criterion (fit function) minimized in ML estimation, and (N - 1). Minimum discrepancy function by degrees of freedom divided by Steiger and Lind (1980):

In this equation, k is the number of groups, χi2 and χ2 are chi-square values for different models, and mi, mi′ are the respective degrees of freedom. Understanding how chi-square values relate to degrees of freedom is essential for evaluating model fit, as emphasized by Eisenhauer (2008). A value of χ2/df≤2 is considered acceptable according to Tabachnick and Fidell (2007), and a p-value less than 0.05 indicates statistical significance (Jöreskog & Sorbom, 1996). Then, chi-square divided by degrees of freedom by Kline (1998), Marsh and Hocevar (1985) is an excellent fit between values 1 and 3. Furthermore, the root mean square error of approximation with values ≤ 0.05 are considered excellent (MacCallum et al., 1996; Steiger, 1990).

These analyses contribute significantly to the understanding of the financial zeitgeist and support the study’s objective of achieving cost efficiency and promoting sustainable business practices.

Replication details in the methodology

To promote replicability, the methodology section provides specific details on the sample, participant demographics, sampling procedures, and data analysis strategies. A breakdown of participant characteristics (e.g., industry sectors, company sizes, respondent roles, etc.) is provided in Tables 5, 6, and 7. The qualitative analysis of the data used for coding was based on the theories highlighted in Theoretical Foundation section. Table 4 outlines the theoretical contributions associated with each actor and its variables, highlighting the foundations used in their construction.

Rationale for mixed methods approach

This study uses a mixed methods approach, integrating quantitative Likert scale data with qualitative interview responses to comprehensively address the research questions. This design enhances the analysis by utilizing numerical data and contextual knowledge, following a convergent parallel design to analyze both data types simultaneously. The qualitative data added depth to the quantitative findings. A detailed integration of these findings is presented in the results, highlighting findings for each analysis and test used in this research.

Sampling strategy and generalizability

The study focuses on Kosovo firms in 2022-2023 to examine investment dynamics, cost efficiency, and operational capacity in a developing market. While this targeted sampling allows for a deeper understanding of Kosovo’s business environment, limitations to generalizability are acknowledged. Kosovo’s unique economic, regulatory, and cultural characteristics may affect the applicability of findings to other regions in Europe and beyond.

Transparency and justification of statistical analysis

The statistical analysis framework used in this study adheres to rigorous criteria, employing thresholds and model fit standards from the established literature (MacCallum et al., 1996; West et al., 2012). Reporting effect sizes alongside p-values enhances the interpretability of findings, while power analysis demonstrates that the sample size was adequate to detect hypothesized effects, particularly in SEM. This approach increases confidence in the statistical reliability and transparency of the study.

Operationalization of key constructs

The CaOE, IDaII, and OCaD constructs were operationalized based on an extensive literature review and refined through expert feedback. Survey items were validated through cognitive interviews and pilot testing confirmed item reliability, ensuring that each construct meaningfully captures the dimensions relevant to deciphering the financial zeitgeist.

Table 4 shows the elaboration of the three factors and the variables included in each factor. CaOE includes six variables, IDaII includes 13 variables, and OCaD includes six variables. Finally, statistical validation procedures, including convergent validity, power analysis, and sensitivity analysis, were used to verify the validity of the three factors - CaOE, IDaII, and OCaD - concerning the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve cost efficiency and promote sustainable growth in investments and operations within the company. Together, these processes enhanced the overall reliability and validity of the survey instruments used in the study.

Note. Author’s analysis (2023-2024). Each construct is linked to its definition and indicators, providing a clear understanding of their relationships. The bullet points within the table enhance clarity and organization.

ANALYSIS AND DISCUSSION OF RESULTS

This section examines the results from multiple analyses to assess how well the financial zeitgeist is decoded through the three factors: cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). These factors are explored through scientific analysis of capital calculations to support sustainable economic growth in investments and operations in companies. The section begins by presenting descriptive statistics on respondent characteristics and representativeness, followed by an analysis of F and critical F statistics to determine the significance of demographic variables. Subsequent analyses include EFA, CFA, SEM, Cohen’s effect size, power analysis, and sensitivity analysis for each subsection.

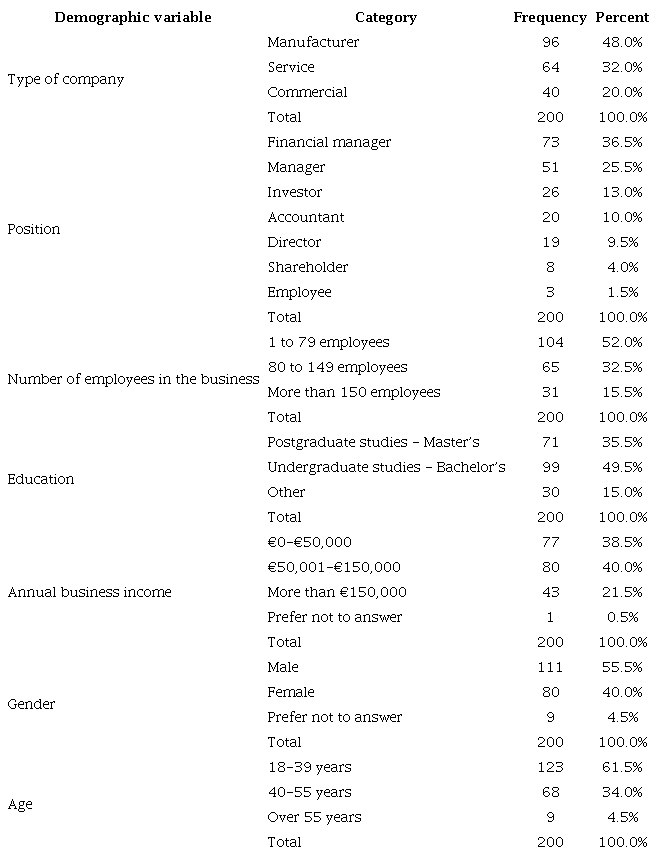

Table 5 shows the sample characteristics and representativeness, providing a comprehensive overview of the demographic characteristics of the 200 participants/companies in the study regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. The data reveal that a significant majority of respondents are employed in manufacturing (48.0%), followed by service providers (32.0%) and retailers (20.0%). This distribution indicates a notable representation from the manufacturing sector, which may influence the study’s findings and implications. In terms of professional roles, most respondents hold managerial positions, with financial managers constituting the largest group at 36.5%. Other roles include general managers, investors, accountants, directors, shareholders, and employees, reflecting insights captured from key decision-makers within organizations. Regarding company size, over half of the respondents (52.0%) work for organizations with 1 to 79 employees, while a smaller proportion is employed in larger firms (32.5% have 80 to 149 employees, and 15.5% work for companies with more than 150 employees). The educational background of respondents is noteworthy, with nearly half (49.5%) holding undergraduate degrees and 35.5% possessing postgraduate qualifications (master’s). This indicates a well-educated respondent pool, potentially enhancing the credibility of the insights gathered. When examining annual business income, the results show a near-even distribution between businesses earning €0-€50,000 (38.5%) and those earning €50,001-€150,000 (40.0%), with a smaller segment (21.5%) generating more than €150,000. This distribution provides valuable insights into the economic environment and operational scale of the respondent companies. Additionally, the gender distribution indicates that the majority of respondents identify as male (55.5%), while females comprise 40.0%, with a small percentage (4.5%) opting not to disclose their gender. The age distribution reveals that most respondents (61.5%) fall within the 18 to 39 age range, suggesting a trend toward younger professionals in the workforce, which could influence perspectives on industry practices and innovations. In summary, these insights not only provide valuable information about the demographic composition of the respondents but also highlight their professional backgrounds, company characteristics, and personal attributes.

Note. Author’s analysis (2023-2024). In the ‘education’ variable, the ‘other’ category includes 12 respondents with certifications from financial and accounting institutions, six pursuing doctoral degrees, and 12 holding international investment certifications.

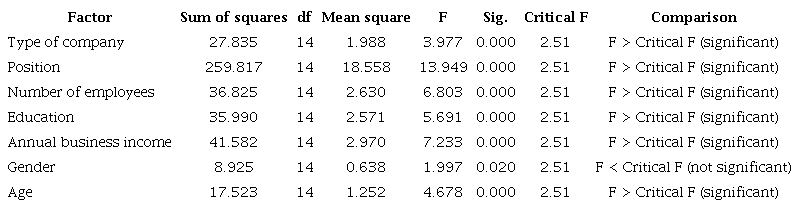

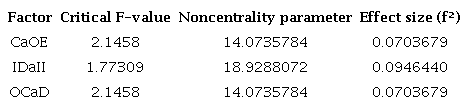

Table 6 shows the F statistics evaluated against critical thresholds, highlighting the statistical significance of various factors affecting the three core areas of this study, such as cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). The results indicate that the CaOE factor is significantly influenced by the type of company, position within the organization, number of employees, education level, and annual business income. Specifically, the company type factor yielded an F statistic of 3.977 with a p-value of 0.000, exceeding the critical F-value of 2.51, indicating a strong significant effect. This suggests that different types of companies implement different operational strategies and efficiencies, which ultimately affect their cost structures and overall operational performance. Similarly, the Position factor produced an F statistic of 13.949, reinforcing the notion that the role of management plays a critical role in shaping operational efficiency within organizations. Furthermore, the IDaII factor was also found to be significantly affected by several variables. The number of employees in the business showed an F statistic of 6.803 with a p-value of 0.000, which indicates that the scale of operations can influence investment decisions and the resultant industrial impact. Larger firms may have more capital to invest, thus affecting their market dynamics and growth potential. Similarly, the annual business income factor, with an F statistic of 7.233, suggests that higher income levels correlate with more dynamic investment strategies, enhancing industrial performance and growth prospects. On the other hand, the OCaD factor reveals significant findings as well, with education level and age showing statistically significant F statistics of 5.691 and 4.678, respectively, both with p-values less than 0.05. This indicates that higher education levels among employees contribute positively to operational capacities, as educated individuals tend to be more adept at managing complex tasks and optimizing workflows. Similarly, the age of respondents plays a role, potentially reflecting the experience and adaptability of different age groups in operational settings. In contrast, the gender factor presented an F statistic of 1.997, which, despite being statistically significant (p = 0.020), was less than the critical F-value of 2.51, suggesting that while gender does have some influence, it may not be as pronounced as other factors. Overall, the findings reinforce the importance of understanding the interplay of these variables in shaping the operational efficiency, investment dynamics, and development capabilities of organizations, emphasizing that strategic decisions must consider these factors for effective management and growth.

Note. Author’s analysis (2023-2024). Sig.: Represents the significance level (p-value) of the F statistic. Critical F: This value is determined based on the chosen significance level (α = 0.05) and degrees of freedom. For this example, a critical F value of 2.51 is used. Comparison: Indicates whether the calculated F-value is greater than or less than the critical F-value, determining the significance of the results.

Table 7 presents the descriptive statistics for three factors analyzed, such as cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD) regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. Each factor is based on a robust sample size of 200 companies. The CaOE factor has a mean of 18.64, suggesting that participants generally view cost and efficiency positively, with a standard deviation of 4.33 indicating moderate dispersion around this mean. Conversely, the IDaII factor has a higher mean of 39.77, coupled with a standard deviation of 9.24, reflecting a broader range of perspectives on investment dynamics and its industrial impact, highlighted in particular by its moderate negative skewness of -0.622. The OCaD factor, with a mean of 18.87 and a standard deviation of 4.28, indicates a balanced view among the participants, similar to the CaOE factor. However, the positive kurtosis values for all factors suggest that the distributions are relatively peaked with potential outliers present, warranting further investigation of these extreme values.

Note. Author’s analysis (2023-2024). Valid N (listwise) = 200.

Exploratory factorial analysis (EFA) and Cronbach’s alpha (reliability analysis) of (CaOE, IDaII, and OCaD) factors in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

In this section, a comprehensive analysis of the model data was conducted using statistical methods, specifically exploratory factorial analysis (EFA) and Cronbach’s alpha. These analyses were used to ensure a careful and clear examination of the significance of the three model factors (CaOE, IDaII, and OCaD) and their respective variables.

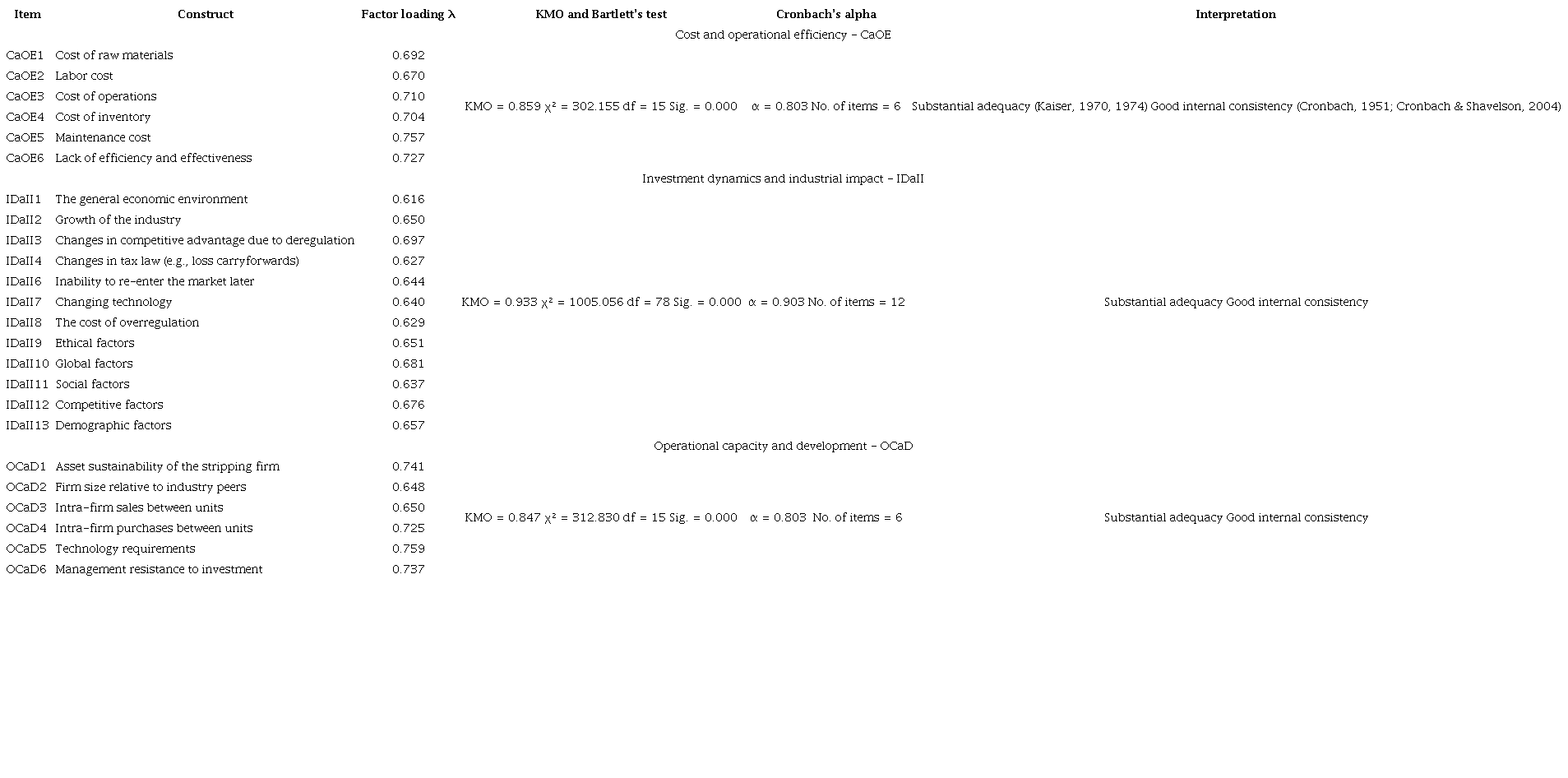

Table 8 shows the pattern matrix according to EFA, which emphasizes the creation of three factors (cost and operational efficiency - CaOE, investment dynamics and industrial impact - IDaII, and operational capacity and development - OCaD) with their subfactors (CaOE1-6, IDaII1-4, 6-13, OCaD1-6) related to the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve efficient costs and promote sustainable growth in investments and operations in companies. All subfactors of the factors are important as their value is above 0.50. According to the KMO test (Kaiser & Rice, 1974) for all three factors, it is emphasized that the data have a reliable fit to the model as its value is above 0.80 (CaOE, KMO = 0.859; IDaII, KMO = 0.933; OCaD, KMO = 0.847), and according to Bartlett’s test of sphericity, it is emphasized that the data for all three factors are important and significant (Sig. = 0.000) as there is a high correlation between the variables. Furthermore, according to the reliability analysis (Cronbach’s alpha) (Cronbach, 1951), it is emphasized that the factors (CaOE, IDaII, and OCaD) together with their variables included in the model have a high degree of reliability (CaOE, 0.80 ≥ α ≤ 0.70; IDaII, 0.90 ≥ α ≤ 0.70; OCaD, 0.80 ≥ α ≤ 0.70). Therefore, the analysis results lead to the conclusion that companies should give serious consideration to the key factors identified: cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). These factors, recognized as pivotal determinants of the financial landscape, significantly influence a company’s ability to attain cost efficiency and foster sustainable growth in both investments and operations. Notably, the variables within the model under these factors exhibit a substantial level of impact, emphasizing that a strategic focus on these aspects will markedly affect both financial and operational performance. The statistical analysis underscores the model’s robust and dependable foundation, affirming that the insights derived from these factors and variables hold validity and utility for shaping effective business strategies and decisions. This analytical framework serves as a crucial tool for management, aiding in the identification and resolution of capital and operational challenges to enhance overall performance and ensure sustained future growth.

Note. Author’s analysis (2023-2024). α: Cronbach’s alpha; KMO: Kaiser-Meyer-Olkin; χ²: Chi-square; df: Degrees of freedom; *** p < 0.001.

Confirmatory factorial analysis (CFA) of (CaOE, IDaII, and OCaD) factors in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

In this section, a comprehensive analysis of the model data was performed using statistical methods, specifically confirmatory factorial analysis (CFA). The goal was to ensure a meticulous and clear examination of the significance of the three model factors (CaOE, IDaII, and OCaD) and their respective variables.

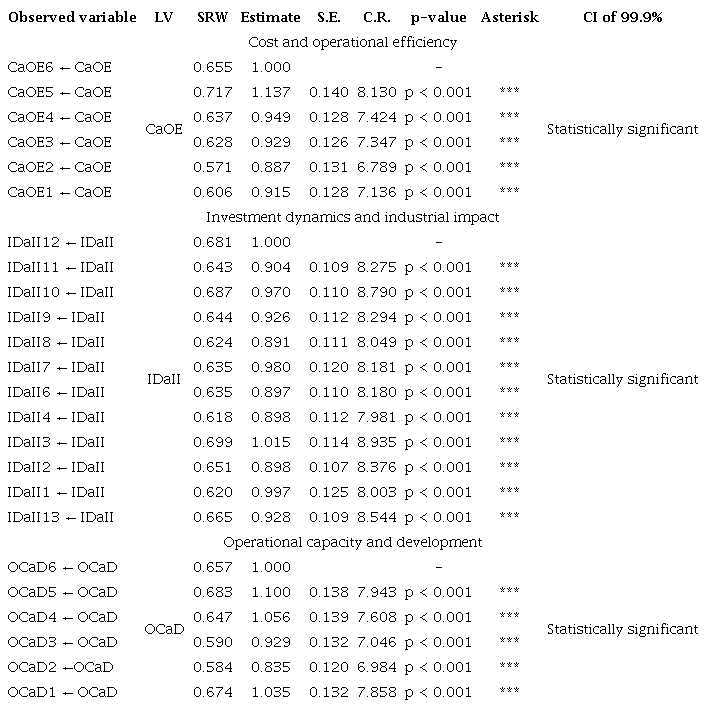

Table 9 presents the results of the confirmatory factor analysis (CFA) related to the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve efficient costs and promote sustainable growth in investments and operations in companies among the CaOE factors (1-6), IDaII (1-4, 5-13), and OCaD (1-6). In this analysis, according to Bollen (1989), the results show a significant and statistically reliable influence of each observed variable (CaOE1-6), (IDaII1-4, 6-13), and (OCaD1-6) on the latent variables CaOE, IDaII, and OCaD. According to the estimation, it is emphasized that all factor variables (CaOE, IDaII, and OCaD) are statistically significant as they have standardized regression weights greater than 0.5 and p < 0.001 (***) (Kline, 2016). Therefore, in the context of cost and operational efficiency (CaOE), the most significant variable is (CaOE5←0.717), which relates to maintenance costs. In the context of investment dynamics and industrial impact (IDaII), the most significant variables are (IDaII3←0.699), related to changes in competitive advantage due to deregulation; (IDaII10←0.687), related to global factors; and (IDaII12←0.681), related to competitive factors. Regarding operational capacity and development (OCaD), the most significant variables are (OCaD5←0.683), related to technological requirements; and (OCaD1←0.674), focused on the sustainability of the stripping firm’s assets. Therefore, based on the results of the confirmatory factor analysis (CFA), this study provides a clear approach to the main factors that influence the creation of the financial zeitgeist for companies (CaOE, IDaII, and OCaD) and have a significant and statistically certain impact on business performance. This analysis provides valuable information for business management, emphasizing that a special focus on the critical elements of each factor can improve operational efficiency, influence sustainable growth, and strengthen capacity development. In addition, the identification of key variables within each factor, such as maintenance costs in the case of CaOE, changes in competitive advantage due to implementation in the case of IDaII, and technology requirements in the case of OCaD, provides a valuable guide for companies to understand which aspects they need to prioritize to improve performance and make smart strategic decisions for the future.

Note. Author’s analysis (2023-2024). S.E.: Standard error; C.R.: Critical ratios; *** p < .001 indicates statistical significance; CI: The confidence interval is set at 99.9% (CI); SRW: Standardized regression weights; LV: Latent variable.

Note. Author’s analysis (2023-2024). Covariance estimate indicates the degree to which two variables change together. Correlation estimate is a standardized measure of the strength and direction of the relationship between two variables, where values range from -1 to +1. Cohen’s effect size interpretation: Small (0.1-0.3): Minor relationship; Medium (0.3-0.5): Noticeable effect; Large (≥ 0.5): Strong relationship, indicating significant implications. The 95% confidence interval provides a range within which the true population parameter is expected to lie with 95% confidence.

Table 9 presents the interrelationships among three critical factors: investment dynamics and industrial impact (IDaII), operational capacity and development (OCaD), and cost and operational efficiency (CaOE) regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. The analysis reveals significant insights into how these factors interact and influence one another. The relationship between investment IDaII and OCaD demonstrates a strong positive correlation, with a correlation estimate of 0.623 and a covariance estimate of 0.289. This indicates that as investment dynamics improve, operational capacity and development also tend to increase significantly. The 95% confidence interval of (3.805, 8.469) suggests robust variability in this relationship, highlighting the importance of aligning investment strategies with operational capabilities. Organizations should focus on enhancing investment dynamics to foster improvements in operational capacity, which can involve promoting innovation and forming strategic partnerships. In contrast, the correlation between IDaII and CaOE yields a moderate positive correlation, with a correlation estimate of 0.514 and a covariance estimate of 0.245. This indicates that while there is a relationship between investment dynamics and operational efficiency, it is less pronounced than the relationship with operational capacity. The confidence interval of (1.267, 2.223) reinforces the notion that investments yield measurable improvements in operational efficiency, albeit to a lesser extent. To maximize efficiency outcomes, organizations may need to refine their operational processes in conjunction with their investments. The relationship between OCaD and CaOE shows another strong positive correlation, with a correlation estimate of 0.661 and a covariance estimate of 0.284. This suggests that improvements in operational capability significantly improve cost efficiency, as organizations that develop their operational capability become more effective at managing costs. The confidence interval of (0.991, 1.863) indicates considerable certainty regarding this relationship, suggesting that companies can reliably expect operational improvements to translate into cost efficiencies. Therefore, prioritizing the development of operational capabilities may be an effective strategy for firms seeking to improve their cost efficiency. Overall, the findings illustrate the critical interdependencies among CaOE, IDaII, and OCaD. By recognizing these relationships, organizations can strategically align their investments with operational improvements to drive efficiency and competitiveness in their markets. These insights serve as a valuable framework for stakeholders involved in operational and investment decisions, emphasizing the need for a holistic approach to improving overall business performance.

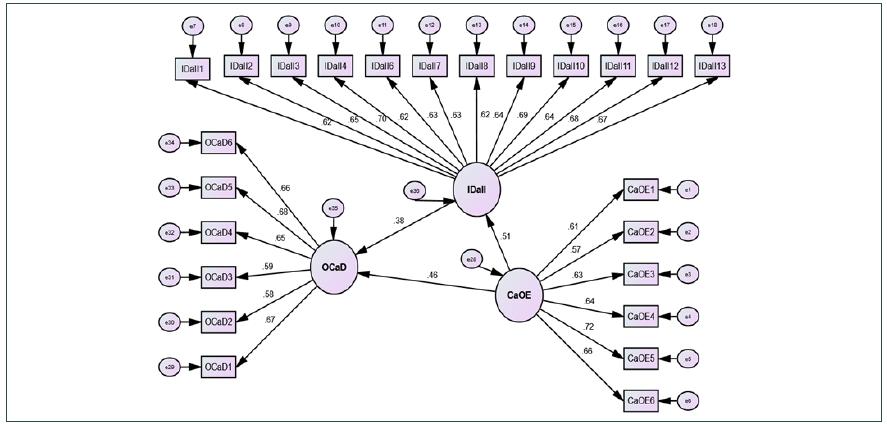

Figure 2 illustrates the interrelationships among the three primary factors (CaOE, IDaII, and OCaD), as well as the interrelationship of each factor with its respective variables (CaOE ←→ CaOE1-6; IDaII ←→ IDaII1-4, 6-13; OCaD ←→ OCaD1-6) concerning the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve cost efficiency and promote sustainable growth in investments and operations in companies. As elaborated in Table 9, there is a correlation between the three factors: CaOE ←→OCaD (r = 0.66), CaOE ←→ IDaII (r = 0.51), and IDaII ←→OCaD (r = 0.62). Additionally, it is emphasized that each factor has an interrelation with its variables greater than 0.50.

Figure 2

CFA model.

Source: Author’s analysis (2023-2024).

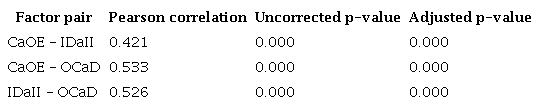

Multiple comparisons correction

Table 11 presents the Pearson correlation coefficients, uncorrected p-values, and adjusted p-values for the relationships among the factors such as cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD) regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. The correlation between CaOE and IDaII is 0.421, indicating a moderate positive relationship, suggesting that improvements in cost and operational efficiency are associated with enhanced investment dynamics and their impact on industrial performance. This relationship is statistically significant, with both uncorrected and adjusted p-values of 0.000, indicating a strong likelihood that this correlation is not due to chance. The correlation between CaOE and OCaD is stronger at 0.533, reflecting a significant relationship that implies organizations managing their costs effectively are likely to experience improved operational capacity and development processes. This finding is also supported by p-values of 0.000, which remain significant after the Bonferroni correction. Furthermore, the correlation between IDaII and OCaD is 0.526, demonstrating that better investment dynamics are associated with enhanced operational capacity and development, with the same level of statistical significance as the previous pairs. Overall, the results highlight strong interrelationships among these factors. These findings emphasize the critical role that cost efficiency and investment dynamics play in shaping organizational performance, providing empirical evidence to support the proposed hypotheses regarding their positive relationships and mediating effects.

Note. Author’s analysis (2023-2024). Note: Pearson correlation coefficients, uncorrected p-values, and adjusted p-values for the correlations between cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD).

Structural equation modeling (SEM) and model fit of (CaOE, IDaII, and OCaD) factors in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

In this section, a comprehensive analysis of the model data was conducted using statistical methods, specifically structural equation modeling (SEM) and model fit summary. These analyses were used to ensure a careful and clear examination of the significance of the three model factors (CaOE, IDaII, and OCaD) and their respective variables.

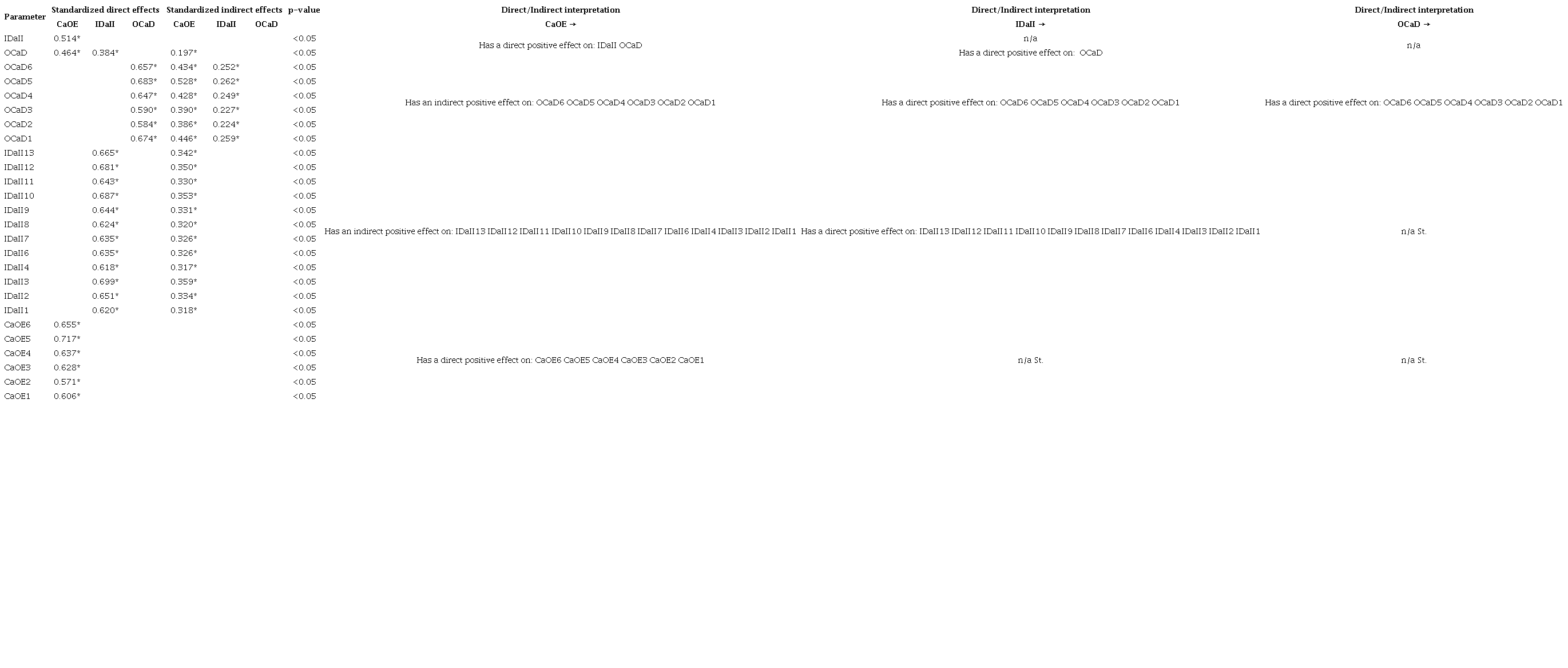

Table 12 presents the standardized direct and indirect effects of the three factors (OCaD, IDaII, and CaOE) concerning the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve cost efficiency and promote sustainable growth in investments and operations in companies. Regarding the results of the direct and indirect effects of the CaOE (cost and operational efficiency) factor, it is highlighted that an increase in CaOE triggers a direct and positive increase in the investment dynamics and industrial impact (IDaII, 0.514*) factor, as well as in the operational capacity and development (OCaD, 0.464*) factor. An increase in CaOE leads to an increase in its variables (CaOE6, 0.655*; CaOE5, 0.717*; CaOE4, 0.637*; CaOE3, 0.628*; CaOE2, 0.571*; CaOE1, 0.606*) or an increase in the cost of raw materials, labor costs, operational costs, inventory costs, maintenance costs, and costs related to inefficiency and ineffectiveness. Meanwhile, an increase in the CaOE factor causes an indirect and positive increase in the operational capacity and development factor (OCaD, 0.197*) and its variables (OCaD6, 0.434*; OCaD5, 0.4528*; OCaD4, 0.428*; OCaD3, 0.390*; OCaD2, 0.386*; OCaD1, 0.446*) or an increase in the size of the company compared to other companies, sales and purchases within business units, asset sustainability, technology requirements, and management resistance to investment. In addition, an increase in the CaOE factor indirectly and positively increases the variables of investment dynamics and industrial impact (IDaII13, 0.342*; IDaII12, 0.350*; IDaII11, 0.330*; IDaII10, 0.353*; IDaII9, 0.331*; IDaII8, 0.320*; IDaII7, 0.326*; IDaII6, 0.326*; IDaII4, 0.317*; IDaII3, 0.359*; IDaII2, 0.334*; IDaII1, 0.318*) or increases the overall economic environment, business growth, changes in competitive advantage due to deregulation, changes in tax burdens, inability to re-enter the market at a later date, technological changes, costs of non-compliance, and ethical, global, social, competitive, and demographic factors. Regarding the results of the direct and indirect effects of the IDaII (investment dynamics and industrial impact) factor, it is emphasized that an increase in IDaII causes a direct and positive increase in the operational capacity and development factor (OCaD, 0.384*). Furthermore, an increase in IDaII leads to a direct and positive increase in its variables (IDaII13, 0.665*; IDaII12, 0.681*; IDaII11, 0.643*; IDaII10, 0.687*; IDaII9, 0.644*; IDaII8, 0.624*; IDaII7, 0.635*; IDaII6, 0.635*; IDaII4, 0.618*; IDaII3, 0.699*; IDaII2, 0.651*; IDaII1; 0.620*) or a direct positive increase in the overall economic environment, business growth, changes in competitive advantage due to deregulation, changes in tax burden, inability to re-enter the market later, technological changes, costs of non-compliance, and ethical, global, social, competitive, and demographic factors. Regarding the indirect effect, an increase in IDaII causes indirect and positive increases in the variables of the operational capacity and development factor (OCaD6, 0.252*; OCaD5, 0.262*; OCaD4, 0.249*; OCaD3, 0.227*; OCaD2, 0.224*; OCaD1, 0.259*) or indirect positive increases in company size compared to other companies, sales and purchases within business units, asset sustainability, technology requirements, and management resistance to investment. Regarding the results of the direct and indirect effects of the operational capacity and development factor, it is highlighted that an increase in OCaD only causes direct and positive increases in its variables (OCaD6, 0.657*; OCaD5, 0.683*; OCaD4, 0.647*; OCaD3, 0.590*; OCaD2, 0.584*; OCaD1, 0.674*) or an increase in the size of the company compared to other companies, sales and purchases within business units, asset sustainability, technology requirements and management resistance to investments. As for the indirect effect, this factor has no effect on itself or on the factors (IDaII, CaOE) and their variables. Therefore, it can be concluded that an increase in cost and operational efficiency (CaOE) has significant positive effects on investment dynamics and industrial impact (IDaII), as well as on operational capacity and development (OCaD). This suggests that companies that focus on improving their operational efficiency and reducing costs can expect a positive impact on their growth, sustainable development, and industrial impact. Understanding these relationships can help companies shape their strategies to improve performance and competitiveness in the marketplace.

Note. Author’s analysis (2023-2024). St.: standardized; n/a: There is no direct/indirect effect. Symbols: *** p < .001, ** p < .01, * p < 0.05.

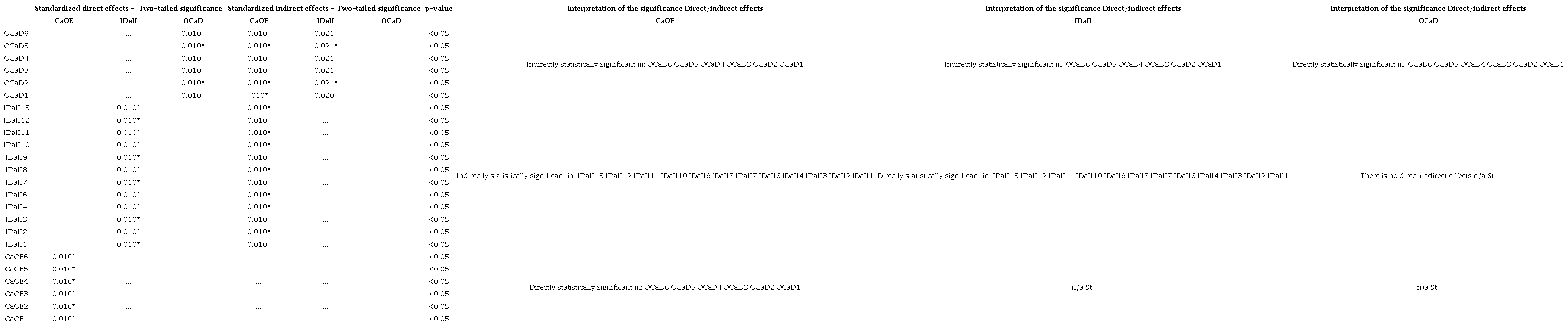

Table 13 presents the results of significant changes at the 5% level (.05) for the factors CaOE (cost and operational efficiency), IDaII (investment dynamics and industrial impact), and OCaD (operational capacity and development) related to the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve cost efficiency and promote sustainable growth in investments and operations within companies. Regarding the direct and indirect effects of the cost and operational efficiency factor (CaOE), it is observed that a significant increase in CaOE has a substantial and statistically significant effect on all its variables (CaOE6, CaOE5, CaOE4, CaOE3, CaOE2, CaOE1, p = 0.010*). In terms of indirect effects, CaOE shows a statistically significant and certain effect on the variables of the OCaD and IDaII factors (OCaD6, OCaD5, OCaD4, OCaD3, OCaD2, OCaD1, IDaII13, IDaII12, IDaII11, IDaII10, IDaII9, IDaII8, IDaII7, IDaII6, IDaII4, IDaII3, IDaII2, IDaII1, p = 0.010*). For the investment dynamics and industrial impact factor (IDaII), a significant direct increase in IDaII has a substantial and statistically significant effect on all its variables (IDaII13, IDaII12, IDaII11, IDaII10, IDaII9, IDaII8, IDaII7, IDaII6, IDaII4, IDaII3, IDaII2, IDaII1, p = 0.010*). Regarding the indirect effects, IDaII shows a statistically significant and certain effect on the variables of the operational capacity and development factor (OCaD6, OCaD5, OCaD4, OCaD3, OCaD2, p = 0.021*, and OCaD1, p = 0.020*). Regarding the operational capacity and development factor (OCaD), a significant direct increase in OCaD has a substantial and statistically significant effect on all its variables (OCaD6, OCaD5, OCaD4, OCaD3, OCaD2, OCaD1, p = 0.010*). For the flow of indirect effects, it is observed that OCaD does not have a statistically significant indirect effect on the variables of the other factors. Thus, it can be concluded that changes in CaOE, IDaII, and OCaD have significant direct and indirect effects on their variables and the variables of other factors.

Note. Author’s analysis (2023-2024). Note. St.: Standardized; * p < .05; n/a: There is no direct/indirect effect.

Table 14 indicates a robust evaluation of the model fit measures, demonstrating excellent alignment with the suggested thresholds across all indices regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. The chi-square statistic (CMIN) of 306.617, coupled with degrees of freedom (DF) at 249, results in a CMIN/DF ratio of 1.231, falling well within the acceptable range of 1 to 3, thereby indicating a good fit. The comparative fit index (CFI) of 0.965 and the Tucker-Lewis coefficient (TLI) of 0.961 exceed the recommended threshold of 0.95, indicating that the model effectively captures the relationships among the constructs of cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD). Additionally, the standardized root mean square residual (SRMR) of 0.051 and the root mean square error of approximation (RMSEA) of 0.034 further affirm the model’s excellent fit, as both values are below their respective critical thresholds. The probability of close fit (PClose) at 0.986 indicates a high likelihood that the RMSEA is less than 0.05, reinforcing confidence in the model’s validity. Collectively, these results suggest that the structural equation model adequately represents the underlying data structure, providing a solid foundation for further exploration and application in enhancing operational efficiency and investment strategies within industrial contexts, and highlighting the possibility of the presence of significant relationships and interactions between factors through direct and indirect effects when testing alternative hypotheses. These results provide a robust framework for interpreting and evaluating complex interactions in the proposed model. Future research could extend this framework to investigate additional factors that may influence these constructs or assess its applicability across different industries.

Note. Author’s analysis (2023-2024). Values above 0.90 for CFI, NFI, and TLI indicate a good fit, while RMSEA values below 0.06 suggest excellent fit. The parsimony ratio (PRATIO) above 0.50 indicates a favorable balance between model complexity and fit.

Table 15 presents the validation of the hypotheses regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth and investment and operational sustainability across three factors (CaOE, IDaII, and OCaD) at a 0.05 (5%) significance level. It highlights that CaOE has a direct and positive effect on both IDaII and OCaD (p = 0.010). Furthermore, IDaII has a direct and positive effect on OCaD (p = 0.021), and CaOE has an indirect and positive effect on OCaD through IDaII (p = 0.021). Therefore, it is emphasized that Hypothesis 1 is accepted, concluding that the positive and statistically significant result indicates that any increase in cost and operational efficiency (CaOE) is associated with a significant and positive increase in investment dynamics and operational impact (IDaII), as well as operational capacity and development. This result can be interpreted as a positive contribution of cost management and operational efficiency to improve investment dynamics and operational impact, suggesting that optimizing cost and operational efficiency can improve organizational capacity and development through the financial zeitgeist decoding process. Hypothesis 2 is accepted, concluding that the positive and statistically significant result indicates that an increase in investment dynamics and operational impact (IDaII) is associated with a positive increase in operational capacity and development (OCaD). This result can be interpreted as a significant contribution of investment dynamics and operational impact to the improvement of organizational capacity and development. Finally, Hypothesis 3 is accepted, concluding that the positive and statistically significant result indicates that the establishment of an indirect link from CaOE to OCaD through IDaII is positive. This means that the organization, through cost management and operational efficiency, has a positive impact on investment dynamics and operational impact, followed by a positive impact on operational capacity and development.

Note. Author’s analysis (2023-2024). * < 0.05.

Figure 3 presents the structural equation model (SEM) for the standardized direct and indirect effects and significance (two-tailed) of the factors (OCaD, IDaII, and CaOE) regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. As emphasized in Tables 12 and 13, the results of this figure also highlight the significant and meaningful interconnections among the factors (direct effect: CaOE → IDaII → OCaD and IDaII → OCaD; indirect effect: CaOE → OCaD). Therefore, based on the results of the complex analysis of the relationships between cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD), a key conclusion for companies is drawn. Improvements in cost efficiency, investment dynamics, industrial impact, and operational capacity development are integral to creating a sustainable and efficient environment for their operations and investments. The strong links and significant influences identified in these factors suggest that improvements in one aspect will have a significant impact on others, creating opportunities for growth and competition in the marketplace. As a result, companies will benefit from an integrated approach that includes attractive investment strategies, operational efficiency, and capacity development. This analysis provides a deep understanding of the complex relationships and interdependencies among key operational and investment components, helping companies develop strategies to achieve optimal performance and adapt to the demands of sustainable competition in their respective markets.

Figure 3

SEM model.

Source: Author’s analysis (2023-2024).

Power analysis of (CaOE, IDaII, and OCaD) factors in the sustainable development of investments and operations in the context of the financial decoding of the zeitgeist

In this section, a comprehensive analysis of the model data was performed using statistical methods, with particular emphasis on power analysis. This approach allowed a thorough and precise assessment of the power (1 - β) of the three model factors CaOE, IDaII, and OCaD and their respective variables.

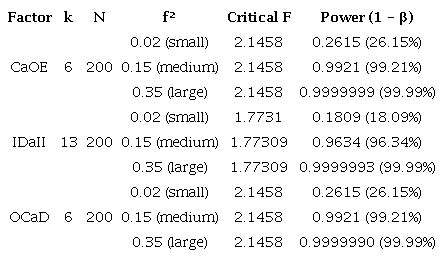

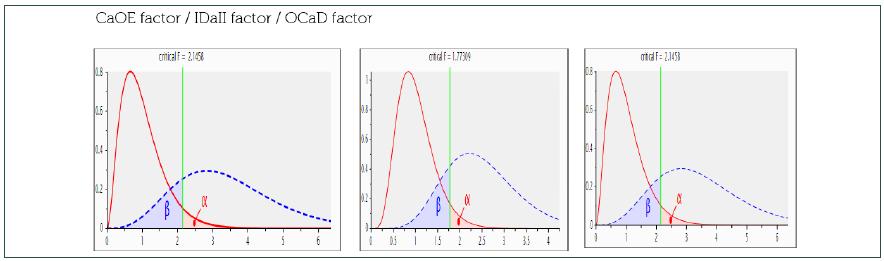

Table 16 presents the power analysis results for three factors such as cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD) concerning the decoding of the financial zeitgeist through a scientific exploration of capital calculations to achieve cost efficiency and promote sustainable growth in investments and operations in companies. This table summarizes the effect sizes, critical F-values, and statistical power (1 - β) for each factor across three effect size categories: small, medium, and large. Understanding these results is crucial for interpreting the study’s findings and implications. For the CaOE factor, the analysis indicates a significant disparity in the ability to detect different effect sizes. With a small effect size (f² = 0.02), the achieved power is a mere 0.2615 (26.15%), highlighting a low probability. Conversely, the power for medium effect size (f² = 0.15) increases dramatically to 0.9921 (99.21%), reflecting a robust capacity to detect meaningful outcomes. For large effect sizes (f² = 0.35), the power nearly reaches perfection at 0.9999999 (99.99%), instilling a high level of confidence in the findings related to CaOE. Similarly, for the IDaII factor, the power analysis reveals comparable results. The achieved power for a small effect size (f² = 0.02) stands at 0.1809 (18.09%), indicating low sensitivity to detect small effects. However, when evaluating medium effect sizes, the power improves significantly to 0.9634 (96.34%), suggesting a strong likelihood of detecting relevant effects. The power for large effects is also nearly perfect at 0.9999993 (99.99%), indicating a very high confidence in identifying substantial impacts in this area. This study effectively demonstrates high statistical power for detecting medium and large effect sizes across CaOE, IDaII, and OCaD, with achieved power values ranging from 96.34% to 99.99%. However, it is important to note that the power for detecting small effect sizes was relatively low, ranging from 18.09% to 26.15%. The sample size of 200 participants was adequate for larger effects but may limit the ability to detect smaller. According to Cohen’s benchmarks for power, this low power for small effect sizes highlights the need fore potential impacts of smaller effects. Overall, the strong capacity to detect medium and large effects reinforces the study’s contributions, providing a solid foundation for further exploration in this area.

Note. Author’s analysis (2023-2024). Effect sizes: Each factor is analyzed for three different effect sizes (small, medium, and large), providing a comprehensive view of how power varies across different contexts. Power values: Power (1 - β) is expressed as both a decimal and a percentage for clarity. Critical F: The values indicate the threshold for significance, showing consistency across effect sizes within each factor. k: Number of predictors; N: Sample size; f²: Effect size, G*Power.

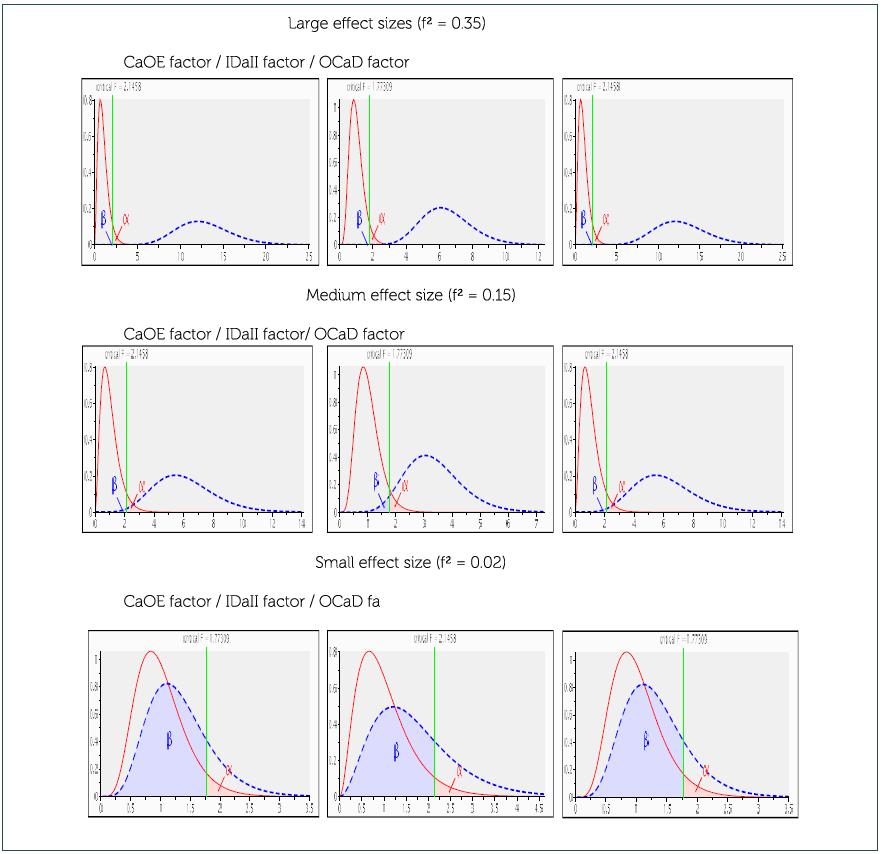

Figure 4 provides an overview of the power analysis results for three factors such as cost and operational efficiency (CaOE), investment dynamics and industrial impact (IDaII), and operational capacity and development (OCaD) regarding the decoding of the financial zeitgeist through a scientific exploration of capital calculations for sustainable economic growth in investments and operations in companies. Each factor is evaluated across small, medium, and large effect sizes, illustrating their capacity to detect significant effects. These findings highlight the differences in statistical power across the three factors and effect sizes. For CaOE, the ability to detect medium and large effects is robust, whereas small effects show low power. Similarly, IDaII demonstrates low sensitivity to small effects but strong power for medium and large effects. OCaD exhibits comparable results, with limited power for small effects but high reliability for medium and large sizes. Overall, both Table 16 and Figure 5 underscore the importance of effect size in interpreting the effectiveness of the factors analyzed.

Figure 4

Power analysis.