Research Article

The Impact of Corporate Governance on the Dividend Distribution Policy of Multinational and Domestic Enterprises

Eduardo Cezar de Oliveira eduardocezar.oliveira@bol.com.br

Michele Nascimento Jucá michele.juca@mackenzie.br

João Paulo Torre Vieito joaovieito@esce.ipvc.pt

Eduardo Cezar de Oliveira eduardocezar.oliveira@bol.com.br

Michele Nascimento Jucá michele.juca@mackenzie.br

João Paulo Torre Vieito joaovieito@esce.ipvc.pt

The Impact of Corporate Governance on the Dividend Distribution Policy of Multinational and Domestic Enterprises

BAR - Brazilian Administration Review, vol. 22, no. 2, e230105, 2025

ANPAD - Associação Nacional de Pós-Graduação e Pesquisa em Administração

Received: 04 July 2023

Accepted: 01 March 2025

Published: 11 June 2025

Funding

Funding source: National Council for Scientific and Technological Development

Contract number: 402516/2023-0

Funding statement: This study was supported by the National Council for Scientific and Technological Development (CNPq) - Process number 402516/2023-0.

ABSTRACT

Objective: this study examines the impact of a company’s status as a multinational enterprise (MNE) or a domestic enterprise (DE) on its dividend distribution policy. It also analyzes the moderating effect of corporate governance mechanisms on the payout ratios of MNEs.

Methods: the research draws on a sample of 3,397 publicly traded companies (40,310 observations) listed on the stock exchanges of countries designated as OECD key partners - Brazil, China, India, Indonesia, and South Africa - between 2008 and 2019. Data were sourced from the Capital IQ Pro, Bloomberg, and PRS Group databases. The analysis employs logistic regression (logit) and censored regression models (tobit).

Results: the results support the proposed hypotheses. MNEs tend to reinvest excess cash in their own projects, while DEs are more inclined to distribute profits to shareholders. Additionally, managerial ownership in MNEs alters this behavior, increasing the likelihood of dividend distribution.

Conclusions: these findings offer insights for corporate decision-making in multinational firms, particularly when considering political risk and tax burden in the choice between profit retention and shareholder distribution.

Keywords: Dividend policy+ corporate governance+ multinational enterprises+ logit+ tobit.

INTRODUCTION

Dividend distribution policy is one of the most important corporate decisions. Its consistency can attract investors seeking reliable returns and help mitigate agency conflicts between owners and managers. The literature on this topic has primarily focused on the traditional determinants of dividend policy, such as ownership structure, profitability, free cash flow, company life cycle, and corporate governance mechanisms (Bahreini & Adaoglu, 2018; Dewasiri et al., 2019; Wu et al., 2020). These factors are indeed essential for understanding how companies balance retaining earnings and distributing profits. However, the literature reveals gaps in understanding other equally relevant aspects in global markets. One such gap is the analysis of differences in dividend distribution policies between multinational enterprises (MNEs) and domestic enterprises (DEs) (Akhtar, 2018a, 2018b; Ghadhab, 2023).

MNEs tend to have more complex dividend policies than DEs due to their greater exposure to political risk and their access to financing across multiple markets. While MNEs benefit from geographic and industrial diversification that helps them mitigate certain risks, this characteristic also exposes them to specific challenges such as exchange rate volatility, differing tax regimes, and varying levels of regulatory risk (Allen & Pantzalis, 1996; Akhtar, 2018a; Michel & Shaked, 1986). These factors often lead MNEs to retain earnings to preserve financial flexibility, resulting in a less generous dividend policy compared to DEs, which typically operate within a single national market and face fewer uncertainties.

Corporate governance, including the composition of the board of directors and executive compensation policies, also plays a critical role in shaping dividend policy. For MNEs, whose operations are more complex and risk-laden, strong governance mechanisms can help align managerial interests with those of shareholders by promoting investor-friendly practices, including decisions about dividend payouts. Empirical studies suggest that executives with equity-based variable compensation may be less inclined to distribute dividends, opting instead to retain profits to increase firm value and thereby enhance their own compensation (Jensen, 1986). However, when dividends are viewed as a direct return for both shareholders and managers, equity-based compensation can also incentivize dividend distribution, aligning the interests of both parties (Ding et al., 2020; Trinh et al., 2020; Yet et al., 2019).

Given these dynamics, it is important to examine how MNEs and DEs adjust their dividend policies in response to internal and external factors, such as corporate governance mechanisms and political risk. This study also investigates the effect of executive variable compensation on dividend decisions, identifying differences between companies with and without international operations. Understanding these nuances can inform investors and policymakers in fostering a corporate environment that supports effective dividend policies, whether to attract foreign investment or protect shareholder interests.

This study distinguishes itself by analyzing whether the determinants of dividend distribution differ between MNEs and DEs. A further contribution is the evaluation of corporate governance mechanisms as moderators in this relationship. To that end, the study analyzes a sample of publicly traded companies from countries identified as OECD key partners (Brazil, China, India, Indonesia, and South Africa) from 2008 to 2019, using the Capital IQ database. The hypotheses are tested using logit and tobit models, with additional verification through multilevel robustness tests (hierarchical linear modeling - HLM). One of the key findings is that MNEs distribute fewer dividends than DEs. However, the adoption of corporate governance mechanisms reverses this trend, highlighting their moderating role in dividend policy.

LITERATURE REVIEW

Among the main theories that seek to explain dividend policy, the following stand out: the dividend irrelevance theory (Miller & Modigliani, 1961), the bird-in-hand theory (Gordon, 1963; Lintner, 1962), and the signaling theory (Spence, 1973). According to the dividend irrelevance theory, Miller and Modigliani (1961) argue that dividend distribution policy is irrelevant to investors, based on the assumption of a perfect market. In this context, a company’s value relies solely on the cash flows generated by its assets and the associated economic risk. Therefore, the way these flows are allocated, whether as dividends or retained earnings, does not affect the firm’s value creation.

In contrast, Lintner (1962) and Gordon (1963) assert that dividends are indeed relevant. Their perspective, known as the bird-in-hand theory, suggests that investors prefer to receive dividends sooner rather than later, as this reduces uncertainty regarding their return and increases the stock price. According to this view, investors favor immediate returns in dividends over the potential future appreciation of share prices in the capital market.

The signaling theory, introduced by Spence (1973), challenges the notion of a perfect market in which all participants have equal access to information. In the context of financial markets, this theory has been applied to explain behaviors such as dividend payments and capital gains, suggesting that these actions serve as signals to investors about a company’s future prospects or financial health.

Dividend distribution policy in domestic and multinational enterprises

While the determinants of dividend distribution have received considerable attention in academic literature, there is still a lack of studies specifically focused on understanding the factors that differentiate MNEs from DEs in this corporate decision (Akhtar, 2018a, 2018b; Ghadhab, 2023). Moreover, the limited empirical studies on this topic often present conflicting results. Fama and French (2001) and Denis and Osobov (2008), for instance, find that MNEs tend to distribute more profits than DEs due to their greater profitability, larger size, and more abundant investment opportunities (Ghose et al., 2022; Hussain & Akbar, 2022).

Conversely, Huang et al. (2015) and Akhtar (2018a, 2018b) report that MNEs distribute fewer dividends than DEs. According to the authors, MNEs are more exposed to political risks and uncertainties regarding future cash flow generation. Another important factor is the statutory tax rate in different countries: if a subsidiary operates in a country with a lower tax rate, the parent MNE’s payout ratio in its home country tends to be lower. Additionally, MNEs often maintain a more consistent dividend distribution policy over time compared to DEs, which may also lead them to distribute fewer dividends (Pieloch-Babiarz, 2020).

Im (2021) demonstrates that MNEs differ from DEs across several dimensions. MNEs typically have more assets, employ more workers, and exhibit higher productivity, profitability, and market value. They also tend to pay higher salaries, show greater innovation, and use more capital per capita than DEs. As a result, MNEs are more likely to retain operating cash flow, which supports the tendency to distribute fewer dividends. These findings support Hypothesis 1 (H1) of this study: There is a negative relationship between being an MNE and dividend distribution.

Dividend distribution policy and corporate governance mechanisms

However, this relationship may be influenced by the presence of corporate governance mechanisms, such as enhanced managerial oversight, increased transparency in decision-making, and the implementation of variable compensation policies for executives. These mechanisms can mitigate agency conflicts and reduce information asymmetry between shareholders and managers, ultimately leading to higher payout ratios (Kanojia & Bhatia, 2022; Sheikh, 2022).

According to Jensen and Meckling (1976), firms consist of a series of contracts among individuals, with the most critical being those between owners (principals) and managers (agents). Ideally, managers should act in the best interests of the owners. However, these interests are not always aligned, which requires mechanisms to mitigate conflicts. Information asymmetry, as described by Akerlof (1970), arises when one party in a transaction possesses more information than the other, leading to power imbalances and potentially suboptimal decisions (Cho et al., 2023; Taher & Al-Shboul, 2022).

Jensen (1986), Ding et al. (2020), and Gyimah and Gyapong (2021) argue that high executive compensation can increase agency costs by reducing the firm’s free cash flow, thereby lowering dividend payouts. However, when executive compensation is equity-based, it can positively influence dividend distribution (Ding et al., 2020; Jensen et al., 1992). Therefore, greater managerial ownership tends to be associated with higher dividend payments.

Other important governance mechanisms include board independence and diversity. The presence of an independent board of directors is associated with higher dividend distribution. Independent board members are more effective at addressing agency conflicts and protecting minority shareholders from expropriation by controlling shareholders (Setia-Atmaja et al., 2009; Tahir & Mushtaq, 2016; Yarram & Dollery, 2015). Therefore, a higher proportion of independent directors tends to promote greater dividend payouts (Chintrakarn et al., 2022; Kilincarslan, 2021).

Regarding gender diversity on the board of directors, the presence of women enhances the quality of discussions on complex decision-making issues. Women contribute diverse and sometimes divergent perspectives, thereby enriching the information available to the board. Moreover, boards with female members tend to engage more critically and competitively in decision-making processes, avoiding unanimous decisions and mitigating agency conflicts, as they are more likely to advocate for the interests of a broader range of stakeholders (Ain et al., 2021; Byoun et al., 2016; Gul et al., 2011; Pucheta-Martínez & Bel-Oms, 2016). Given these considerations, a higher proportion of women on the board of directors is associated with increased dividend distribution by companies. These arguments support Hypothesis 2 (H2) of this study: There is a positive relationship between corporate governance mechanisms and the distribution of dividends by MNEs.

Other determinants of dividend distribution policy

With regard to company-specific control variables, Lintner (1956) suggests that managers feel more comfortable paying dividends when firms offer higher returns on investment. Additionally, shareholders tend to expect higher dividends from more profitable companies. Firm size also plays a role: larger companies typically have greater access to financial markets and face lower financing and issuance costs, both of which facilitate dividend distribution. Therefore, a positive relationship is expected between profitability, firm size, and the payout ratio. In contrast, highly leveraged firms are less likely to distribute dividends because they need available cash to meet debt obligations (Jensen et al., 1992). Consequently, leverage and dividend distribution can function as alternative mechanisms for mitigating agency problems by limiting the firm’s free cash flow (Ain et al., 2021; Attig et al., 2021; Ding et al., 2020).

Political uncertainty is another factor influencing dividend distribution, as it can increase information asymmetry in financial markets (Farooq & Ahmed, 2019). According to La Porta et al. (2000), periods marked by high information asymmetry heighten expectations regarding payout ratios. Huang et al. (2015) demonstrate that the impact of political risk on dividend distribution is greater for MNEs. However, this effect is mitigated in countries with stronger investor protection laws and more stable political environments, suggesting a negative relationship between political risk and dividend distribution.

Finally, Pattenden and Twite (2008) note that the taxation of dividends received by individuals may actually increase the likelihood of dividend payments by firms. However, in the case of Brazil, dividends are not subject to taxation, unlike in many other countries. These cross-country differences in tax regimes make taxation a particularly relevant determinant of dividend policy for MNEs. Accordingly, a negative relationship is expected between tax incidence and dividend distribution policy.

Results of empirical studies on dividend distribution policy

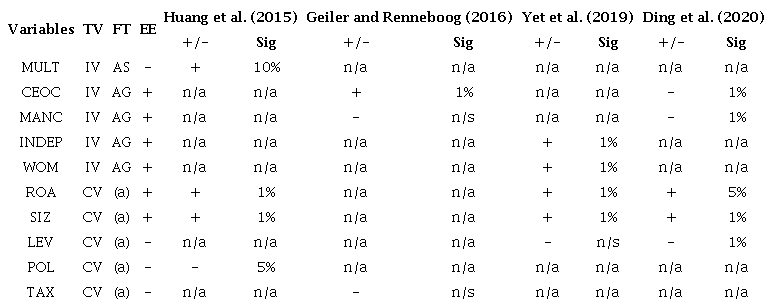

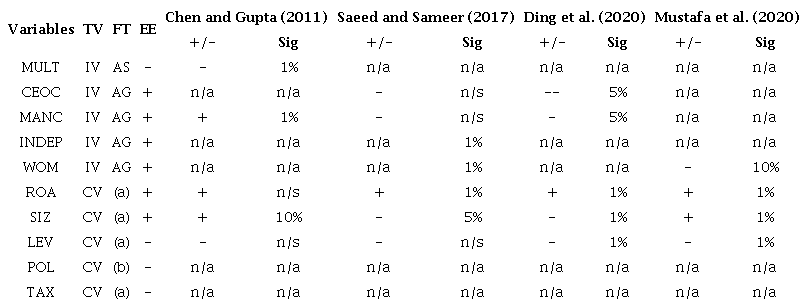

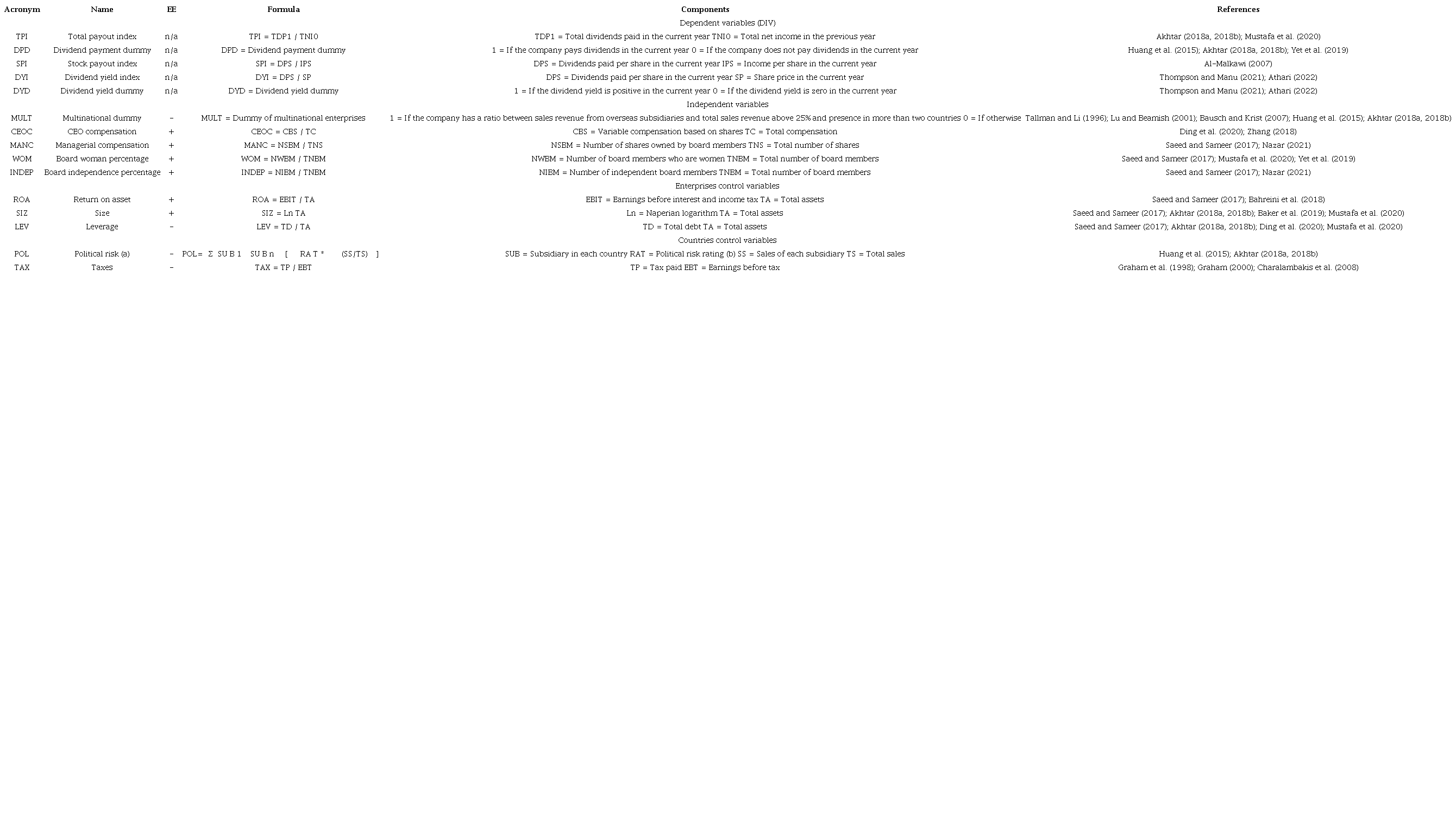

Tables 1 and 2 summarize the results of studies using logit and tobit regression models, respectively. In both cases, the dependent variable relates to dividend payment, defined as a binary variable in Table 1 and as the payout ratio in Table 2. Table 3 outlines the variables.

Note. TV = Type of variable; FT = Finance theory; EE = Expected effect (+ or -); IV = Independent variable; CV = Control variable; AG = Agency theory; AS = Information asymmetry; Sig = Significance; n/a = Not applicable; n/s = No significance; (a) = The expected relationship (whether + or -) of the control variables is supported and justified by the empirical studies presented in the referred literature; (b) The description of the variables is shown in Table 3.

Note. TV = Type of variable; FT = Finance theory; EE = Expected effect (+ or -); IV = Independent variable; CV = Control variable; AG = Agency theory; AS = Information asymmetry; Sig = Significance; n/a = Not applicable; n/s = No significance; (a) = The expected relationship (whether + or -) of the control variables is supported and justified by the empirical studies presented in the referred literature; (b) The expected negative effect of the political risk variable is supported by the empirical studies of Huang et al. (2015) and Akhtar (2018a, 2018b).

Note. (a) The political risk variable is calculated only for MNEs. (b) The rating is composed of 12 components, namely: 1. Government stability, 2. Socioeconomic conditions, 3. Investment profile, 4. Internal conflicts, 5. External conflicts, 6. Corruption, 7. Military in politics, 8. Religious tensions, 9. Law and order, 10. Ethnic tensions, 11. Democratic accountability, 12. Quality of bureaucracy.

In Table 1, Huang et al. (2015) report that MNEs distribute more dividends than expected, yet political risks negatively affect their payouts, ultimately reducing dividend distribution. Geiler and Renneboog (2016) and Yet et al. (2019) find that CEO variable compensation, as well as the presence of independent and female board members, are positively associated with dividend distribution. Conversely, Ding et al. (2020) show that stock-based compensation for CEOs and other executives is linked to lower dividend payouts. Regarding the control variables, their behavior aligns with theoretical expectations.

Regarding Table 2, Chen and Gupta (2011) find that MNEs distribute fewer dividends than DEs. Saeed and Sameer (2017), as well as Ding et al. (2020), report that variable compensation for CEOs and other executives is associated with a reduction in dividend distribution. Similarly, Mustafa et al. (2020) find a negative relationship between the presence of women on the board of directors and dividend payouts. These findings contradict the theoretical framework previously outlined. As for the control variables, most exhibit results consistent with expectations.

METHODOLOGY

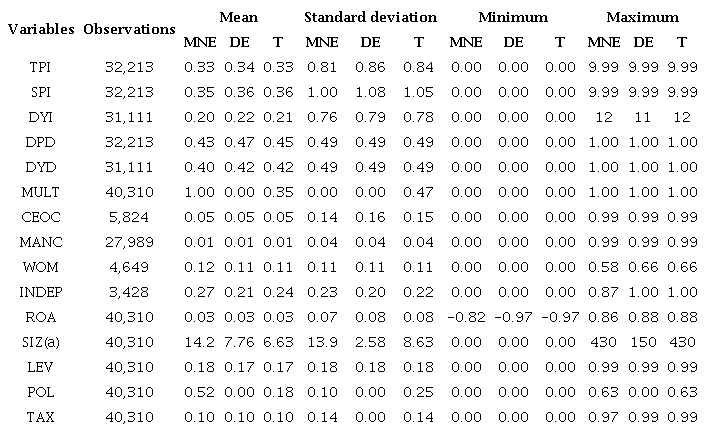

The initial sample comprises 10,147 publicly traded firms (120,450 observations) listed on the stock exchanges of the OECD key partners: Brazil, China, India, Indonesia, and South Africa. The following were excluded from the sample: (1) 2,598 companies (30,849 observations) with negative equity; (2) 1,747 companies (20,741 observations) from the financial industry; and (3) 2,405 companies (28,550 observations) with total assets below USD 1 million. As a result, the final sample includes 3,397 companies (40,310 observations). The period analyzed spans from 2008 to 2019, thereby excluding the effects of the COVID-19 pandemic. Data were collected from the Capital IQ Pro and Bloomberg databases, except for political risk ratings, which were obtained from the PRS Group - International Country Risk Guide, Table 3B: Political risk points by components. Country ratings range from 0 (highest risk) to 100 (lowest risk). The data were winsorized between the 2.5th and 97.5th percentiles.

The sample data were analyzed using descriptive statistics (see Table 4), difference in means tests (Table 5), and correlation analysis (Table 6). Hypotheses H1 and H2 were tested using logistic regressions (Tables 7 and 8) and censored regression models (tobit) (Tables 9 and 10). The logit model was applied to the binary dependent variables: dividend payment dummy (DPD) and dividend yield dummy (DYD). The tobit model was used for the continuous dependent variables: total payout index (TPI), stock payout index (SPI), and dividend yield index (DYI). This model, also known as a corner solution model, is appropriate when the dependent variable is censored within a given range and exhibits a high concentration at zero while remaining continuous for positive values, as is the case with dividend distribution (Cameron & Trivedi, 2010; Wooldridge, 2019).

Note. MNE = Multinational enterprises; DE = Domestic enterprises; T = Total sample; (a): Values in USD million.

Note. Statistically significant variables at the 1% (***), 5% (**), and 10% (*) levels.

Note. The higher values correspond to the correlation coefficient, while the lower values correspond to its significance level. The values emphasized have statistical significance at the 1% or 5% level.

Note. Statistically significant variables at the 1% (***), 5% (**), and 10% (*) levels.

Note. Statistically significant variables at the 1% (***), 5% (**), and 10% (*) levels.

Note. Statistically significant coefficients at the 1% (***), 5% (**), and 10% (*) levels; n/a = Not applicable; ME = Marginal effect percentage.

Note. Statistically significant coefficients at the 1% (***), 5% (**), and 10% (*) levels; n/a = Not applicable; ME = Marginal effect percentage.

Additionally, robustness checks were conducted using multilevel logistic and tobit regression models for both H1 (Table 11) and H2 (Table 12). These models consist of two levels: level 1 (firm) and level 2 (country) (Antonakis et al., 2021; Fávero & Belfiore, 2019). Equations (1) and (2) represent the logit and tobit models tested, respectively, with variable descriptions provided in Table 3. The analysis for H1 was performed using the full sample, with the multinational dummy (MULT) as the independent variable (Tables 7 and 9). The analysis for H2 was conducted on the subsamples of multinational enterprises (MULT = 1) and domestic enterprises (MULT = 0), using the corporate governance proxy (GOV) as the independent variable (Tables 8 and 10).

Note. Statistically significant coefficients at the 1% (***) and 5% (**) levels.

Note. Statistically significant coefficients at the 1% level; n/a = Not applicable.

Where:

DIV = Dividend distribution; MULT = Multinational dummy; GOV = CEO compensation, manager compensation, board independence, and gender diversity; FirmControls = ROA, firm size, and leverage; CountryControls = Political risk and tax rate; P = Probability; F(z) = exp(z) / [1 + exp(z)]; i = firm; t = time; k = country; θₖₜ = country-year effect; μᵢₖₜ = residuals.

Logistic regression (logit)

In the logit model, coefficients are obtained using the maximum likelihood method with pooled estimators (Cameron & Trivedi, 2010). The model’s goodness-of-fit can be assessed using the pseudo coefficient of determination (R²) and predictive accuracy measures, such as the Hosmer-Lemeshow goodness-of-fit test (Hair et al., 2018; Hosmer et al., 2013).

Censored regression (tobit)

In the tobit model, the payout ratio is censored at the lower limit of the sample (zero), reflecting companies that do not distribute dividends. There is no upper limit for positive values. Given the number of zero observations in the sample, the tobit model is more appropriate than an uncensored model, as it helps mitigate distortions in the normal distribution of the sample. To determine the appropriate model specification, whether panel or pooled, the Breusch and Pagan Lagrangian multiplier test for random effects was applied. The results indicated that the pooled model was more suitable. For post-estimation analysis, robust methods are employed to address potential issues related to the normality and heteroscedasticity of residuals. Finally, the marginal effects of the model are examined (Cameron & Trivedi, 2010).

ANALYSIS OF RESULTS

Table 4 presents descriptive statistics for the data from the subsamples of multinational enterprises (MNEs) and domestic enterprises (DEs), as well as the total sample. The DEs subsample has a higher average dividend payout across all three dependent variables than the MNEs subsample. This result may indicate that MNEs, due to their international operations, are exposed to greater risks than DEs and operate with more volatile cash flow, which could reduce dividend distribution.

Another important point is that the corporate governance variables - CEO compensation (CEOC), women on the board (WOM), and board independence (INDEP) - have relatively few observations: CEOC (5,824), WOM (4,649), and INDEP (3,428), as shown in Table 4. This limited data availability justifies their exclusion from the regression analyses in Tables 6 through 10.

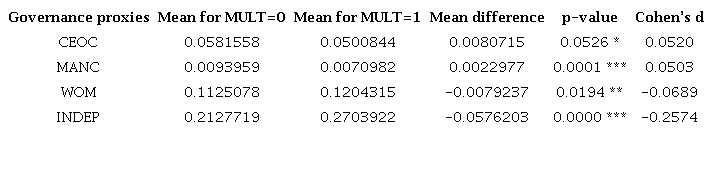

Table 5 presents a test of the difference in means for the governance proxies between the subsamples of domestic (MULT = 0) and multinational (MULT = 1) enterprises, including effect sizes calculated using Cohen’s d. This metric quantifies the standardized difference between two means. The interpretation of the effect size is based on the absolute value of the difference, while the direction of the effect is positive or negative (Cohen, 1988). The results show that all differences are statistically significant, indicating distinct corporate governance mechanisms between the two subsamples. Among the governance proxies, board independence (INDEP) exhibits the largest effect size at -0.25, meaning that the DEs (MULT = 0) have a lower average than the MNEs (MULT = 1). CEOC, MANC, and WOM present smaller effect sizes, ranging from 0.05 to -0.06 (Vaske et al., 2024; Yang & Berdine, 2021).

For the CEO compensation (CEOC) and managerial compensation (MANC) proxies, DEs (MULT = 0) show higher averages than MNEs (MULT = 1). This suggests that variable compensation, particularly stock-based, plays a more prominent role in executive governance policies among DEs than among MNEs. Conversely, for the board gender diversity (WOM) and board independence (INDEP) proxies, MNEs (MULT = 1) have higher averages than DEs (MULT = 0), indicating that gender diversity and board independence are more firmly established governance practices among MNEs compared to DEs.

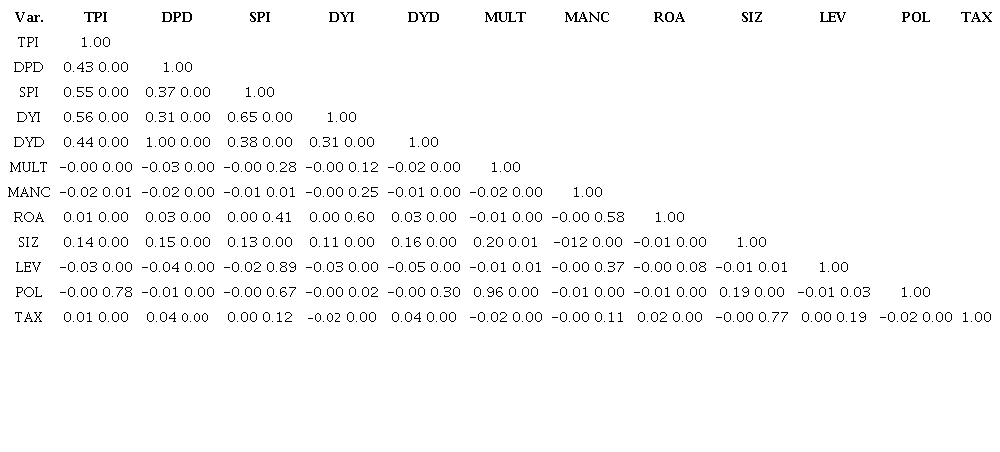

Table 6 presents the correlation levels and statistical significance between the variables in Equation (1). The dependent variables related to dividend distribution (TPI, DPD, and DYD) show a negative and statistically significant relationship with MULT. Similarly, except for DYI, the other dependent variables also exhibit a negative and statistically significant relationship with MANC. Regarding the relationships among the explanatory variables, the only pair with a high positive correlation is MULT and POL, which can be attributed to the mathematical structure of their formulations.

Results of the logistic regression analysis (Logit)

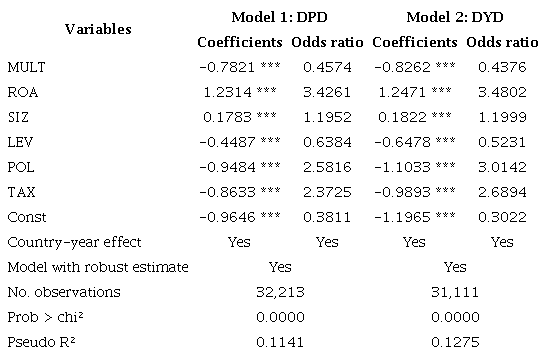

Tables 7 and 8 present the results of the logistic regressions, with DPD (Model 1) and DYD (Model 2) as the dependent variables. Table 7 tests H1, while Table 8 tests H2. Models 1 and 2 in both tables are estimated using robust standard errors, and their goodness-of-fit is assessed using the likelihood ratio (LR chi²) and its significance level (Prob > chi²), as well as the pseudo R². In Table 7, both models are statistically significant (Prob > chi² = 0.0000).

The independent variable MULT is negative and statistically significant at the 1% level in both models, confirming H1. In Model 1, being an MNE reduces the likelihood of paying dividends by 54.3% [100 × (0.457 − 1)]. In Model 2, the reduction is even greater, at 56.3% [100 × (0.437 − 1)]. These findings are consistent with Akhtar (2018a, 2018b) but contradict Huang et al. (2015) (see Table 1). MNEs face greater exposure to various risks - operational, credit, market, and political - than DEs, which leads them to retain more operating cash flow and, consequently, distribute fewer dividends.

Regarding the control variables, LEV, POL, and TAX show a negative and statistically significant relationship with dividend payments, aligning with the theories and empirical studies referenced in Table 1. Conversely, the control variables ROA and SIZ display a positive and statistically significant relationship with dividends, supporting the findings of Huang et al. (2015), Yet et al. (2019), and Ding et al. (2020).

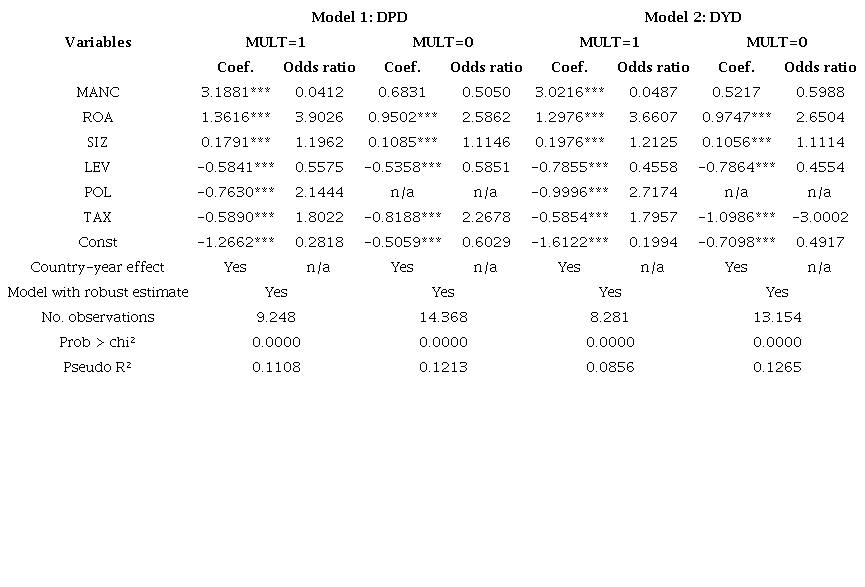

Regarding Table 8, Models 1 and 2 are statistically significant for both subsamples (Prob > chi² = 0.0000). For the independent variable MANC, a positive and statistically significant relationship with dividend distribution is observed only for MNEs (MULT = 1). This suggests that corporate governance mechanisms lead to more generous dividend distribution in MNEs compared to DEs, for which MANC does not show statistical significance. For instance, in Model 1 (DPD), a 1% increase in the percentage of shares held by MNE managers raises the probability of dividend distribution by 218% [100 × (3.1881 − 1)].

Similarly, in Model 2 (DYD), MANC shows a positive and statistically significant relationship with dividend distribution for MNEs (MULT = 1). As predicted by theory, corporate governance mechanisms help mitigate agency conflicts (Ding et al., 2020; Jensen et al., 1992). Therefore, the results support the conclusion that the variable remuneration policy for MNE managers encourages dividend distribution, confirming H2. As for the control variables, the effects (whether positive or negative) and the statistical significance of their coefficients are consistent with those presented in Table 7.

Regarding the post-estimation tests of the logistic regression models, specifically the Hosmer-Lemeshow goodness-of-fit test, the measures of sensitivity, specificity, and predictive power are analyzed. The actual data confirm an estimated dividend distribution accuracy above 60%.

Results of the tobit regression analysis

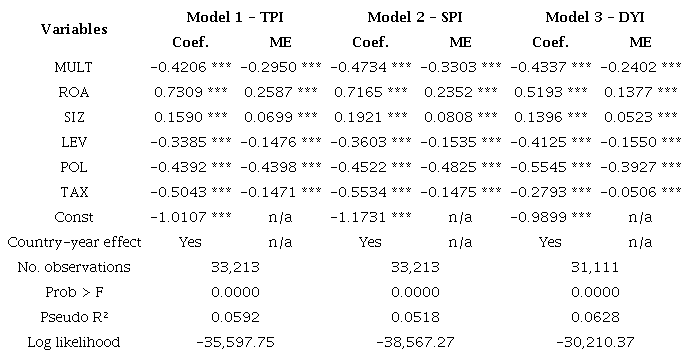

The analysis begins with the Breusch and Pagan Lagrangian multiplier test for random effects to determine the most appropriate modeling approach: pooled or panel. The null hypothesis (H0) assumes a pooled model, while the alternative hypothesis (H1) suggests a panel model with random effects. The test result (Prob > chibar² = 0.078) leads to the acceptance of H0. This indicates that the covariance between the fixed effects and the independent variables is not statistically significant, and the data should therefore be analyzed using the pooled model, where all individuals in the sample are assumed to share the same underlying characteristics. Table 9 presents the results of the pooled tobit models used to test H1, considering three dependent variables: Model 1 - TPI, Model 2 - SPI, and Model 3 - DYI. In all models, issues of heteroscedasticity and autocorrelation are addressed using robust standard errors. Each model demonstrates overall statistical significance (Prob > F = 0.0000), and the results confirm H1. Additionally, all control variables are statistically significant and show the expected effects (positive or negative).

The coefficients for the MULT variable are negative and statistically significant at the 1% level across all models. Specifically, for MNEs, dividend distribution is reduced by 0.420%, 0.473%, and 0.433% in Models 1 (TPI), 2 (SPI), and 3 (DYI), respectively. The marginal effect (ME), which indicates the probability of a non-distributing company beginning to distribute dividends, is -0.295%, -0.330%, and -0.240% for the same proxies. These findings support H1 and are consistent with those reported by Akhtar (2018a, 2018b). This suggests that firms with subsidiaries or revenue streams located outside their home country tend to retain earnings and reinvest them, rather than distributing them to shareholders as dividends.

All control variables display the expected effects (positive or negative) and are statistically significant at the 1% level. ROA and SIZ show positive coefficients, while LEV, POL, and TAX are negatively associated with dividend distribution. For instance, a 1% increase in return on assets (ROA) is associated with increases of 0.730%, 0.716%, and 0.519% in the dividend distribution proxies TPI, SPI, and DYI, respectively. These results align with findings by Saeed and Sameer (2017), Ding et al. (2020), and Mustafa et al. (2020) (see Table 2).

Regarding the construction of the dependent variables, TPI and SPI represent the ratio between dividend distribution and company profits, whereas DYI is calculated as the ratio between dividend distribution and the current share price (see Table 4). This distinction suggests that political risk (POL) exerts a more direct influence on a company’s market value than on its profitability, as argued by Attig et al. (2021). These findings also corroborate the results presented by Huang et al. (2015) and Akhtar (2018a, 2018b).

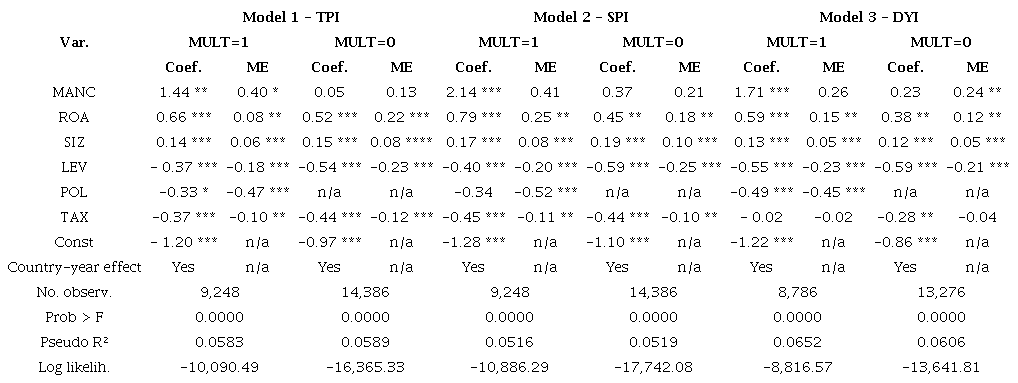

Table 10 presents the results of the pooled tobit models for testing H2, considering three dependent variables, Model 1 (TPI), Model 2 (SPI), and Model 3 (DYI), and two subsamples (MULT = 1 and MULT = 0) for each model. In all cases, heteroscedasticity and autocorrelation issues are addressed using robust standard errors. Furthermore, all models (1, 2, and 3) demonstrate overall statistical significance (Prob > F = 0.0000). Consistent with Table 8, the corporate governance mechanism, managerial compensation (MANC), shows a positive and statistically significant relationship with dividend distribution for MNEs (MULT = 1).

Specifically, for every additional 1% of shares held by board members of MNEs, dividend distribution increases by 1.44%, 2.14%, and 1.71% in Models 1, 2, and 3, respectively. Additionally, the marginal effect (ME), which indicates the probability of a company that currently distributes dividends ceasing to do so (Cameron & Trivedi, 2010), is 0.40%, 0.41%, and 0.26% for Models 1, 2, and 3, respectively. In contrast, for DEs (MULT = 0), corporate governance instruments do not show statistical significance in Models 1 and 2. However, in Model 3, these instruments exhibit a positive and statistically significant relationship with dividend distribution. It is worth noting that the DYI proxy is calculated as the ratio between dividends paid and the current year’s share price. These results confirm H2.

It is well established that high fixed executive compensation tends to reduce the profits available for distribution as dividends, leading to an expected negative relationship between the two (Ding et al., 2020; Jensen, 1986). However, when compensation is provided in the form of shares, it functions as a mechanism to align the interests of executives with those of shareholders. In this case, a positive relationship between payout ratios and executives’ variable income is expected.

Regarding the control variables, all coefficients exhibit the expected effects. ROA and SIZ show positive coefficients, whereas LEV, POL, and TAX are negatively associated with dividend distribution. For example, in the case of LEV, a 1% increase in the leverage of MNEs results in a reduction of 0.37%, 0.40%, and 0.55% in the dividend distribution proxies TPI, SPI, and DYI, respectively. These findings are consistent with those reported by Ding et al. (2020) and Mustafa et al. (2020) (see Table 2).

Concerning the TAX control variable, for every 1% increase in taxes paid by MNEs (MULT = 1), dividend distribution decreases by 0.37%, 0.45%, and 0.02% for TPI, SPI, and DYI, respectively. The reductions are even more pronounced for DEs (MULT = 0): 0.44% for both TPI and SPI, and 0.28% for DYI. Regarding the mathematical construction of the variables, TPI and SPI measure the ratio between dividend distribution and company profits. In contrast, DYI reflects the ratio between dividends and share price (see Table 3). These results suggest that taxes paid have a more immediate impact on company profits than on share prices.

Robustness tests

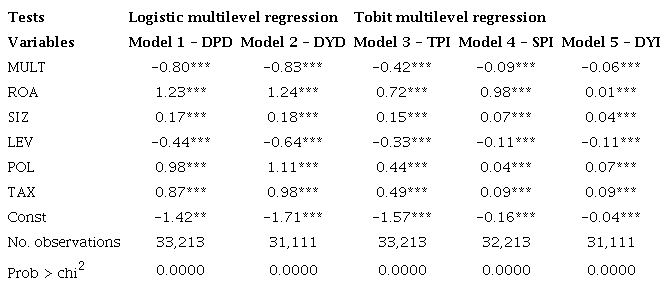

Two-level multilevel logit and tobit models were applied for the robustness tests, with level 1 representing the firm and level 2 the country. The rationale for using hierarchical linear modeling (HLM) is supported by the likelihood ratio test results for the null (unconditional) model. Since Prob ≥ chibar² = 0.0000, the null hypothesis that the random intercepts are equal to zero was rejected. It is important to note that robustness tests serve as stress testing, designed to exhaustively validate the results obtained from the traditional models (Antonakis et al., 2021; Fávero & Belfiore, 2019).

Table 11 presents the results of the H1 tests. Models 1 and 2 are logistic regressions with DPD and DYD as the dependent variables, respectively. Models 3, 4, and 5 are multilevel tobit regressions, with TPI, SPI, and DYI as the dependent variables. In all models, the coefficients for the MULT variable are negative and statistically significant at the 1% level. Specifically, in Models 3, 4, and 5, the dividend distribution percentages for MNEs are reduced by 0.42%, 0.09%, and 0.06%, respectively. Therefore, consistent with the results in Tables 7 and 9, the findings in Table 11 confirm H1 (there is a negative relationship between being an MNE and dividend distribution).

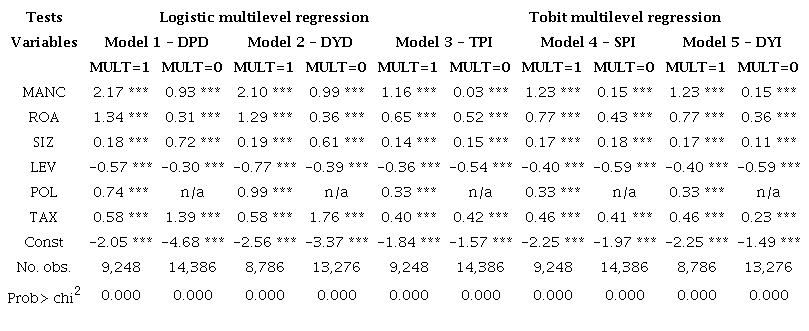

Table 12 presents the results of the H2 tests. As in Table 11, Models 1 and 2 are logistic regressions with DPD and DYD as the dependent variables. Models 3, 4, and 5, on the other hand, are multilevel tobit regressions with TPI, SPI, and DYI as the dependent variables, respectively. The results for the governance variable (MANC) are consistent with those obtained in Tables 8 and 10 for the subsample of MNEs (MULT = 1). This provides supporting evidence for H2 (there is a positive relationship between corporate governance instruments and the dividend distribution of MNEs), based on the proposed methodology.

However, for the subsample of DEs (MULT = 0), a positive and statistically significant result is also observed for MANC, which contrasts with the findings in Tables 8 and 10. Nevertheless, the associated coefficients are considerably lower and exhibit diminished statistical significance compared to the multinational subsample. This difference may be related to the consideration of intraclass correlation effects at levels 1 (firms) and 2 (countries).

CONCLUSION

This study investigates potential differences in dividend distribution between multinational enterprises (MNEs) and domestic enterprises (DEs). Additionally, it analyzes the moderating effect of corporate governance mechanisms on the payout ratios of these two types of firms. To this end, a sample of 3,397 publicly traded companies (40,310 observations) listed on stock exchanges in countries designated as OECD key partners - Brazil, China, India, Indonesia, and South Africa - is considered. The data, covering the period from 2008 to 2019, were obtained from Capital IQ Pro, Bloomberg, and the PRS Group.

Hypotheses H1 and H2 are tested using logistic regression models (logit) and left-censored tobit models, due to the high number of observations with zero payout ratios. The logit model is applied to the binary dependent variables - DPD and DYD - while the tobit model is used for the continuous metrics - TPI, SPI, and DYI. A robustness check is also performed using multilevel logistic and tobit regression models for both hypotheses.

All logit and tobit regression results (Tables 7 to 10), along with the robustness tests (Tables 11 and 12), support the confirmation of both hypotheses. In the logit model, Table 7 indicates that being a multinational company reduces the likelihood of dividend distribution by more than 75%, confirming H1. MNEs tend to reinvest excess cash in internal projects, while DEs are more likely to distribute profits to shareholders.

Table 8 reveals a positive relationship between the percentage of shares held by MNE managers and the likelihood of dividend distribution, confirming H2. For example, in Model 1 (DPD), a 1% increase in managerial ownership corresponds to a 218% increase in the probability of dividend distribution [100 × (3.1881 − 1)]. As predicted by theory, corporate governance instruments mitigate agency conflicts. Therefore, these results support the idea that variable compensation policies for MNE managers incentivize dividend distribution.

Regarding the tobit model, Table 9 shows a negative relationship between MNEs and payout proxies, while Table 10 confirms that the corporate governance mechanism - managerial compensation (MANC) - contributes to increased dividend distribution in MNEs. These results reinforce the confirmation of both H1 and H2. Furthermore, the multilevel logistic model (Table 11) and tobit model (Table 12) used in the robustness check are consistent with the findings in Tables 9 and 10.

This study contributes to the literature by analyzing how being an MNE or a DE affects the firm’s dividend distribution policy. It also demonstrates the moderating role of corporate governance - specifically, the variable compensation of MNE managers - on payout ratios. These findings provide insights into corporate decision-making in MNEs, especially regarding the impact of political risk and tax burden on profit retention, reinvestment, and distribution. The study is further distinguished by focusing on developing countries likely to become OECD members.

However, the study has certain limitations. Notably, it does not include the period of the COVID-19 pandemic (2020-2021). Additionally, the small number of observations for most governance variables - such as CEO compensation, women on the board, and board independence - justifies their exclusion from the regression tests. For future research, it is suggested to explore other governance mechanisms that could mitigate the reduction in dividend distribution among multinationals, such as executive compensation plans based on stock options and measures of employee diversity.

REFERENCES

Ain, Q. U., Yuan, X., Javaid, H. M., Zhao, J., & Xiang, L. (2021). Board gender diversity and dividend policy in Chinese listed firms. SAGE Opens, 11(1), 1-19. https://doi.org/10.1177/2158244021997807

Al-Malkawi, H. (2007). Determinants of corporate dividend policy in Jordan: An application of the Tobit model. Journal of Economic and Administrative Sciences, 23(2), 44-70. https://doi.org/10.1108/10264116200700007

Allen, L., & Pantzalis, C. (1996). Valuation of the operating flexibility of multinational corporations. Journal of International Business Studies, (27), 633-653. https://www.jstor.org/stable/155506

Akerlof, G. A. (1970). The market for “lemons”: Quality uncertainty and the market mechanism. Quarterly Journal of Economics, 84(3), 488-500. https://doi.org/10.2307/1879431

Akhtar, S. (2018a). Dividend payout determinants for Australian multinational and domestic corporations. Accounting and Finance, 58(1), 11-55. https://doi.org/10.1111/acfi.12137

Akhtar, S. (2018b). Dividend policies across multinational and domestic corporations - An international study. Accounting and Finance, 58(3), 669-695. https://doi.org/10.1111/acfi.12179

Antonakis, J., Bastardoz, N., & Rönkkö, M. (2021). On ignoring the random effects assumption in multilevel models: Review, critique, and recommendations. Organizational Research Methods, 24(2), 443-483. https://doi.org/10.1177/1094428119877457

Athari, S. A. (2022). Does investor protection affect corporate dividend policy? Evidence from Asian markets. Bulletin of Economic Research, 74(2), 579-598. https://doi.org/10.1111/boer.12310

Attig, N., Ghoul, S. E., Guedhami, O., & Zheng, X. (2021). Dividends and economic policy uncertainty: International evidence. Journal of Corporate Finance, 66. https://doi.org/10.1016/j.jcorpfin.2020.101785

Bahreini, M., & Adaoglu, C. (2018). Dividend payouts of travel and leisure companies in Western Europe: an analysis of the determinants. Tourism Economics, 24(7), 801-820. https://doi.org/10.1177/1354816618780867

Baker, H. K., Dewasiri, N. J., Koralalage, W. B. Y., & Azeez, A. A. (2019). Dividend policy determinants of Sri Lankan firms: A triangulation approach. Managerial Finance, 45(1), 2-20. https://doi.org/10.1108/MF-03-2018-0096

Bausch, A., & Krist, M. (2007). The effect of context-related moderators on the internationalization-performance relationship: Evidence from meta-analysis. Management International Review, 47(3), 319-347. https://doi.org/10.1007/s11575-007-0019-z

Byoun, S., Chang, K., & Kim, Y. (2016). Does corporate board diversity affect corporate payout policy? Asia-Pacific Journal of Financial Studies, 45, 48-101. https://doi.org/10.1111/ajfs.12119

Cameron, A. C., & Trivedi, P. K. (2010). Microeconometrics using Stata. Stata Press.

Charalambakis, E. C., Espenlaud, S. K., & Garrett, I. (2008). Leverage dynamics, the endogeneity of corporate tax status and financial distress costs, and capital structure. Social Science Research Network. https://papers.ssrn.com/sol3/papers.cfm?abstract id=110216891

Chen, M., & Gupta, S. (2011). An empirical investigation of the effect of imputation credits on remittance of overseas dividends. Journal of Contemporary Accounting & Economics, 7(1), 18-30. https://doi.org/10.1016/j.jcae.2011.06.001

Chintrakarn, P., Jiraporn, P., Treepongkaruna, S., & Lee, S. M. (2022). The effect of board independence on dividend payouts: A quasi-natural experiment. North American Journal of Economics and Finance, 63, 101836. https://doi.org/10.1016/j.najef.2022.101836

Cho, J. S., Greenwood-Nimmo, M., & Shin, Y. (2023). The asymmetric response of dividends to earning news. Finance Research Letters, 54, 103792. https://doi.org/10.1016/j.frl.2023.103792

Cohen, J. (1988). Statistical power analysis for the behavioral sciences. Routledge Academic.

Denis, D. J., & Osobov, I. (2008). Why do firms pay dividends? International evidence on the determinants of dividend policy. Journal of Financial Economics, 89(1) 62-82. https://doi.org/10.1016/j.jfineco.2007.06.006

Dewasiri, N. J., Koralalage, W. B. Y., Azeez, A. A., Jayarathne, P. G. S. A., Kuruppuarachchi, D., & Weerasinghe, V. A. (2019). Determinants of dividend policy: Evidence from an emerging and developing market. Managerial Finance, 45(3), 413-429. https://doi.org/10.1108/MF-09-2017-0331

Ding, C., Ho, C.Y., & Chang, M. (2020). CEO and CFO equity compensation and dividend payout over the firm lifecycle. Global Finance Journal, 49, 100562. https://doi.org/10.1016/j.gfj.2020.100562

Fama, E. F., & French, K. R. (2001). Disappearing dividends: Changing firm characteristics or lower propensity to pay? Journal of Financial Economics, 60(1) 3-43. http://dx.doi.org/10.2139/ssrn.203092

Farooq, O., & Ahmed, N. (2019). Dividend policy and political uncertainty: Evidence from the US presidential elections. Research in International Business and Finance, 48(1), 201-209. https://doi.org/10.1016/j.ribaf.2019.01.003

Fávero, L. P., & Belfiore, P. (2019). Data science for business and decision making. Academic Press.

Ghadhab, I. (2023). Bonding, signaling theory and dividend policy: Evidence from multinational firms. Journal of Asset Management, 24, 69-83. https://doi.org/10.1057/s41260-022-00289-7

Ghose, B., Baruah, D., & Gope, K. (2022). Propensity to propose and pay dividend: Does firm characteristics matter? Global Business Review, 0(0). https://doi.org/10.1177/09721509221110314

Geiler, P. & Renneboog, L. (2016). Executive remuneration and the payout decision. Corporate Governance: An International Review, 24(1), 42-63. https://doi.org/10.1111/corg.12127

Graham, J. R, Lemmon, M., & Schallheim, J. (1998). Debt, leases and the endogeneity of corporate tax status. Journal of Finance, 53(1), 131-162. https://doi.org/10.1111/0022-1082.55404

Graham, J. R. (2000). How big are the tax benefits of debt? Journal of Finance, 55(5), 1901-1941. https://doi.org/10.1111/0022-1082.00277

Gordon, M. J. (1963). Optimal investment and financing policy. Journal of Finance, 28(2), 264-272. https://doi.org/10.1111/j.1540-6261.1963.tb00722.x

Gul, F. A., Srinidhi, B., & Ng, A. C. (2011). Does board gender diversity improve the informativeness of stock prices? Journal of Accounting & Economics, 51(3), 314-338. https://doi.org/10.1016/j.jacceco.2011.01.005

Gyimah, D., & Gyapong, E. (2021). Managerial entrenchment and payout policy: A catering effect. International Review of Financial analysis, 73, 101600. https://doi.org/10.1016/j.irfa.2020.101600

Hair, J. F., Jr., Willian, C. B., Babin, B. J, & Anderson, R. E. (2018). Multivariate data analysis. Cengage.

Hosmer, D. W., Lemeshow. S., & Sturdivant. R. (2013). Aplied Logistic Regression. John Wiley.

Hussain, A., & Akbar, M. (2022). Dividend policy and earnings management: Do agency problem and financing constraints matter? Borsa Istanbul Review, 22(5), 839-853. https://doi.org/10.1016/j.bir.2022.05.003

Huang, T., Wu, F., Yu, J., & Zhang, B. (2015). Political risk and dividend policy: Evidence from international political crises. Journal of International Business Studies, 46(5), 1-22. https://doi.org/10.1057/jibs.2015.2

Im, J. (2021). Multinational investment policy: Why do multinational enterprises invest less? http://dx.doi.org/10.2139/ssrn.3769610

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review, 76(2), 323-329. https://www.jstor.org/stable/1818789

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Jensen, G. R., Solberg, D. P., & Zorn, T. S. (1992). Simultaneous determination of insider ownership, debt and dividend policies. Journal of Financial and Quantitative Analysis, 27(2), 247-263. http://dx.doi.org/10.2307/2331370

Kanojia, S., & Bhatia, B. S. (2022). Corporate governance and dividend policy of the US and Indian companies. Journal of Management and Governance, 26, 1339-1373. https://doi.org/10.1007/s10997-021-09587-5

Kilincarslan, E. (2021) The influence of board independence on dividend policy in controlling agency problems in family firms. International Journal of Accounting & Information Management, 29(4), 552-582. https://doi.org/10.1108/IJAIM-03-2021-0056

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., & Vishny, R. W. (2000). Agency problems and dividend policies around the world. Journal of Finance, 55(1), 1-33. https://doi.org/10.1111/0022-1082.00199

Lintner, J. (1956). Distribution of incomes of corporations among dividends, retained earnings, and taxes. American Economic Review, 46(2), 97-113. https://www.jstor.org/stable/1910664

Lintner, J. (1962). Dividends, earnings, leverage, stock prices and the supply of capital to corporations. Review Economics and Statistics, 44(3), 243-269. https://doi.org/10.2307/1927792

Lu, J. W., & Beamish, P. W. (2001). The internationalization and performance of SMEs. Strategic Management Journal, 22(6-7), 565-586. https://doi.org/10.1002/smj.184

Michel, A., & Shaked, A. (1986). Multinational corporations versus domestic corporation’s financial performance and characteristics. Journal of International Business Studies, (16), 89-104. https://doi.org/10.1057/palgrave.jibs.8490435

Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth and the valuation of shares. Journal of Business, (34)4, 411-433. https://doi.org/10.1086/294442

Mustafa, A., Saeed, A., Awais, M., & Aziz, S. (2020). Board-gender diversity, family ownership, and dividend announcement: Evidence from Asian emerging economies. Journal of Risk and Financial Management, 13(4), 1-20. https://doi.org/10.3390/jrfm13040062

Nazar, M. C. A. (2021). The influence of corporate governance on dividend decisions of listed firms: Evidence from Sri Lanka. Journal of Asian Finance, Economics and Business, 8(2), 289-295. https://doi.org/10.13106/jafeb.2021.vol8.no2.0289

Pattenden, K., & Twite, G. (2008). Taxes and dividend policy under alternative tax regimes. Journal of Corporate Finance, 14(1), 1-16. https://doi.org/10.1016/j.jcorpfin.2007.09.002

Pieloch-Babiarz, A. (2020). Characteristics identifying the companies conducting different dividend policy: evidence from Poland. Equilibrium. Quarterly Journal of Economics and Economic Policy, 15(1), 63-85. https://doi.org/10.24136/eq.2020.004

Pucheta-Martínez, M. C., & Bel-Oms, I. (2016). The board of directors and dividend policy: The effect of gender diversity. Industrial and Corporate Change, 25(3), 523-547. https://doi.org/10.1093/icc/dtv040

Saeed, A., & Sameer, M. (2017). Impact of board gender diversity on dividend payments: Evidence from some emerging economies. International Business Review, 26(6), 1100-1113. https://doi.org/10.1016/j.ibusrev.2017.04.005

Setia-Atmaja, L., Tanewski, G. A. & Skully, M. (2009). The role of dividends, debt and board structure in the governance of family-controlled firms. Journal of Business Finance & Accounting, 36(7), 863-898. https://doi.org/10.1111/j.1468-5957.2009.02151.x

Sheikh, S. (2022). CEO power and the likelihood of paying dividends: Effect of profitability and cash flow volatility. Journal of Corporate Finance, 73, 102186. https://doi.org/10.1016/j.jcorpfin.2022.102186

Spence, M. (1973). Job market signaling. Quarterly Journal of Economics, 87(3), 355-374. https://doi.org/10.2307/1882010

Taher, F. N. A., & Al-Shboul, M. (2022). Dividend policy, its asymmetric behavior and stock liquidity. Journal of Economic Studies, 50(3), 578-600. https://doi.org/10.1108/JES-10-2021-0513

Tahir, M., & Mushtaq, M. (2016). Determinants of dividend payout: Evidence from listed oil and gas companies of Pakistan. Journal of Asian Finance, Economics and Business, 3(4), 25-37. https://doi.org/10.13106/jafeb.2016.vol3.no4.25

Tallman, S., & Li, J. (1996). Effects of international diversity and product diversity on the performance of multinational firms. Academy of Management journal, 39(1), 179-196. https://doi.org/10.5465/256635

Thompson, E. K, & Manu, S. A. (2021). The impact of board composition on the dividend policy of US firms. Corporate Governance, 21(5), 737-753. https://doi.org/10.1108/CG-05-2020-0182

Trinh, V. Q., Cao, N. D., Dinh, L. H., & Nguyen, H. N. (2020). Boardroom gender diversity and dividend payout strategies: Effects of mergers deals. International Journal of Finance and Economics, 1-22. https://doi.org/10.1002/ijfe.2106

Vaske, J. J., Beaman, J. A. Y., & Miller, C. A. (2024). Practical application of a minimal important percent difference formulation of Cohen’s d. Human Dimensions of Wildlife, 29(3), 269-283. https://doi.org/10.1080/10871209.2023.2233544

Wooldridge, J. M. (2019). Introductory econometrics: A modern approach. Cengage Learning.

Wu, M., Ni, Y., & Huang, P. (2020). Dividend payouts and family-controlled firms - The effect of culture on business. Quarterly Review of Economics and Finance, 75, 221-228. https://doi.org/10.1016/j.qref.2019.03.004

Yang, S., & Berdine, G. (2021). Effect size. Southwest Respiratory and Critical Care Chronicles, 9(40), 65-68. https://doi.org/10.12746/swrccc.v9i40.901

Yarram, S. R., & Dollery, B. (2015). Corporate governance and financial policies influence of board characteristics on the dividend policy of Australian firms. Managerial Finance, 41(3), 267-285. https://doi.org/10.1108/MF-03-2014-0086

Yet, D., Deng, J., Liu, Y., Szewczyk, S.H., & Chen, X. (2019). Does board gender diversity increase dividend payouts? Analysis of global evidence. Journal of Corporate Finance, 58, 1-26. https://doi.org/10.1016/j.jcorpfin.2019.04.002

Zhang, D. (2018). CEO dividend protection. Journal of Empirical Finance, 45, 194-211. https://doi.org/10.1016/j.jempfin.2017.10.005

Notes

BAR - Brazilian Administration Review encourages data sharing but, in compliance with ethical principles, it does not demand the disclosure of any means of identifying research subjects.

Plagiarism Check: BAR maintains the practice of submitting all documents received to the plagiarism check, using specific tools, e.g.: iThenticate.

Author notes

(Universidade do Vale do Rio dos Sinos, Brazil)

Ricardo Limongi https://orcid.org/0000-0003-3231-7515

(Universidade Federal de Goiás, Brazil)

(Universidade Federal de Uberlândia, Faculdade de Gestão e Negócios, Brazil)

and one anonimous reviewer.

Corresponding author: Eduardo Cezar de Oliveira Universidade Presbiteriana Mackenzie Rua da Consolação, n. 930, Consolação, CEP 01302-907, São Paulo, SP, Brazil.

Conflict of interest declaration